Editorial Note: This is an edited version of the keynote address by the Parliamentary Budget Officer Jenny Wilkinson at the launch of the Open Budget Survey for Australia at the Crawford School of Public Policy, ANU, on 20 March 2018. The original text is available at the PBO website.

I am very pleased to be here today at the launch of the Open Budget Survey. This survey has been running since 2006, and in 2017, for the first time, Australia participated in it. The Tax and Transfer Policy Institute was instrumental in having the survey conducted for Australia.

Surveys like these are useful—to focus the debate on important issues and provide international benchmarks and comparators for performance. Like all international comparisons, however, they have their strengths and weaknesses. I note that while there is a reference in the report to the Parliamentary Budget Office (PBO), the structure of the survey doesn’t really capture how independent fiscal institutions are contributing to increasing transparency, and I hope this will be incorporated in future updates.

Miranda will have more to say about the survey, but I would like to take this opportunity to commend the TTPI for supporting this initiative. It encourages governments to operate openly and transparently, which I think supports better public policy making.

I will spend the rest of my address explaining how I think independent fiscal councils generally, and the PBO in particular, have contributed to an increased focus on fiscal issues, and have improved the transparency of the debate around fiscal matters.

Rise of independent fiscal authorities

Over the past decade, the number of independent fiscal authorities around the world has increased rapidly. In 1990 there were six in place and now there are around 40. We are regularly contacted by countries or jurisdictions who are considering establishing an independent authority to discuss our experience.

This growth has been driven by a range of factors. In the UK, the Office of Budget Responsibility was established in 2010 following a perception that the UK government had systematically generated over-optimistic fiscal forecasts and continued to move its fiscal targets. In Europe, the EU mandated the establishment of independent fiscal councils in 2011 to complement new fiscal rules that were introduced in the aftermath of the global financial crisis. In Australia, a commitment to establish a PBO formed part of the agreement negotiated between political parties and independent members of parliament after the 2010 federal election and we were formally established in 2012.

