The key challenge for the Australian retirement income system is how to take full advantage of its Defined Contribution basis (including inter-generational equity and financial sustainability) while also achieving an outcome broadly similar to that of Defined Benefit social security systems overseas (including adequacy, security and cohesion).

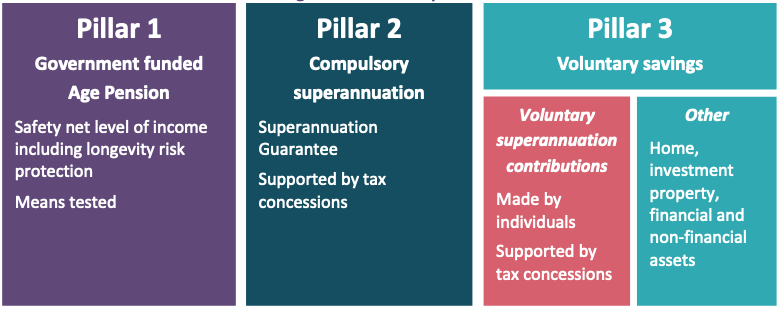

This is the conclusion of our submission to the Retirement Income Review, drawing on the work we did with the Committee for Sustainable Retirement Incomes in 2016. The emphasis now should be placed on the pensions phase, not the accumulation phase, and all the pillars of the system (the age pension, mandated superannuation and voluntary savings for retirement included supplementary superannuation and housing, see Figure 1) need to work together to deliver adequate and secure retirement income streams. The submission also canvasses the ongoing debate about the adequacy of the Superannuation Guarantee, and calls on the Review to settle this by its own examination with carefully considered and explicit assumptions.

Figure 1: The three pillars of Australia’s retirement income system identified by the Review

Source: Retirement Income Review Consultation Paper, p. 4

The following summarises the main points of the submission.

Purpose of the system and role of the pillars

The idea of security as well as adequacy needs to be incorporated in the system’s objective. The formulation suggested by the Committee for Sustainable Retirement Incomes is:

‘To provide adequate income through all the years of retirement for all Australians in a sustainable way’.

Important aspects of the objective are not widely understood:

- Most significantly, accumulated superannuation savings from pillars 2 and 3 are not widely considered in terms of the retirement income streams they can fund;

- Accordingly, there is little understanding of ‘adequacy’, relating accumulated assets to pre-retirement incomes and living standards; and

- There is a lack of understanding of longevity risk and how to manage it; few people are appreciating that efficient management of longevity risk requires pooling.

It is essential to change the language surrounding our retirement income system, as well as to ensure appropriate products are readily available. It is also important to address the complexity of the system, presenting all three pillars in terms of secure retirement income streams, and simplifying the means test.

Principles for assessing the system

We would add ‘security’ to the suggested principles of adequacy, equity, sustainability and cohesion. We have included some comments on security in the section below on adequacy. We support the inclusion of ‘cohesion’, as it underlines the idea of a retirement income ‘system’ that should be coherent and widely understood.

Adequacy (and security)

Unlike the Committee for Sustainable Retirement Incomes’ approach, the Review’s Consultation Paper does not have a separate section devoted to ‘post-retirement incomes’. Work done over the last two years within the Government on Comprehensive Income Products for Retirement, or CIPRs, is aimed to guide retirees towards turning their accumulated superannuation savings into (secure) income streams suited to their circumstances and helping them to optimise their consumption over their retirement years. As yet, however, CIPRs are not widely offered or used.

We strongly recommend the Review investigate why the take-up of annuities remains so low, and what actions might lead to the optimal use of accumulated savings for the purpose of ensuring adequate and secure lifetime incomes. There is a case for the Government to sell annuities itself at prices set by the actuary.

Adequacy should be considered against two implied objectives: poverty alleviation and income maintenance.

In terms of poverty alleviation, the Harmer Report and work by Peter Whiteford suggest that the basic rates of age pension are sufficient for those who own their own homes, but that rent assistance is insufficient for those in private rental accommodation. Newstart (now renamed JobSeeker payment) is much lower than the age pension and is not indexed to wages. It is well below any reasonable standard of poverty though relied upon by people unable to find employment ahead of age pension age.

Defining adequacy for the purposes of income maintenance is complex. First, there is debate about the denominator – the pre-retirement income base. Second, there is debate about the numerator – the measure of income post-retirement. Third, there is the benchmark ratio between the denominator and numerator (a net income replacement rate of 70 per cent is commonly used, for example, by the OECD, at least for those around median to average earnings).

It is also important to take into account wide variation in both pre-retirement and post-retirement experiences and preferences. On the basis of modelling by Phil Gallagher, the Committee for Sustainable Retirement Incomes considered that increasing the superannuation guarantee to 12 per cent, as currently legislated, will deliver slightly below the 70 per cent benchmark for those on median earnings, and was appropriate.

We recommend, however, that the Review conduct its own examination, drawing on actuarial advice and using a range of typical cameos of working lives and family circumstances, together with carefully considered, explicit assumptions about the benchmark pre-retirement income in each case and the appropriate post-retirement consumption of accumulated savings. We suggest the Review apply a 70 per cent net income replacement rate at retirement for those on around median earnings or slightly above, to assess the optimal superannuation guarantee rate.

Equity

Australia’s reliance on Defined Contribution superannuation means it achieves inter-generational equity far better than most other countries. The age pension ensures generally good protection against poverty, and concentrates assistance on those most in need.

