This Election Brief summarises the key tax policies, costings and revenue estimates of the incumbent Liberal-National Coalition (LNP) Government, the Australian Labor Party (ALP), and the Australian Greens, announced before or during the election campaign. We benchmark the tax policies against the original aspirations of the Henry Tax Review and against the fiscal challenges identified in the Pre-Election Fiscal Outlook Statement issued jointly by the Secretaries of Treasury and Finance (PEFO). These parties’ policies have been presented because they are the ones which are most likely to form a government, or to have an influence on government policy, after the election. They are also the parties with the most comprehensive tax policies to compare.

The 2016 federal election has sometimes seemed to be all about tax, while at other times, tax policies have disappeared from the radar. Neither the Treasurer (LNP) nor Shadow Treasurer (ALP) has been willing to commit to big picture tax reform after the election and they are not seeking a mandate based on achieving “tax reform”. This is in spite of the Re:Think Better Tax process initiated by the Abbott-Hockey government, or the Henry Tax Review initiated by the previous Rudd-Swan Labor government. Yet, the election and the budget before it include a number of fairly significant tax policies.

Fiscal sustainability and budget repair

Tax policies must be considered in the context of the fiscal deficit Australia has had since the Global Financial Crisis, now in its eighth year. The PEFO Statement required by the Charter of Budget Honesty, estimates a peak in the deficit of $37.1 billion (2.2% of GDP) for the 2016-17 year. This is forecast to improve to a deficit of $5.9 billion (0.3% of GDP) in 2019-20 and small surpluses after that.

The LNP’s updated costings plan of 28 June and the ALP’s Fiscal Plan of 26 June illustrate the different weights the two major parties have put on reducing the deficit. There has been some discussion about this during the last week of the election campaign.

The parties have presented tax policies that will have an immediate effect for this electoral cycle and across the usual 4 year Medium Term Expenditure Framework (forward estimates) used in the annual budget. They have also presented policies whose effect will be felt mainly in the future. Tax policies such as the LNP’s proposed company tax cut, or the ALP’s proposed tightening of negative gearing and capital gains tax, have fiscal costs and revenues estimated over 10 years. The focus on the longer term is positive but it makes estimating fiscal costs and benefits, and predicting other effects such as on jobs, growth or the housing market, extremely difficult for both experts and the electorate. The future is full of “unknown unknowns” as a former US Secretary of Defence, Donald Rumsfeld, once said.

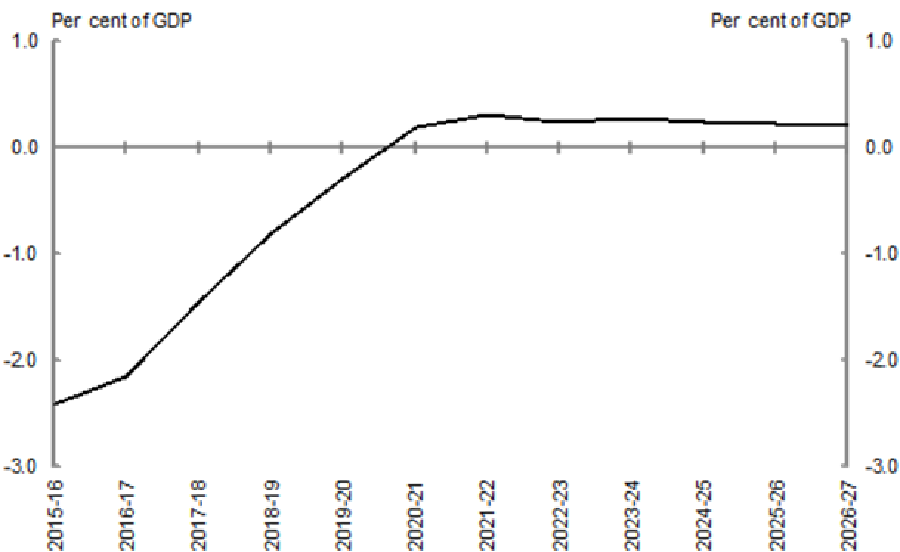

Underlying federal cash balance projected to 2026-27

Source: PEFO, Chart 1.