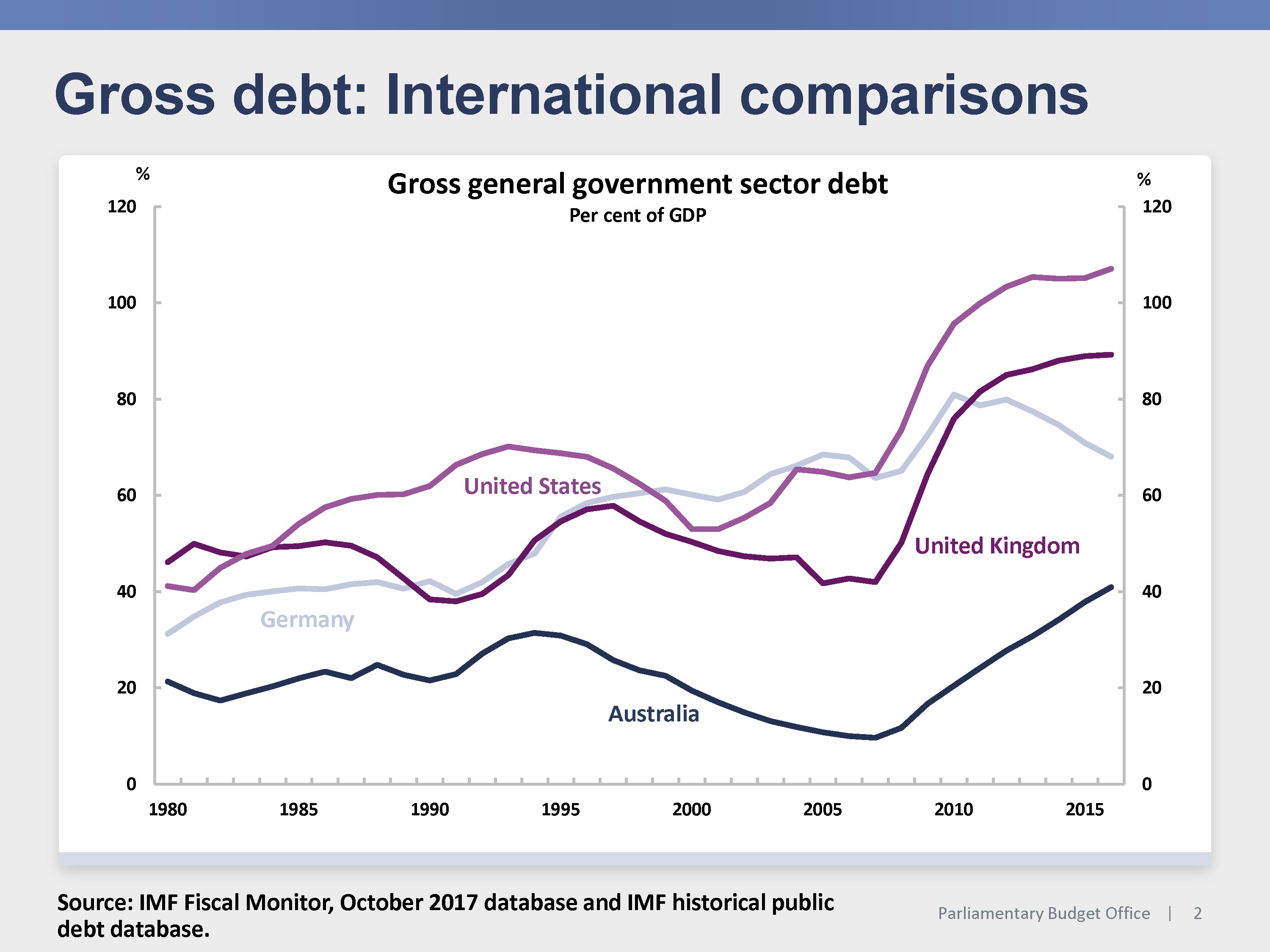

A common driver across countries has been concern over the significant increase in government debt that has occurred across many countries since the global financial crisis, and therefore a need to increase transparency around budget-related issues. (Figure 1)

Figure 1

The genesis of each authority has determined, to some extent, the mandate for that authority. This has led to quite different mandates.

Some independent fiscal authorities have a primary responsibility to monitor compliance with the government’s fiscal rules. Some assess the government’s macroeconomic and/or fiscal forecasts. Some are responsible for setting the forecasts themselves. Some have a role in independently assessing the fiscal cost of policy proposals. They have widely varying budgets and staffing profiles (Figure 2).

The diversity in roles and mandates for these new institutions is strikingly different from those of another independent economic institution—the independent monetary authority. Independent monetary authorities are now ubiquitous and, to a very significant degree, have commonality in their roles and mandates. Almost all have a mandate to maintain inflation at or near a publicly announced numerical target at a low single digit level—and almost all have independence over the setting of interest rates or other instruments to achieve their outcomes.

Figure 2

It is going to be fascinating to see whether there is convergence in the roles and mandates of independent fiscal authorities over time. I think this will depend, in part, on assessments about the effectiveness of different mandates, governance structures and designs of these bodies. It will be important that academic work contributes effectively to these debates.

While there is diversity across independent fiscal authorities, there are also some common elements. Almost all of these new fiscal authorities are:

- explicitly independent of government, and non-partisan

- charged with increasing transparency around fiscal issues

- expected to focus on fiscal sustainability in both the short and medium-term.

This means that they independently analyse and release research on fiscal and budgetary issues, operate openly and transparently, and, through this work, contribute to important fiscal debates which are relevant to the welfare of current and future generations.

PBO: the Australian experience

I will turn now to the Australian experience. The PBO is now near the end of its sixth year in operation. Our mandate comprises three main elements, which are to:

- improve the transparency around, and public understanding of, fiscal and budget policy issues

- level the playing field by providing confidential costing and budget analysis services to all parliamentarians throughout the parliamentary term

- release a post-election report that shows the fiscal implications of major parties’ election commitments.

