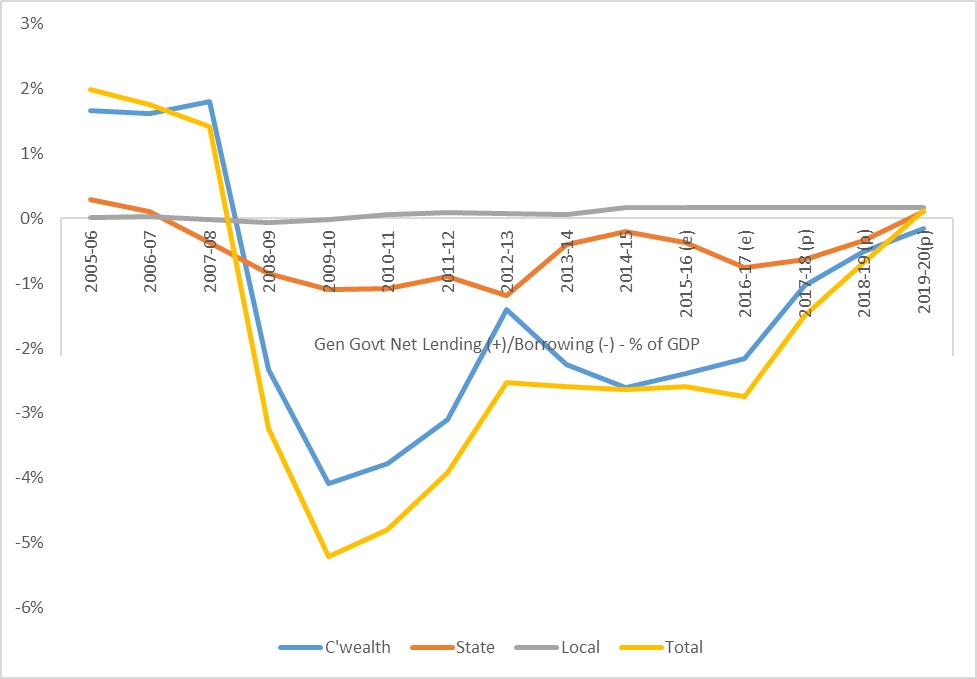

Budgetary issues in Australia have dominated public policy discussion at the federal level since the 2008-10 Global Financial Crisis (GFC). Governments at both national and state level entered the GFC running budget surpluses, yet post-GFC Australia has experienced one of the fastest growing public debt levels in the world due to a series of historically large budget deficits that have persisted for longer than after previous economic downturns (see Figure 1).

Figure 1 – Australian, state and local government budget balances

Source: Makin and Pearce (2016) and ABS sources cited therein.

The Federal Government has overwhelmingly contributed to the escalation of Australia’s public debt because it has run more sizeable deficits than State Governments and been much less successful in reducing them.

Australia’s public debt to GDP ratio at around 30 per cent may not be high by OECD standards. However, not only has it been amongst the fastest growing in the world, it is mostly (around two thirds) owed to foreigners, unlike in other advanced economies. Foreign public debt also now comprises a sizeable component of Australia’s total private plus public foreign debt, which stands at over 55 per cent of GDP in net terms.

Key questions in the fiscal deficit and debt debate are:

1. Is higher federal spending or lower tax revenue driving the deficits?

2. What are the macroeconomic risks of ongoing federal budget deficits?

3. What level of public debt is optimal for Australia?

4. What fiscal consolidation is needed to stabilise and reduce Australia’s public debt?

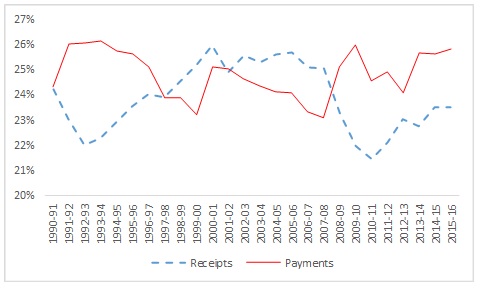

This article briefly addresses these questions. In response to the first, Federal Government spending at 26 percent of GDP is running above its long run average since 1990 of 25 percent, while revenue remains slightly below its long run average of 24 per cent (see Figure 2). Hence both are contributing to the ongoing deficits, although expenditure more so.

In answer to the second question, the main risk of failing to rein in the fiscal deficit is a downgrading of Australia’s AAA credit rating, which would add a risk premium to interest paid on government bonds. A 30 basis point rise in interest paid on government debt, for instance, would increase the annual federal public debt interest bill by some $1.5 billion, other things the same.

Figure 2 – Federal Government revenue and payments (percent of GDP)

A credit rating downgrade would disrupt the whole interest rate spectrum, most notably increase rates paid by State Governments and the big four commercial banks on their overseas borrowings. This would ultimately raise mortgage and commercial loan rates throughout the economy, damage business and household confidence and slow private investment and consumption.

World interest rates are also highly likely to rise by at least as much as any risk premium in the near future which would compound the problem, further increasing public debt interest paid abroad.

The third and fourth questions above have been addressed directly in our paper ‘Fiscal Consolidation and Australia’s Public Debt’ published in the Australian Journal of Public Administration. Our paper highlights the Federal Government’s deteriorating balance sheet, as measured by the difference between its public assets and public debt.

It also stresses the increase in foreign public debt on the liabilities side of the government balance sheet, given that servicing foreign public debt directly drains national income by close to $11 billion a year and rising. Additionally, it reminds that the Federal Government is supposed to achieve budget surpluses on average over the course of the economic cycle according to the Commonwealth Charter of Budget Honesty 1998.