In the medium term the PEFO Statement is projected to improve to a surplus of around 0.2 per cent of GDP in 2020-21. Net debt in the 2016-17 period is estimated at $326.1 billion (18.9 per cent of GDP), increasing to $347.1 billion (19.2 per cent of GDP) in the next financial year and declining as a percentage of GDP thereafter as deficits decrease. The LNP and ALP propose achieving reductions in deficits through a mix of reduced spending and revenue raising measures. How, and in which portfolios, spending or saving may occur has been a major issue in the election campaign.

The PEFO fiscal projection incorporates a tax:GDP cap of 23.9%, a figure based on past federal budget performance. No party has yet seriously examined whether this tax cap is right for Australia in the longer term. The PEFO report identifies serious risks to the Budget if the forecasts prove to be too optimistic in the event of external or domestic shocks. Neither the Government’s, nor the ALP’s, spending and revenue projections leave room for error.

Challenges for tax reform

We summarised the economic and social challenges for Australia – and for tax reform – in our 2015 Stocktake Report. We identified two fundamental concerns about the Australian economy: a lack of productivity growth; and the need to stimulate non-mining investment as the mining investment boom wound down. Other challenges are demographic, including our ageing population; increasing workforce participation; inequality; and adapting to a digital global economy. These challenges remain, and have even strengthened, in the last year.

In our Stocktake report, we also suggested the following principles for tax reform: (1) efficiency – to generate and sustain economic prosperity and wellbeing; (2) fairness, including distributive justice and addressing inequality; and (3) resilience of our tax/transfer system, including simplicity and keeping administrative and compliance costs low and ensuring stability in the longer term.

The primary goal of taxes is to raise revenue for government. The Henry Review set out an aspiration for the future tax base for Australia. It was based on a more comprehensive concept of: personal income; taxing business income, consistent with economic growth; taxation of rents from resources and land; and more comprehensive taxation of private consumption. This was expressed in Recommendation 1 of the Review:

Revenue raising should be concentrated on four robust and efficient broad-based taxes:

> personal income, assessed on a more comprehensive base;

> business income, designed to support economic growth;

> economic rents from natural resources and land; and

> private consumption.

This remains the best guide for tax reform for Australia in future.

The missing tax reforms in this election

Before examining the election tax policies, it is worth noting that some fundamental tax reforms that have been much discussed in the last couple of years are absent from the agenda. These include expanding the base or increasing the rate of the Goods and Service Tax (GST) and the reform of State taxes, such as stamp duty, land tax and payroll tax. The issues of how to improve taxation of consumption in Australia, how to change our State tax settings to support stability in revenues and housing markets and how to secure revenues for the States, have been put aside as too hard.

Reform of the fiscal federal bargain – which needs federal government leadership – is nowhere to be seen, despite talk of state income taxes in months before the election. The federation white paper process has now been halted.

Presentation of policies and fiscal impact

Fiscal costings in the Tables are presented per year; over the 4 year forward estimates period; and over the 10 year medium term, where parties have published this information. The Tables follow the convention of the federal Budget (Revenue measures) and the Parliamentary Budget Office policy costings. A positive number for the fiscal impact indicates an increase in revenue or a decrease in expenditure (with a positive impact on the fiscal balance). A negative number indicates a decrease in revenue (or lower tax) or an increase in expenditure (with a negative impact on the fiscal balance).

Policies were recorded up to 28 June 2016, from political parties’ campaign websites and, in the case of the incumbent LNC Government, from the information about policy commitments presented in the 2016 Federal Budget of 3 May 2016. The policies are summarised in the Tables. In the download-able PDF version, the Tables contain web links to the original source, or sources.