While we clearly have a role to hold the parties to account in respect of their election commitments and we independently analyse and publish papers on budget issues, particularly the medium-term fiscal projections, it is our costing role that stands us apart from most other independent fiscal authorities.

I think that others have a lot to learn from the constructive contribution to fiscal rectitude that this part of our mandate plays. There is very high demand from parliamentarians for these costing services—across all political parties. Last year, for example, we responded to over 1,800 requests for costing or budget analysis.

While it was initially expected that demand for these services would be focused around election periods, our experience has been that there is an ongoing, strong level of demand throughout the parliamentary term. This demonstrates that the establishment of the PBO has effectively supported an ongoing policy development and announcement process within opposition parties, rather than leaving much of this activity to election campaigns.

The fact that we are available to provide these services has had a number of implications.

- It has established a new norm that the fiscal implications of policy proposals are considered as part of the policy development process.

- It has assisted parties develop well-specified policies, as a policy has to be well-specified in order to be costed.

- It has provided more transparency around existing government programs, as budget analysis about existing programs can be provided.

- It has encouraged more of a focus on the medium-term fiscal implications of policy proposals. Since April 2017 every costing we have conducted provides an estimate of the cost of the proposed policy over the next 10 years.

- Overall, it has largely removed debate around the veracity or otherwise of the fiscal costs of policy proposals, enabling debate to focus on the merits of the policy itself.

I would argue that this role for the PBO has materially improved the quality of the public policy debate and has ensured that fiscal implications are given appropriate attention in these debates.

In the context of the Open Budget Survey for Australia, I think it has improved public participation in the budget process because it has provided the tools for all parliamentarians (who, of course, represent the people in their electorate) to engage in the policy debate. It is not unusual for us to cost a policy for a parliamentarian which is exploring a matter that one of their constituents has raised directly with them.

Beyond our costing role, the PBO has also endeavoured to make a significant contribution to improving transparency around fiscal issues. In part, we have done this through information papers which try to explain clearly and transparently some conceptual issues such as what a costing actually is, how it is calculated, and what it does and does not take into account.

In part, we have improved transparency by establishing ourselves as an independent authoritative voice on fiscal matters. Our independence was established in our legislation, but has been demonstrated by our publication record and by the way we operate.

Some of the important contributions that we have made have included:

- the development and publication of estimates of the structural budget balance, which have subsequently been adopted and published by the Government in all budget updates

- the publication of scenario analysis over the medium term to demonstrate the sensitivity of different parts of the budget to alternative assumptions around key economic parameters, which also preceded additional scenario analysis being published in budget updates

- analysis of significant areas of government expenditure, such as Medicare and the Disability Support Pension (DSP)—improving the public understanding of medium-term pressures on these large programs

- analysis of ‘off budget’ programs such as the Future Fund and the Higher Education Loan Program (HELP)—to provide more transparency around the fiscal impacts of these types of programs.