Based on the principle that public debt can only be reduced by running budget surpluses that enable debt retirement, the paper exposits a methodology for estimating the size of the federal budget surpluses required to reduce federal public debt to targeted levels. The formula-based approach focuses on the key drivers of public debt sustainability (via interest rates, economic growth and the magnitude of the debt itself) to estimate what federal budget balances are needed to achieve optimal debt targets.

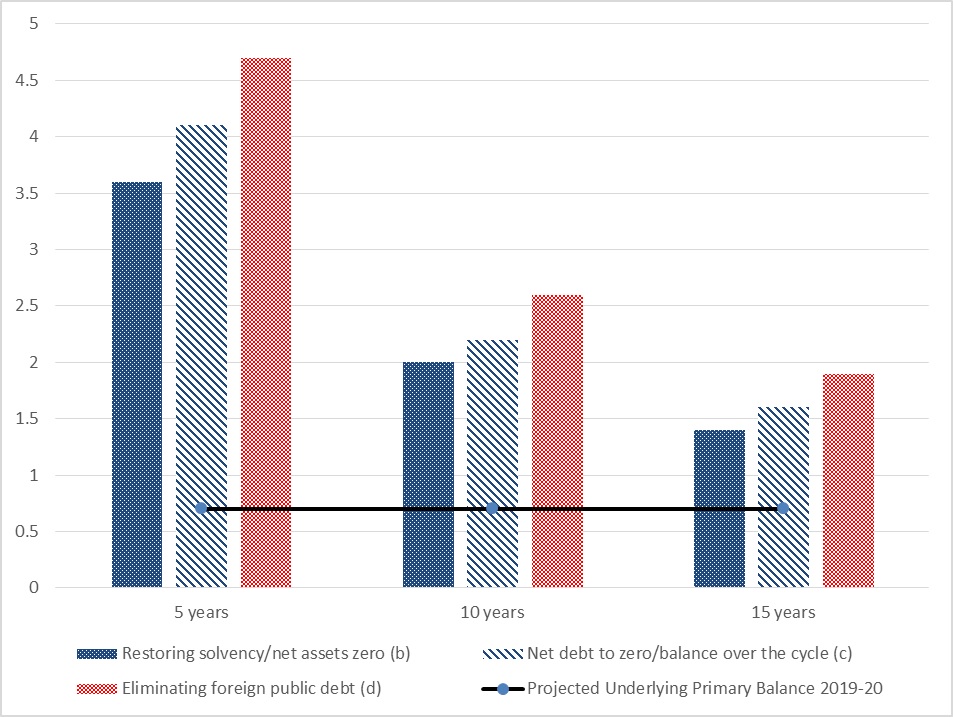

More specifically, Figure 3 from the paper shows what budget surpluses are required to bring public debt down to targeted levels that (i) restore the Federal Government’s net worth to zero; (ii) restore net debt to a level consistent with balancing the budget over the cycle; and (iii) eliminate foreign public debt – each within 5 years, 10 years and 15 years. Higher budget surpluses are obviously required to attain the public debt targets the shorter the time frame. Yet even in 15 years’ time Treasury’s currently projected budget balances are around half those required to reduce public debt to the target levels.

Figure 3 – Budget surpluses required for targeted public debt levels

Source: Makin and Pearce (2016)

For instance, to restore Federal Government net worth within 10 years, budget surpluses would persistently have to run at 3.6% of GDP for 5 successive years, or 2% of GDP for 10 successive years. To eliminate foreign public debt, primary budget surpluses would persistently have to run at 4.7 % of GDP for 5 years, or 2.6% for 10 years. To balance the federal budget over the cycle, primary budget surpluses would persistently have to run at 4.1% of GDP for 5 years or 2.2% for 10 years, over twice the budget balance projected by Treasury on current budget settings.

In short, we find that substantially higher budget surpluses are needed to meet the specified public debt targets. Of concern is that no target debt to GDP level consistent with the optimal levels of public debt will be met into the foreseeable future under existing fiscal settings.

References

Makin, A. and Pearce, J. (2016) ‘Fiscal Consolidation and Australia’s Public Debt’ Australian Journal of Public Administration (forthcoming)

Given our extraordinary levels of private debt, how can public debt *not* keep increasing? May either be studied in isolation from the other? Does not focusing on curbing public debt serve to exacerbate private debt and invite sharp deflation in our current situation?

Well said

To some extent I agree with Bryan’s previous comment. However I believe the states and territories certainly are less able to sustain deficits than the Federal government. In a time of rising private household debt, due to low wage growth and weak private investment Federal governments need to spend to keep up aggregate demand. It is obvious now in 2016 to many business people and non-economists that Federal governments that have a fiat free floating currency, don’t need to worry about deficits when the economy is flat and inflation is not growing.

Thanks for your article but we don’t have a public debt problem. Your focus is badly misplaced,

Yes, I agree that the states and territories have less ambit for continued public debt, Wayne, but Federal surpluses are a rare thing and may only be maintained in the very best of economic times. Otherwise, surpluses will come at a severe cost to all Australians, and we need to disabuse politicians of all stripes that we should be aiming for budgetary surpluses in straitened circumstances such as these. It’s a *terribly* false aim.

I wouldn’t say that the Public depth is such a problem, Australia has a government debt of only 23.3% of the country’s Gross Domestic Product