Personal income tax rates, capital gains, negative gearing

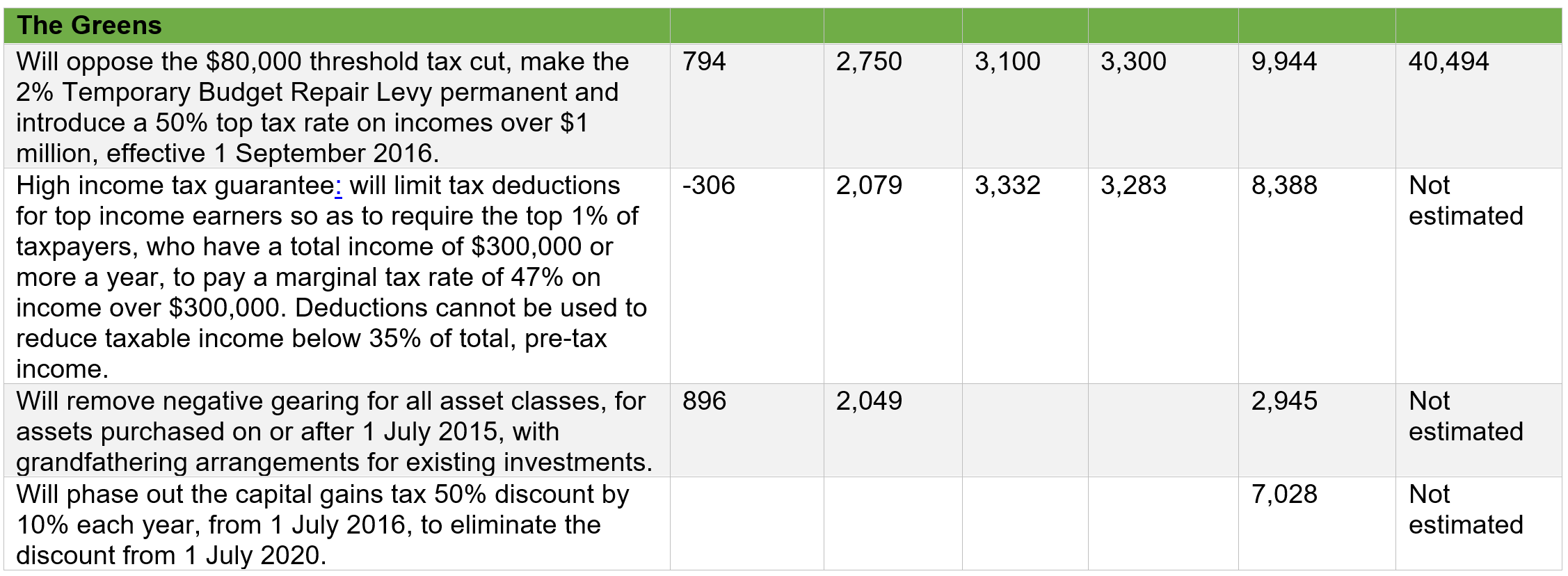

All parties propose some changes to personal income tax rates – albeit in different directions. The LNP proposes a relatively modest tax cut for those at or above average wages, by increasing the 37% tax threshold to offset bracket creep. This has a maximum value of $315 per year for those taxpayers with incomes above $80,000. The LNP will also permit the 3 year Temporary Deficit Repair Levy, enacted under the Abbott-Hockey government which adds 2% to the top marginal tax rate, to expire on 1 July 2017, as per current legislation. The ALP will legislate to retain the Deficit Repair Levy, which in effect becomes a permanent surcharge on incomes over $180,000 under their policy. The Greens support retaining the Levy and propose increasing tax rates on top income earners.