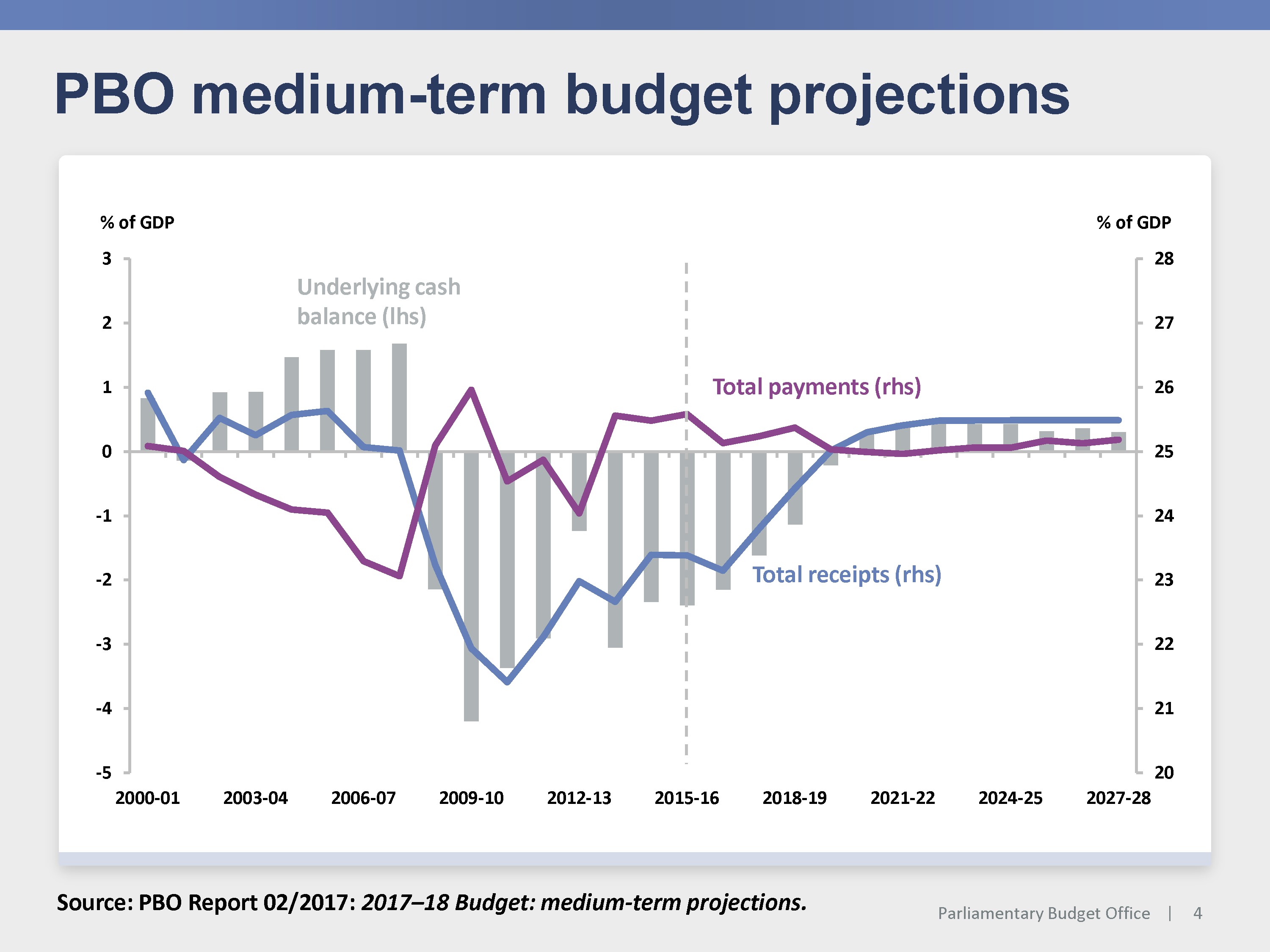

One of our most important contributions to fiscal transparency is the publication of the medium-term fiscal projections report. This analyses the projections for the budget balance, and for the major revenue and expenditure heads over the next ten years. While the budget papers have, since 2009–10, published an estimate of the medium-term projection for the underlying cash balance and net debt, there is typically not a lot of detail published around these estimates. Our reports provide independent projections of the medium-term budget position, highlighting how the underlying components are contributing to these projections, and identifying risks around them.

In the most recent medium-term report, published after the 2017–18 Budget, we noted that:

- under current policy settings, the underlying cash balance is projected to return to surplus in 2020–21 and maintain surpluses of around 0.3 per cent of GDP over the projection period, and net debt as a percentage of GDP is projected to peak in 2018–19 before declining thereafter—which places Australia in a much stronger fiscal position than many other countries

- the projected return to surplus is driven by a significant increase in total receipts and a small decline in payments as a percentage of GDP (Figure 3)

