A vast literature across the social sciences and humanities studies the impact of historical colonial rule. However, less scholarly attention has been devoted to the consequences of the decolonization process that unfolded in the mid-twentieth century. Our paper uses a dataset on the fiscal history of African countries from 1900 to 2015, recently constructed by Albers, Jerven, and Suesse (2023), to analyze the impact of decolonization on fiscal capacity.

What is fiscal capacity?

Fiscal capacity is an important component of the broader notion of state capacity, which is the focus of increasing attention as a crucial precondition for economic development. In particular, fiscal capacity provides an aggregate measure of the degree to which a state has the administrative ability to tax its citizens, and hence the potential to provide public goods conducive to economic development, such as infrastructure and schooling.

We define fiscal capacity in our analysis in terms of the revenue raised from taxes that are relatively difficult to collect and that require more sophisticated administrative infrastructure; this includes, for instance, income taxes and broad-based consumption taxes, but excludes import taxes and mining royalties.

Specifically, we construct a measure of fiscal capacity in units of wage days (i.e., the number of days that a typical urban worker must work to earn an amount equal to nominal tax revenue per capita). This measure is thus independent of changes in the local currency and can be computed even when GDP data is unreliable or nonexistent.

We combine this measure of fiscal capacity with information drawn from historical sources on the year of decolonization for each country in the sample, along with a broad range of covariates. “Decolonization” is defined in our primary analysis as national independence – i.e., sovereignty under international law; however, we also use an alternative definition based on self-government under African majority rule.

How we estimate the impact of decolonization

Our analysis uses a staggered difference-in-differences design, as countries experienced decolonization at different times (albeit with a substantial cluster in the 1960s). This design is implemented using a stacked event study approach. This entails compiling a series of mini-datasets (“stacks”) to construct a stacked dataset. Each stack consists of all countries that were treated (i.e., experienced decolonization) in a particular year, along with a set of control countries that never experienced decolonization within the sample period.

While data is available up to 2015, we truncate the sample period to 1900-1970 and use the former Portuguese colonies of Angola, Guinea-Bissau, and Mozambique (which experienced decolonization late, in the mid-1970s) as control countries that are “never-treated” over this (truncated) sample period.

When we instead conceptualize decolonization as the transition to African majority rule, we also include countries in southern Africa that experienced late transitions to majority rule (1980 for Zimbabwe, 1990 for Namibia, and 1994 for South Africa) in the control group.