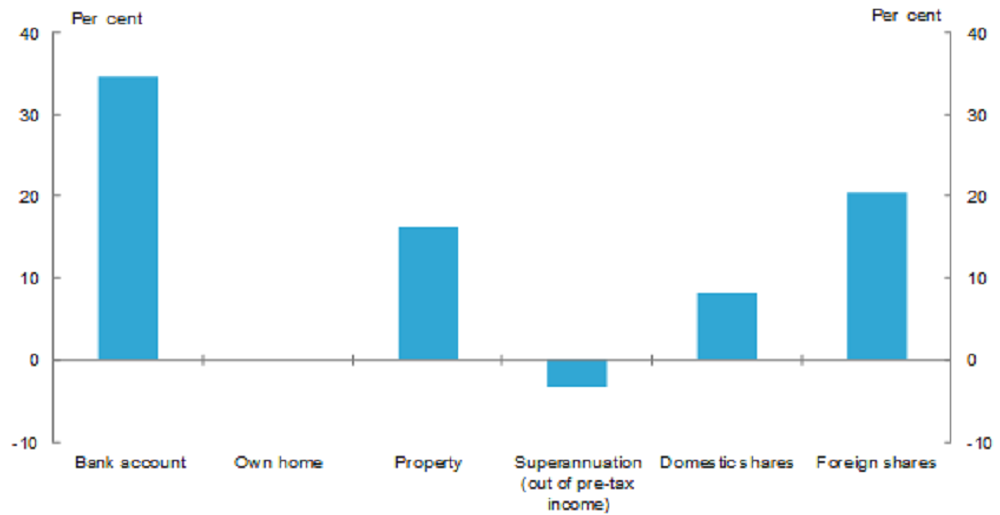

What about the income tax base? The Henry Tax Review identified the wide divergence in tax treatment of different kinds of savings and investment, and this was also highlighted by the Murray Inquiry into the financial system. The after-tax return on various investments and for various tax bracket taxpayers differs widely:

Effective tax rate on investment return for taxpayer on 32.5% marginal rate

Source: Re:Think Tax Discussion Paper (2015), Chart 4.1

All parties propose tightening superannuation tax concessions (see separate discussion below). The LNP does not propose to change any other settings for investment or saving. Both the ALP and Greens would seek to limit negative gearing and tax advantages for rental real estate and to reduce the capital gains tax 50% discount which applies to most investment assets held for more than 12 months.