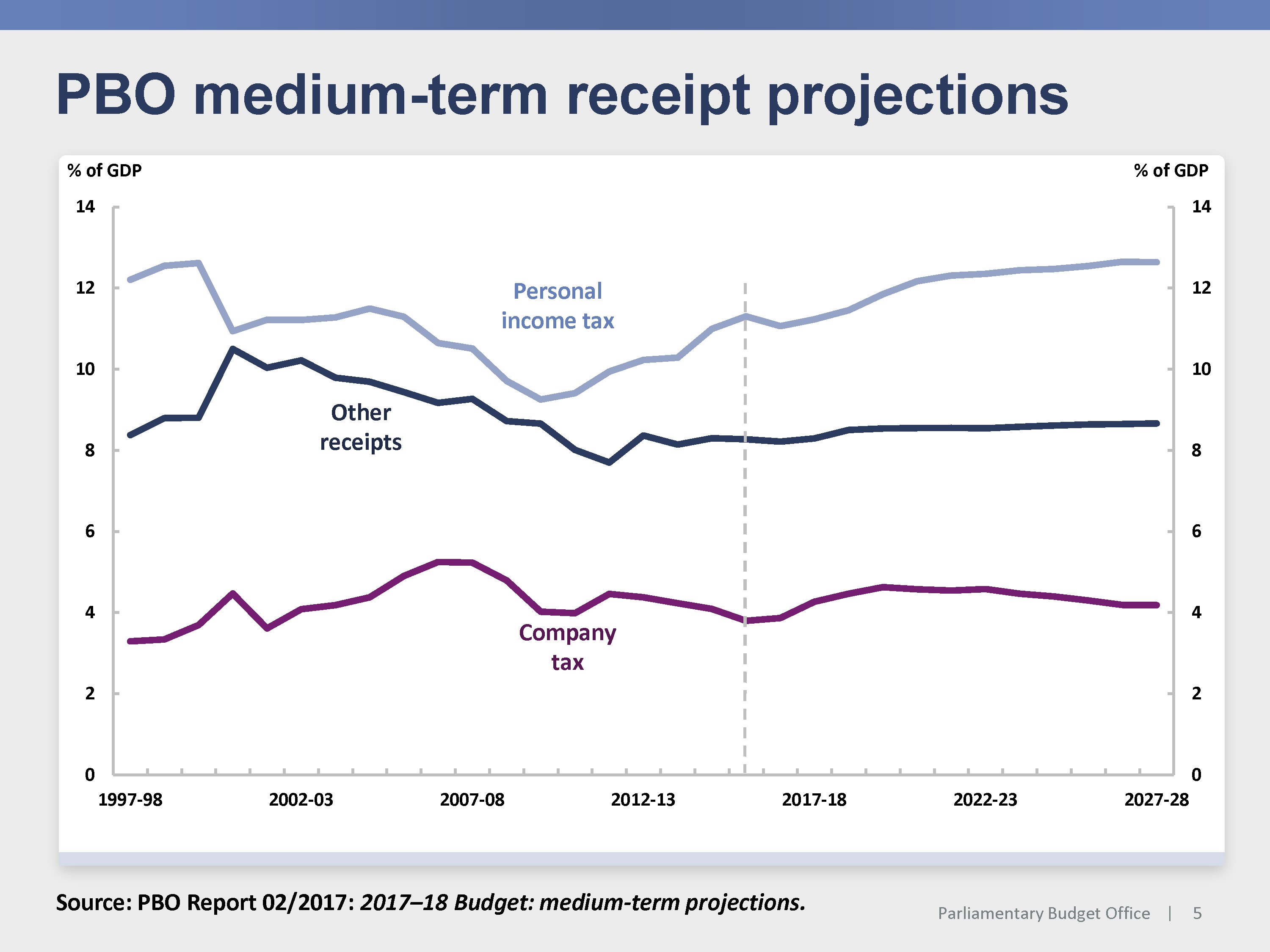

- the projected increase in receipts is predominantly due to a projected rise in personal income tax receipts over the entire medium-term period (Figure 4)

- once the 23.9 per cent ‘tax cap’ is reached, in 2022–23, personal income tax receipts are projected to continue to rise as a percentage of GDP as company tax receipts decline, on account of the government’s policy to cut the company tax rate over time to 25 per cent for all companies.