Decolonization increased fiscal capacity

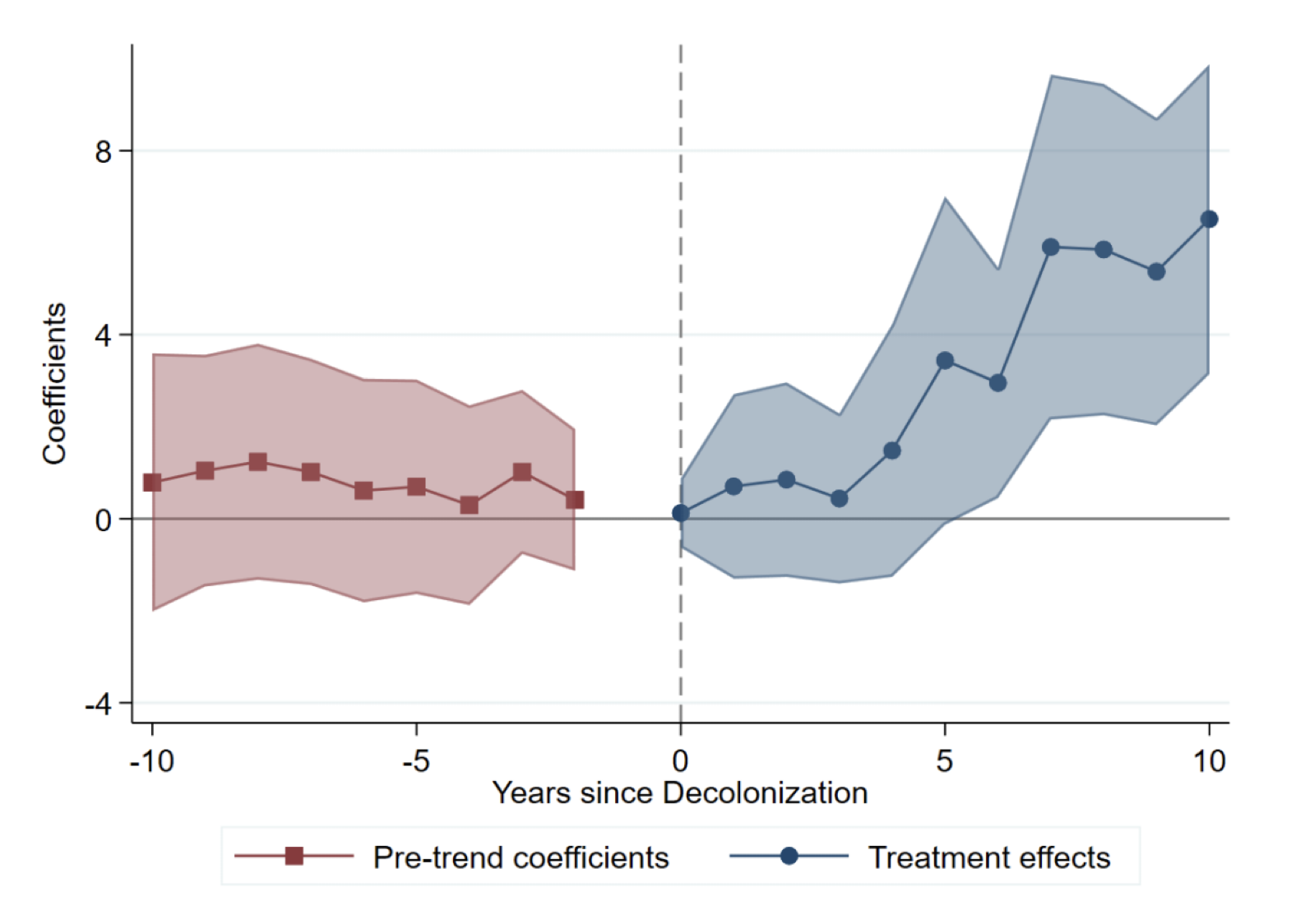

Our primary result is that there was a substantial increase in our measure of fiscal capacity starting about five or six years after decolonization, with no discernible pre-trends prior to decolonization. This result is illustrated in the figure below, where revenue is measured in labor-days.

Fiscal capacity ten years after decolonization is about six to seven labor-days higher than under colonial rule, relative to a mean of about eight labor days in the year before decolonization. Therefore, this represents a substantial effect. The length of the lag – while substantial – appears to be consistent with the time required to undertake significant investments in administrative capabilities to increase fiscal capacity.

This result – which implies substantial state-building activity in postcolonial Africa – is robust to tests for a variety of alternative explanations, including:

- The role of forced labor in the treatment and control countries

- The diffusion of the value-added tax (VAT)

- The potential role of state-owned enterprises (SOEs) and non-tax revenues

- Changes in fiscal centralization

- The impact of armed conflict, coups, high inflation episodes and debt default

- Access to aid and loans

- Changes in commodity export prices.

It is also robust to the use of alternative control groups, and the use of generalized synthetic control methods instead of a stacked event study.

Why did fiscal capacity rise after independence?

A natural potential mechanism for this effect is democratization. However, we are able to rule out this channel. Decolonization did not generally lead to a substantial increase in the prevalence of democracy; even where it did so, we show that fiscal capacity did not change disproportionately. Moreover, subsequent (post-independence) democratization events in Africa are not associated with increases in fiscal capacity.

We therefore posit a conceptual framework that focuses on “tax morale”. In this framework, compliance by taxpayers depends in part on the perceived legitimacy of the state. Thus, tax morale may be lower, and resistance to taxation greater, when the rulers who impose taxation are foreign and perceived as lacking legitimacy. This may lead colonial regimes to impose low effective tax burdens in equilibrium (taking into account enforcement expenditures). Tax morale may increase upon decolonization to the extent that postcolonial governments are perceived as having greater legitimacy; this would lead to higher taxation and enforcement, and thus fiscal capacity, in equilibrium.

To the extent that legitimacy depends on the perceived similarity of ruling elites to the general population, the degree of increased legitimacy upon decolonization may depend on the extent to which the new ruler is ethnically representative of the population. We thus code the ethnicity of post-independence leaders and construct a measure of the ethnic representativeness of these leaders in relation to the national population.

The change in rulers’ ethnic representativeness at independence (which typically involved a transition from European to African rulers) explains much of the baseline effect of decolonization. Thus, ethnic representativeness can be interpreted as a channel through which the legitimacy effect operates.

Conclusion

Overall, our results suggest that, for the first decade at least, independent African governments were able to substantially invest in state-building, and we conclude that the legitimacy channel is the one that best explains this finding. These results shed new light on the consequences of colonial rule and decolonization, and on the determinants of variation in governments’ fiscal capacity in the present day.

References:

Albers, T. N., Jerven, M., and Suesse, M. (2023). The fiscal state in Africa: Evidence from a century of growth. International Organization, 77(1):65–101.

Citation

Dhammika Dharmapala and Marvin Suesse “Decolonization, Legitimacy and Fiscal Capacity: Event Study Evidence from Africa” CESifo Working Paper No. 12059. Available at: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=5392936

Recent Comments