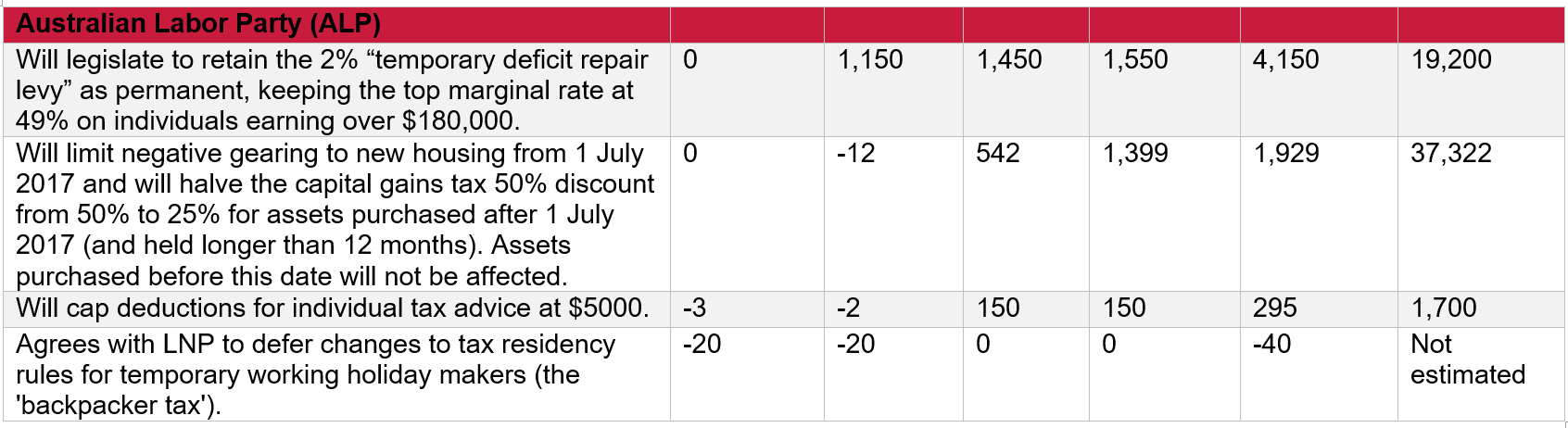

The ALP would restrict new negative gearing to new properties, and halve the capital gains tax 50% discount (to 25%). Both these changes would be ‘grandfathered’—i.e. would not apply to existing assets. This means that the fiscal savings build up slowly, but become significant over the 10 year timeframe used by the ALP. The Greens would end negative gearing and eliminate the CGT discount. The issues are discussed in Ingles and Stewart (2015), where we support placing limits on both negative gearing and the CGT discount to strengthen the income tax base.

There was debate in the final week of the election campaign about how much revenue the ALP’s proposed changes to negative gearing and the capital gains tax concession would raise. The PBO estimated these costs for the LNP policy, finding this would raise around $6 billion a year by 2026-27. This was about $800 million less than ALP’s published figures but with a similar revenue trajectory from 2019-20 onwards. The PBO estimated that about $2.5 billion of this annual revenue would be from reducing the capital gains tax discount and about $3.5 billion from the negative gearing limit. This was the first time a public breakdown had been provided about the estimated split in revenue collections between the two tax measures.

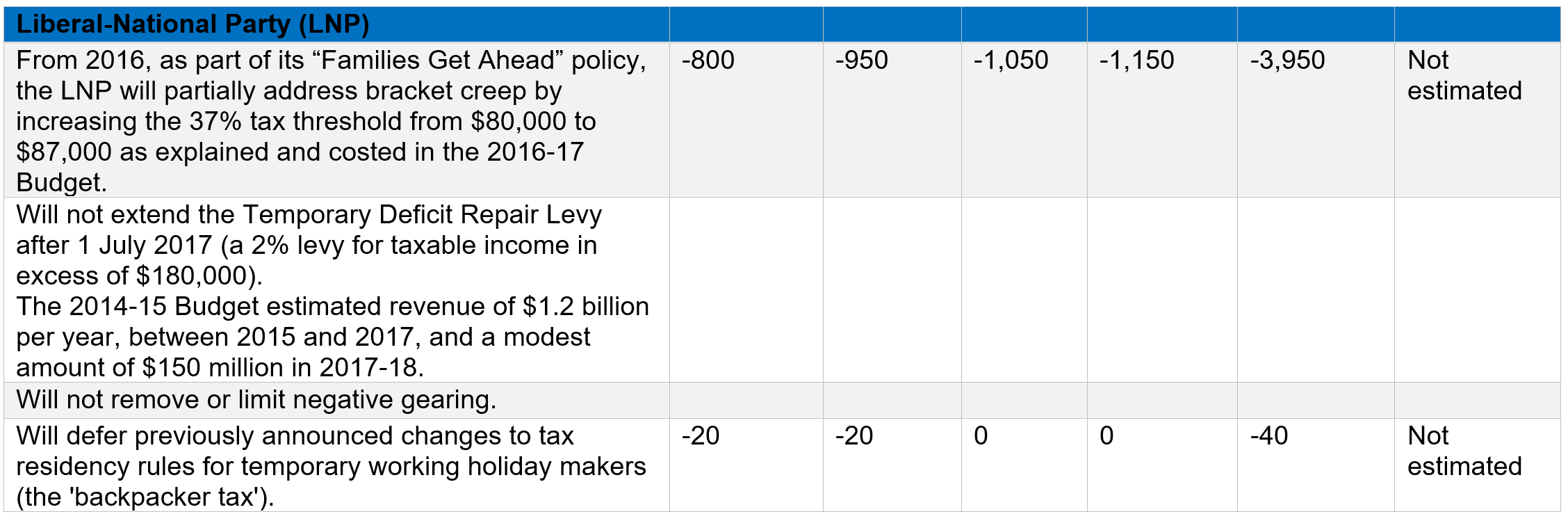

Table 1. Party policies and costings: Personal income tax, negative gearing and capital gains tax concessions

This table containing links to references and notes can be found here.