There is a strong case for including housing assets beyond some quite high threshold in the means test. We are concerned, on the other hand, about the likely impact of the assets test as amended in 2017. The increased taper (above the increased thresholds) means that, over a wide range of assessable assets, a pensioner may have a lower retirement income despite a higher level of assets. Andrew Podger and David Knox have been exploring how a merged means test might be designed today, drawing on the principles behind such a test in the 1960s. They firmly argue for some relaxation of the assets test taper (their initial work suggests an effective taper of around 3 or 4 per cent).

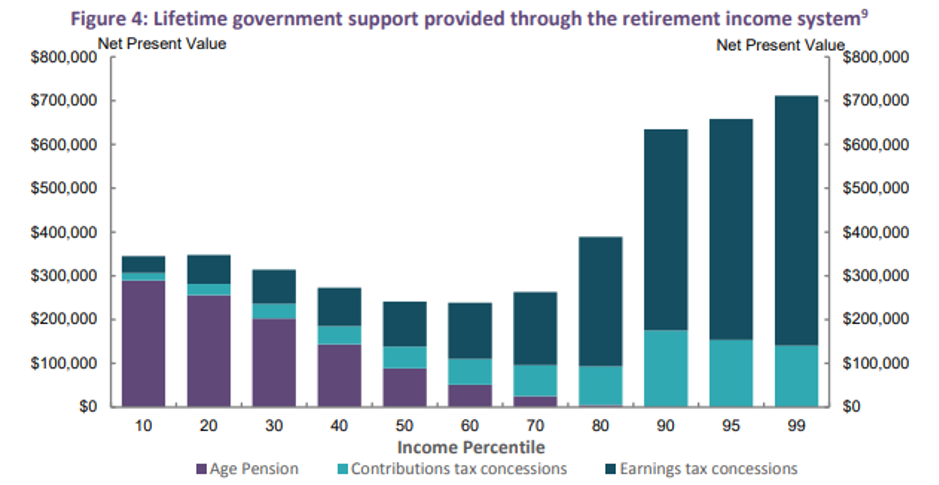

We strongly question the way the Consultation Paper presents the incidence of superannuation tax concessions (Figure 4, p. 18, copy below). This is based upon a benchmark TEE taxation regime for savings (taxed contributions-exempt earnings-exempt withdrawals). That may be appropriate for most savings, but if the purpose of superannuation is to spread lifetime earnings, then lifetime earnings represents the appropriate base for applying the (progressive) income tax. That implies the benchmark should be EET (exempt contributions-exempt earnings-taxed withdrawals), particularly given the period over which the savings are compulsorily held. It is also the only way to tax Defined Benefit schemes and, accordingly, is the orthodox approach internationally.

Source: Retirement Income Review Consultation Paper, p. 18

Work commissioned by the Committee for Sustainable Retirement Incomes from Gallagher revealed that the current ttE regime (low taxes on contributions and earnings, but withdrawals exempted) has a similar impact on after tax retirement incomes to that of the ideal EET regime at most income levels and for most of the cameos studied. Accordingly, using an EET benchmark, not only would the tax expenditures shown in Figure 4 disappear, but also the apparent regressive impact. Indeed, together with the means-tested age pension, the overall retirement income system would be revealed as quite progressive and equitable.

One issue that is frequently raised is whether the system is fair in its treatment of men and women. There continues to be a sharp difference between the accumulated superannuation savings of men and women at the same age, but the data presented (including by Treasury) does not take into account the legal entitlement of married people to a half share of their partners’ savings, nor for those who have divorced or separated in the past, any share of their ex-partners’ savings they may have received. These factors are highly significant given that at age pension age 70 per cent of people have partners and, of the rest, a significant number previously had partners. Policies which facilitate greater opportunities for women to gain employment and experience equal opportunities for career progression et cetera should be the primary focus for addressing the unequal superannuation savings amongst men and women.

Sustainability

The Australian age pension is remarkably sustainable: the cost in 2015 was 4.3 per cent of GDP, less than in almost any other advanced OECD country and not much more than half the OECD average of 8 per cent. Increasing superannuation contributions involves some cost to the budget notwithstanding the strong case for the current tax treatment involved as discussed above, but we are not convinced that such a budgetary cost would be excessive, now or into the future: rather, it is the inevitable consequence of a system that facilitates the spreading of lifetime earnings in an inter-generationally equitable fashion.

Cohesion

It is primarily the pension means test which makes cohesion difficult. A merged means test could be designed to simplify the test, facilitating some improvement in cohesion.

Cohesion would also be improved if all three pillars were regularly presented in terms of the indexed annuities they could generate. From about age 50, people should be able to review their likely retirement incomes from pillars 2 and 3, and to use modelling tools to assess likely eligibility for pension. This would assist planning in the period ahead of retirement, including about whether additional pillar 3 savings would be appropriate and about the appropriate balance between superannuation and home savings.

This is a summary of Andrew Podger and Michael Keating’s submission to the Retirement Income Review. Their full submission is available here: https://treasury.gov.au/sites/default/files/2020-01/csri150120.pdf. Andrew and Michael were both foundation members of the Committee for Sustainable Retirement Incomes (CSRI), an independent, non-partisan, non-profit think tank whose mission is to progress the development and implementation of policies to further the goal of encouraging “adequate incomes through all the years of retirement for all Australians on a fair and fiscally sustainable basis”.

Recent Comments