The final report of New Zealand’s most recent Tax Working Group was released in February 2019. The recommendations were dominated by two proposals: to introduce a comprehensive capital gains tax into New Zealand; and the more targeted use of environmental taxes. While environmental taxes have made it to the work programme of policy makers, capital gains tax was rejected by the Government. New Zealand remains without a comprehensive capital gains tax, and with no prospect of one in the near future.

The Tax Working Group, appointed by the New Zealand Government, used a traditional tax assessment framework to guide the process of evaluating the current tax system for structure, fairness and balance. This is consistent with previous tax reviews and based upon the canons introduced in 1776 by Adam Smith: equity; efficiency; convenience; and certainty.

In addition, the Working Group applied the New Zealand Government’s new multi-dimensional wellbeing framework, developed by the Treasury, the Living Standards Framework. The Tax Working Group took the framework and adapted this to incorporate Māori concepts of wellbeing and developed a new integrated framework, He Ara Waiora, to make their evaluations.

My recently published journal article considers how these tax assessment frameworks have influenced the conclusions reached and recommendations made by the Tax Working Group, compared to its predecessors in New Zealand over the past six decades. I argue that the frameworks have influenced the outcomes of the groups.

Previous tax reviews in New Zealand

The comprehensive tax reviews in New Zealand held since the 1960s, including Ross (1967), McCaw (1982), McLeod (2001) and Victoria University of Wellington (2010) applied Smith’s traditional criteria to assess the tax system. They had a primary focus on tax policy principles of equity and efficiency.

The McLeod (2001) and Victoria University of Wellington (2010) reviews, extended the canon of ‘efficiency’ to include encouraging economic growth and not just neutrality. The result of this is both groups recommended regressive tax policy to stimulate economic growth.

The earlier reviews, Ross (1967) and McCaw (1982) focussed more intensely upon issues of equity. Many of the recommendations they made had a view toward creating greater fairness in a system that was notoriously unfair. The tax base grew very narrow during the 1970s and early 1980s so broadening the tax base and reducing unjustified tax breaks drove the recommendations during this period.

The 2019 Tax Working Group: a strong emphasis on intergenerational wellbeing

Fast forward to 2019 and He Ara Waiora and the Living Standards Framework is used alongside the traditional frameworks in the Tax Working Group’s evaluation of the tax system.

The Living Standards Framework was developed to assist policy developers with the aim of achieving higher living standards for New Zealanders, and an overall goal of intergenerational wellbeing. Intergenerational wellbeing includes current wellbeing and future wellbeing, measured using indicators of stocks of ‘capital’. These stocks include natural capital, human capital, social capital, and financial and physical capital (see Figure 1).

Figure 1: New Zealand Treasury’s Living Standards Framework

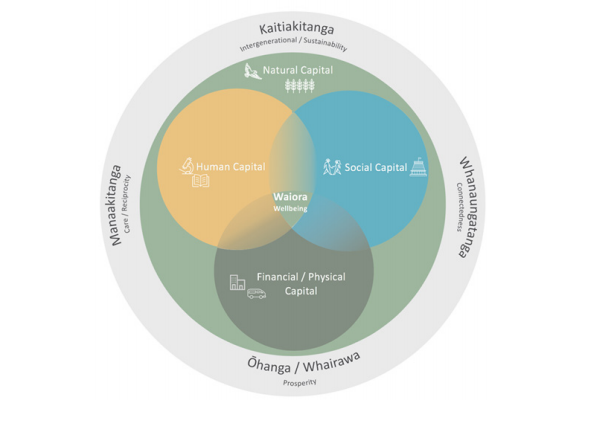

The Tax Working Group further adapted the Living Standards Framework to incorporate Māori concepts of waiora (wellbeing) and the integrated framework He Ara Waiora, which is illustrated in Figure 2.

Figure 2: He Ara Waiora

Thus, the recommendations for capital gains tax and environmental taxes

My research finds that the use of the Living Standards Framework (and its adaptation to He Ara Waiora), caused a greater emphasis on equity and sustainability in the Working Group, which led to the recommendations for a comprehensive capital gains tax and environmental taxes.

The concept of ‘natural capital’ recognises the need for a healthy natural environment to support human activity in the future. While this may be something we have always known, putting it on the policy framework requires that environmental issues are considered as important as building and protecting human, financial and physical capital.

Tax is a lever for governments to change behaviours through creating incentives or disincentives for action. The Tax Working Group proposed that improvement in New Zealand’s stocks of natural capital could be achieved through targeted tax measures. This has been accepted in principle by the government and added to the tax policy work programme.

With regard to the recommendation that New Zealand ought to implement a comprehensive capital gains tax, the Tax Working Group formed this view with fairness, social capital, and productivity in mind.

Concerning fairness, the group point to the regressive nature of New Zealand’s tax system and the effect that failure to tax capital gains has upon growing inequality. Capital gains tend to be derived by asset owners meaning any tax benefits favour the wealthy. This has the result of increasing inequality which runs counter to the objectives of the Living Standards Framework. The framework emphasises the importance of distribution of outcomes across the population.

Social capital refers to the social connectedness, values and trust within a society. Social capital has a direct impact upon people’s willingness to contribute to the tax base. The Tax Working Group point out the importance that taxpayers have a perceived sense of fairness in relation to the tax system to preserve social capital. They argue the failure to tax capital gains on a comprehensive basis is unfair and challenges the integrity of the tax system.

The Tax Working Group also concluded that failure to tax capital gains is contrary to Adam Smith’s canon of efficiency, particularly with regard to tax neutrality. Business investment in New Zealand is heavily weighted into industries where untaxed capital gains make up a large proportion of total income, resulting in distortion of investment choices. The Tax Working Group even state that the activities of these privileged industries are subject to taxpayer subsidisation.

Frameworks matter for tax policy

Although all the previous tax working groups used a traditional tax assessment framework, mainly focussed upon equity and efficiency, they reflect the issues of the time. We may reflect upon the 2019 Tax Working Group in the same way. The Living Standards Framework and its adaptation into He Ara Waiora were important in the recommendations of the Tax Working Group.

Editorial note: This post is part of a special series to mark the anniversary of the release of the final report of New Zealand’s Tax Working Group and to assess its findings. The final report, Future of Tax, was released on 21 February 2019. The Group, chaired by former New Zealand Finance Minister Michael Cullen, was established by the Government of New Zealand in 2017 to consider the future of the New Zealand tax system. It was the latest major tax review after reviews in 2001 and 2010. Discussion papers and submissions to the Working Group are available at the website: https://taxworkinggroup.govt.nz/.

Further Reading

Pavlovich, A 2019, ‘Striving for intergenerational wellbeing’, Journal of Australian Taxation, vol. 21, no. 2, pp. 15-33.

New Zealand’s Tax Working Group series

Māori Perspectives in the New Zealand Tax Working Group Report: Tikanga or Tokenistic Gestures? By Matthew Scobie and Tyron Love.

The Tax Working Group and Capital Gains Tax in New Zealand — A Missed Opportunity?, by Andrew Maples and Sue Yong.

The Tax Working Group and the Circular Economy: Context and Challenges, by Jonathan Barrett and Kathleen Makale.

Recent Comments