Superannuation & assistance to the aged

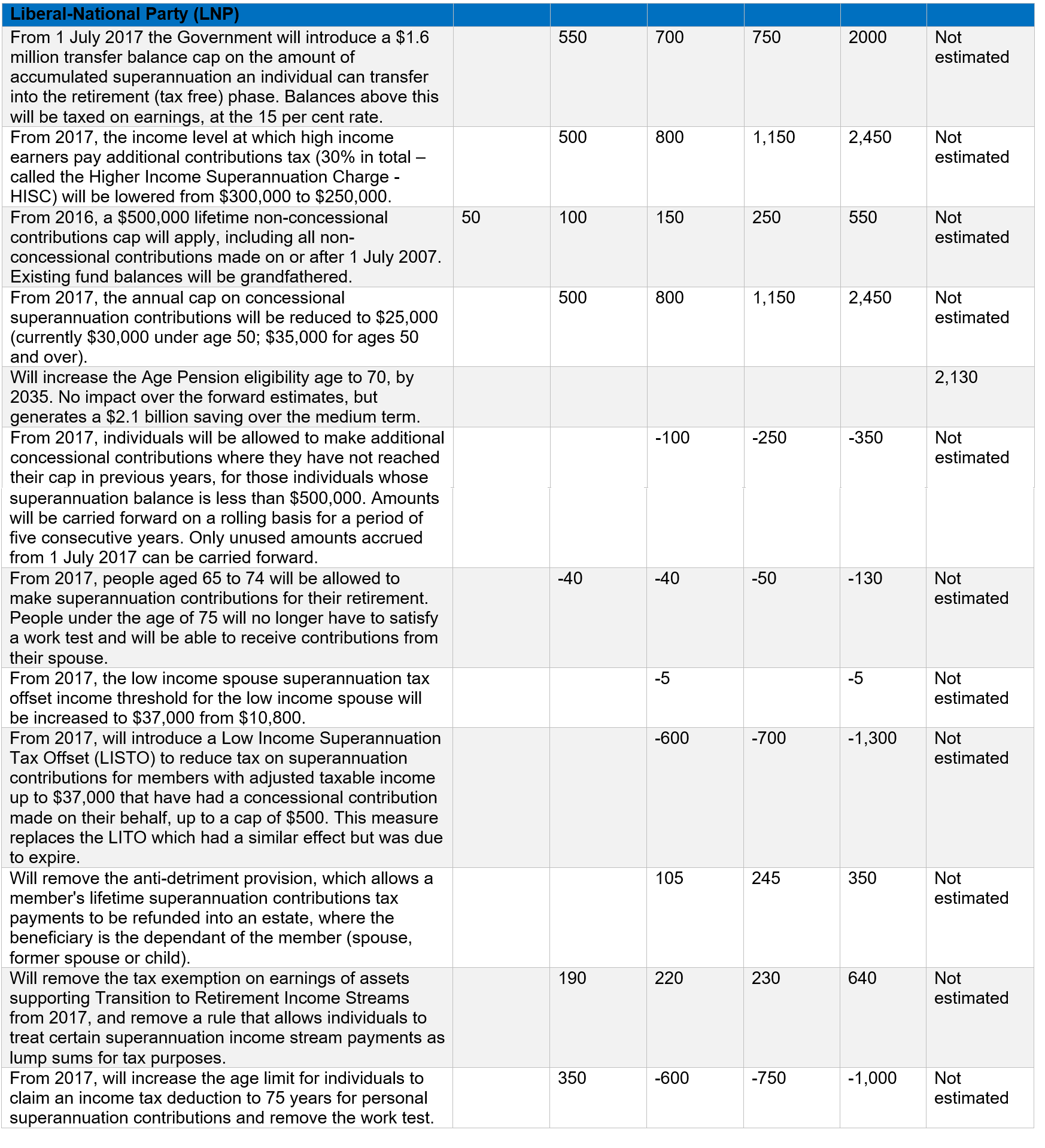

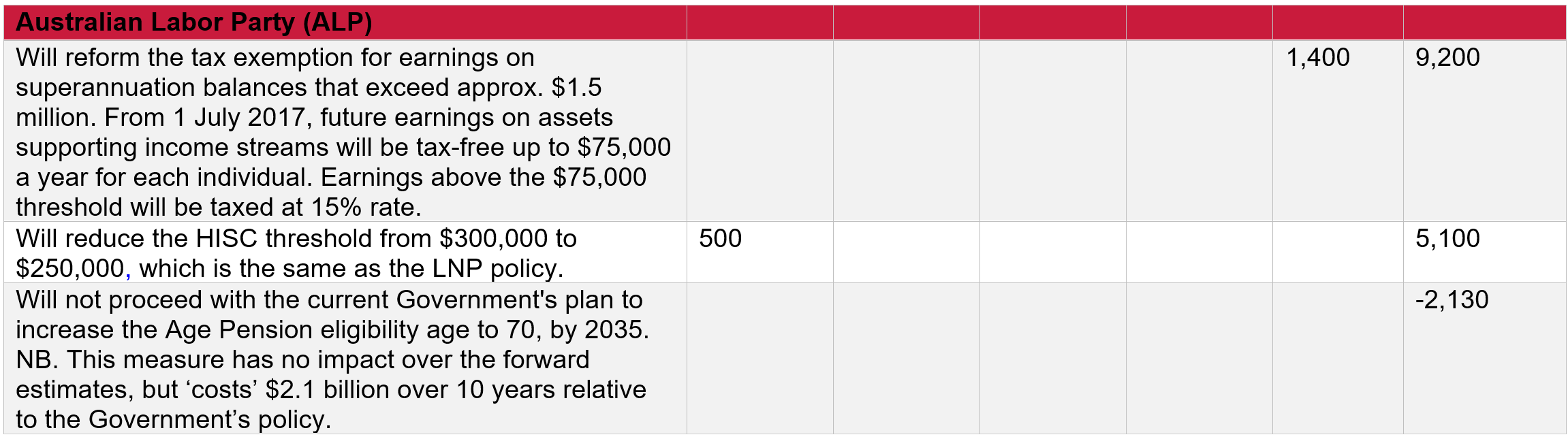

After years of debate, there appears to be a consensus across all parties – although still unpopular in some quarters – that superannuation tax concessions should be limited in some respects. The LNP and ALP have produced policies that look different but will have remarkably similar effects.

In general, the Government’s proposed changes are modest and sensible. They will improve fairness and reduce the fiscal cost of the system somewhat, albeit may add to complexity. The ALP’s policies may have a similar effect; notably the plan to levy some tax on investment earnings during the pension phase and the reduction in the point at which high income earners pay the additional 15% contributions tax, for a total of 30% (Div 293 threshold). These changes move towards the proposals from the Henry Tax Review, although we have argued elsewhere they could go a lot further. None of these policies is actually retrospective, despite such arguments in the media.

All parties propose to retain the age pension at current levels and to continue indexation to wages. The government recently enacted a tightening of the asset means test for the age pension which will commence from 1 July 2017 and which has now been supported by the ALP and Greens. However, it will significantly increase effective marginal tax rates on saving and work by those receiving a part-pension.

There is a major difference between the parties regarding the Government’s proposal to increase the age pension eligibility age to 70 over time, which is not supported by the ALP or Greens.

Table 2. Party policies and costings: Superannuation and pensions

This Table containing links to references and notes can be found here.

Recent Comments