We also noted in the report that, in our view, the significant risks to the forecasts centred around the assumptions for a rebound in wages growth, and the assumptions that there would be no major new spending initiatives over the next decade.

Figure 3

Figure 4

Conclusions

Let me conclude with a few observations on fiscal sustainability.

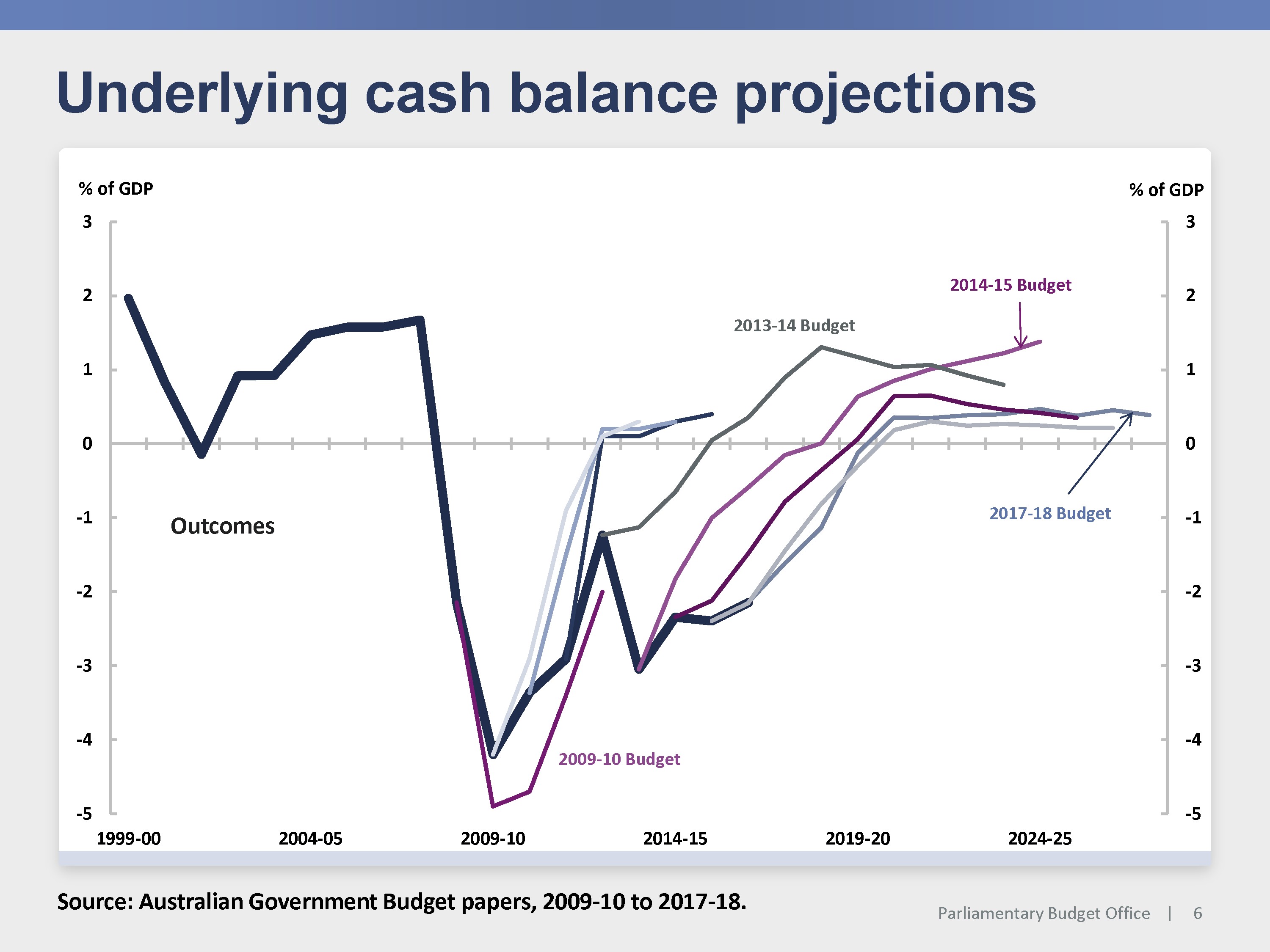

Over the past decade, Australia, like many other countries, has experienced a significant deterioration in its fiscal position and has clearly had challenges turning this around. This is evident when you look at the revisions to budget deficit and net debt forecasts in published budgets over a run of years (Figure 5).

