The Government proposed that individuals with superannuation account balances exceeding $3 million pay 30 per cent tax on their earnings in accumulation, while those with lower balances continue to pay 15 per cent.

Around 80,000 people will be affected by the Government’s proposed measure, with the majority having balances under $5 million in super (33,500 with $3-4 million and 16,500 with $4-$5million). The estimated revenue generated in the first year is approximately $2 billion.

The announcement of this proposed measure comes after the release of the 2022‑23 Tax Expenditures and Insights Statement, which suggests that the tax concessions on superannuation result in foregone revenue of around $50 billion annually. The statement also projects that this cost is expected to exceed that of the Age Pension by 2050.

The policy underpinning the proposed changes is based on a simple principle, which is also the foundation of Division 293 of the Income Tax Assessment Act 1997. This principle states that the more capacity one has to contribute to their retirement savings, the less concessional treatment those savings should receive.

However, there are several aspects of the proposed measures that warrant further consideration.

Treasury figures

There are doubts about the accuracy of the figures presented by the Treasury, as noted by Professor Deborah Ralston. The Treasury estimates the cost of superannuation tax concessions using the revenue forgone method, which compares the concessional 15 per cent to what would be collected at the top marginal rate of 45 per cent. However, these estimates do not take into account withdrawals or other legitimate means of reducing tax, nor do they consider savings made on the Age Pension.

Other methods, such as the ‘expenditure tax benchmark’, provide estimates of tax forgone that are significantly lower. Therefore, it is possible that the cost of the concession and the projected revenue from the proposed changes are overestimated.

This is particularly so when one considers the avenues open to taxpayers to legitimately avoid the imposition of this tax.

Tax avoidance

The majority of the 80,000 superannuates affected by the proposed changes have self-managed superannuation funds (SMSF) and multiple options to legitimately avoid this tax.

One possible way for SMSF holders to avoid this tax is by adding more family members to their SMSF. Each fund can have up to six members, and the $3 million cap applies at the individual level, not the fund level.

Those past the preservation age might equally chose to withdraw their savings and pass it straight to their children, which would also avoid the tax associated with passing super death benefits on to non-dependents.

Another way for SMSF holders to avoid the tax is to withdraw funds from superannuation and invest in alternative vehicles that offer comparable tax savings, such as investment bonds. Investment bonds provide long-term tax-protected investing outside super. Indeed, a similar trend was observed when superannuation concessions were reduced in 2016.

Given these options available to SMSF holders, it is highly unlikely that the proposed changes will generate anywhere near the $2 billion estimated by Treasury. Some argue that even based on Treasury’s figures, the tax will not generate sufficient revenue.

Unrealised earnings

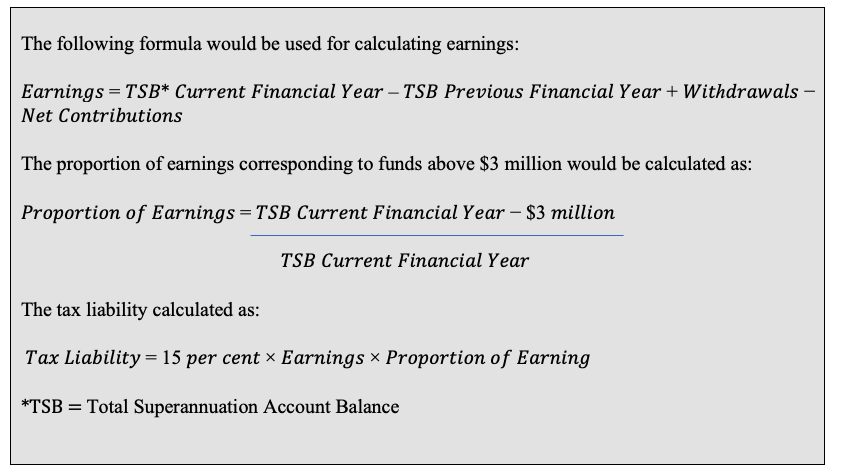

Another concern with the proposed tax is that it will be assessed on unrealised gains. This idea is not new, as the 2009 Henry Tax Review also suggested the possibility of shifting to taxing unrealised gains based on accrual accounting. However, the valuations of unlisted asserts by super funds, which currently calculate members’ annual interests as including unrealised earnings, are often controversial and are under scrutiny from the Australian Prudential Regulation Authority (APRA).

This aspect of the proposed changes appears to discriminate in favour of industry super funds. SMSFs are predominately invested in listed assets, such as shares, where prices are calculated daily, unlike industry funds, which tend to hold a large proportion of unlisted assets whose values are not priced on an open exchange.

Capital gains discount

Another cause for concern is that these changes effectively remove the capital gains discount for complying superannuation funds.

Currently, capital gains generated within a complying superannuation entity receive a one third discount under section 115.100 of the Income Tax Assessment Act 1997. As a result, a complying superannuation entity generally pays an effective tax rate of 10 per cent on capital gains instead of the standard rate of 15 per cent.

The proposed changes would eliminate the capital gains discount because unrealised capital gains would be taxed as income, effectively removing the concession and reducing the capital gain to zero under Section 118-20 of the Act.

Indexation of the $3 million threshold

A particular concern regarding the proposed changes is the lack of indexation of the threshold.

This aspect of the proposal is likely to have a disproportionally adverse impact on younger taxpayers, as the $3 million threshold is not indexed to inflation.

The Grattan Institute estimates that within 30 years, around 10 per cent of workers earning an average of over $142,000 per year throughout their careers will retire with nominal super balances of $3 million or more. Indeed, analysis by the Financial Services Council suggests that the present-day value of $3 million would be a far more modest $1.1 million for a worker currently aged 25 and planning to retire at 65.

Moreover, for small business taxpayers who plan to sell their business and transfer the proceeds into their superannuation, as well as those who intend to deposit the proceeds from selling their family home, the $3 million threshold is also relatively modest.

The claim that these changes do not affect 99.5 per cent of the population is misleading, as the ultimate impact of these measures will not be limited to wealthy superannuates. Instead, the broader effects will be borne by the majority of taxpayers.

Evaluation of policy

There is clearly a need to align the tax on contributions with the tax on earnings and introduce a greater degree of progressivity into the superannuation system.

While measures such as the introduction of Division 293 of the Income Tax Assessment Act 1997 have shown that progressive taxation within the superannuation system is possible, the proposed changes are unlikely to generate substantial revenue and may disproportionally burden younger taxpayers.

Possible alternatives

An alternative approach to the proposed changes could be the introduction of a marginal rates system that applies to both contributions and income. Such a system would allow for the concessional treatment of superannuation while also introducing a more progressive tax structure.

Aligning marginal income tax rates with the concessional treatment of super would ensure consistency for all taxpayers and simplify the system by eliminating the need for contribution caps.

Further consideration should be given to the transfer balance cap, specifically in determining the appropriate level of retirement income that should be subject to tax exemption and what should receive only concessional treatment.

To ensure the long-term viability of any reforms, it is crucial to consider indexation of all thresholds. What may be deemed an appropriate level today could soon become distorted by inflation.

Don’t worry. It’s all avoidable. There is a tax haven called the United States of America which can assist.