Home

About

About this blog

About the TTPI

Articles

Briefs

Contribute

Guide for Contributors

Authors

Topics

Contact us

Resources

Advanced Search

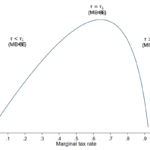

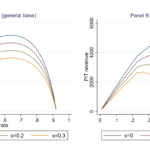

Rethinking the Laffer Curve From an Individual Approach: Evidence from the Spanish Income Tax

Next picture →