Figure 5

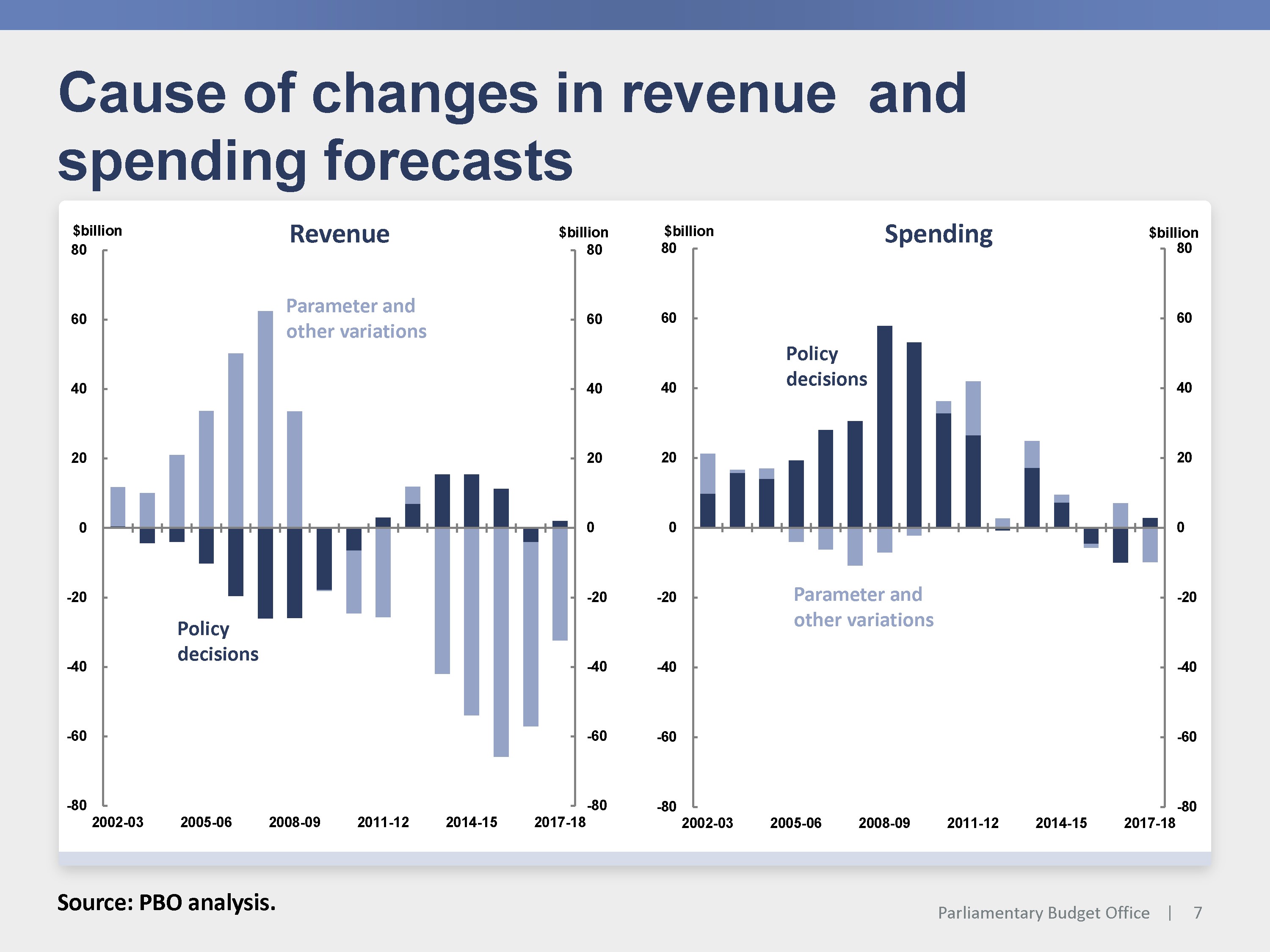

But what has driven these revisions? Figure 6 shows revisions to forecasts for payments and receipts, and break down these revisions into changes driven by policy decisions and changes driven by parameter variations—largely changes in the underlying economic forecasts.[1]

Figure 6

This figure illustrates that over the past decade, most of the revisions to the budget balance have occurred on the revenue side, and most of these have been due to changes in economic parameters. This shouldn’t be a surprise; most countries as well as institutions like the OECD and IMF have been surprised by the sluggish recovery in global growth forecasts, and no forecasters projected the magnitude of the movements in commodity prices which have occurred. These graphs also show that there has been significant restraint on the expenditure side, and there has been little variation in spending from first published estimates in recent years. Our recent paper on the DSP is an illustration of how some of this expenditure restraint has come about.

Looking ahead, there clearly remain risks around the forecasts, and ongoing fiscal restraint will to be critical. Ensuring that we have high quality medium-term forecasts for the fiscal implications of new policy commitments will enhance our ability to assess such commitments, especially when they have little impact on the forward estimates but a significant impact over the medium term. Such assessments will need to take into our aggregate fiscal position.

More broadly though, when we consider the sustainability of the fiscal position, I think it is useful to think about it from three different perspectives:

- How well is the budget being managed to ensure that we will be in a position to respond to the next economic or financial shock that comes along?

- How well are new sources of fiscal risks being managed, particularly those associated with commitments to new programs of spending or changes in taxation arrangements?

- How well are the slow-building sources of fiscal pressure being managed? These will be driven by demographics, structural changes, technological trends, and community expectations (around services like healthcare), and could undermine the sustainability of our fiscal position over the long term.

I think it would be useful to have a broader public dialogue around whether these are useful ways of framing a longer-term discussion around fiscal sustainability in a way that is more accessible to a wider audience.

So to conclude, I consider that institutions like the PBO are important in democratic systems, particularly in a world in which trust is at a low ebb. We aim to provide information that can improve transparency with a view to enhancing the quality of the public debate. Initiatives such as the Open Budget Survey make an important contribution as they open our eyes to how we are performing relative to other countries, and are a source of ideas for ways we could consider improving budget transparency and public participation in the budget process into the future.

[1] This analysis captures the impact of variations published at each economic and fiscal update for the budget year and forward estimates years. The analysis shows changes in the estimates for a given year between the first publication of an estimate for that year and the last published estimate. As a result, the analysis does not capture variations that occur outside the forward estimates.

Further readings: Australia country report | Global report | Rankings | Results by country | Data explorer

Open Budget Survey 2017 Part 1: How Transparent is the Australian Budget? by Miranda Stewart and Teck Chi Wong

Open Budget Survey 2017 Part 2: What Can Australia Do to Improve our Budget Process? by Miranda Stewart and Teck Chi Wong

All About Parliamentary Budget Office Costings by David Tellis

Economic Scenario Analysis of the 2017–18 Budget Medium-Term Projections by Lok Potticary

Podcast

Pingback: Open Budget Survey 2017: How Transparent is the Australian Budget? - Part 1 - Austaxpolicy: The Tax and Transfer Policy Blog

Pingback: Open Budget Survey 2017 Part 2: What Can Australia Do to Improve our Budget Process? - Austaxpolicy: The Tax and Transfer Policy Blog

Pingback: Open Budget Survey 2017 Part 1: How Transparent is the Australian Budget? - Austaxpolicy: The Tax and Transfer Policy Blog

An excellent speech that helps to highlight the continued importance of the Parliamentary Budget Office in Australia and international Independent Fiscal Institutions more broadly