Deductions for work-related expenses (WREs) have been a feature of Australia’s income tax system since it commenced in 1915. The longstanding policy justification for deductions is focussed upon the correct measurement of the income which should be subject to tax.

Notwithstanding this, deductions are a contributor to tax system complexity, for taxpayers and tax administrators. The approach to WRE deductions in Australia has been characterised as quite generous by international standards. Economist Jonathan Baldry has referred to ‘a strong case against employee tax-deductibility of WREs on both efficiency and equity grounds’.

A recommendation of the Australia’s Future Tax System Review Final Report was the introduction of a standard deduction to ‘simplify people’s interactions with the tax system’ and to increase the level of pre-filling of tax returns. The Rudd Government announced the introduction of a $500 standard deduction in 2012-13, which was to increase to $1,000 in 2013-14. Ultimately, the proposed standard deduction was not enacted.

In 2021, the Blueprint Institute proposed a $3,000 standard deduction for individual taxpayers, which would apply to WREs as well as other deduction categories. The Blueprint Institute estimated that its deduction proposal would have a revenue cost of approximately $5 billion. The ATO estimated a tax gap for individuals not in business of $8.4 billion in 2018-19. According to Chris Jordan, WRE deduction claims are the main driver of the tax gap for this group of taxpayers.

We analysed the Australian Taxation Office’s (ATO’s) 2% Sample Unit Record File of individual tax returns (2017-18) to develop a reform proposal for WRE deductions that would improve simplicity, while achieving revenue neutrality. Our review of the sample file revealed that although 78.8% of these taxpayers had claimed WRE deductions, most of these claims were for relatively small amounts. Notably, 58.5% of taxpayers in the sample file population claimed less than $1,000 in WRE deductions.

Using an optimisation modelling approach, we found levels at which a standard deduction for WREs could be introduced, accompanied by a cap on claims for actual WRE deductions. The reform proposal is revenue neutral, as the revenue cost of the standard deduction is completely offset by the revenue gain of the cap. Our model was formulated as a mixed integer programming model, where the objective function maximises the standard deduction for a given cap level, subject to a revenue neutrality constraint.

Reform options

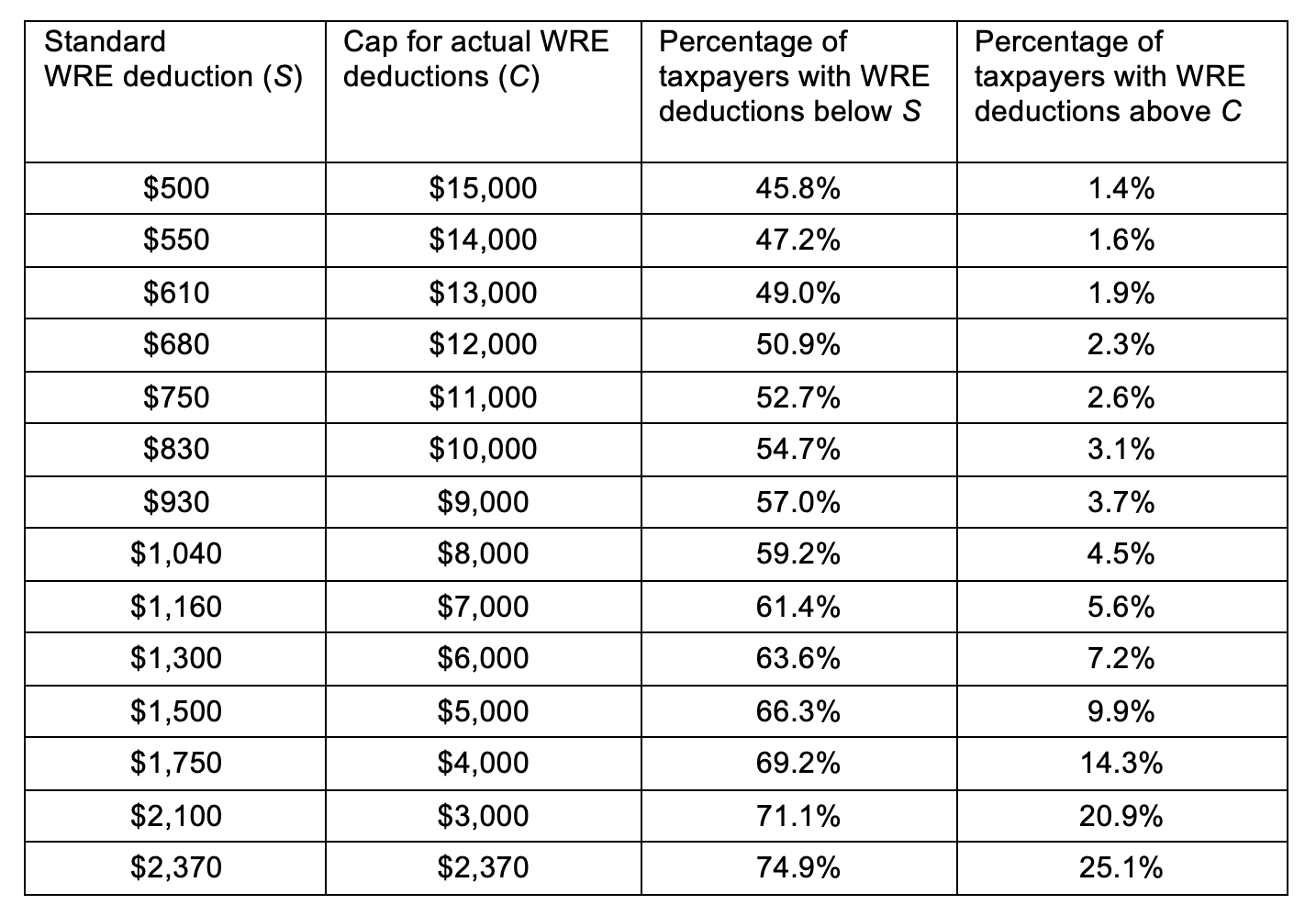

As shown in Table 1 below, our initial analysis yielded 14 revenue neutral levels of a standard deduction with an accompanying cap on actual WRE deductions. The table includes the percentage of taxpayers who would claim the standard deduction, as their WRE deductions are up to the standard deduction level. The table also shows the percentage of taxpayers who would have their actual WRE deduction claims limited to the amount of the cap.

Table 1: Revenue neutral combinations of standard WRE deduction (S) and WRE deduction cap (C)

Source: John Minas and James P. Minas, ‘Deductions for work-related expenses: an analysis of options for reform’ (2021) 36(1) Australian Tax Forum.

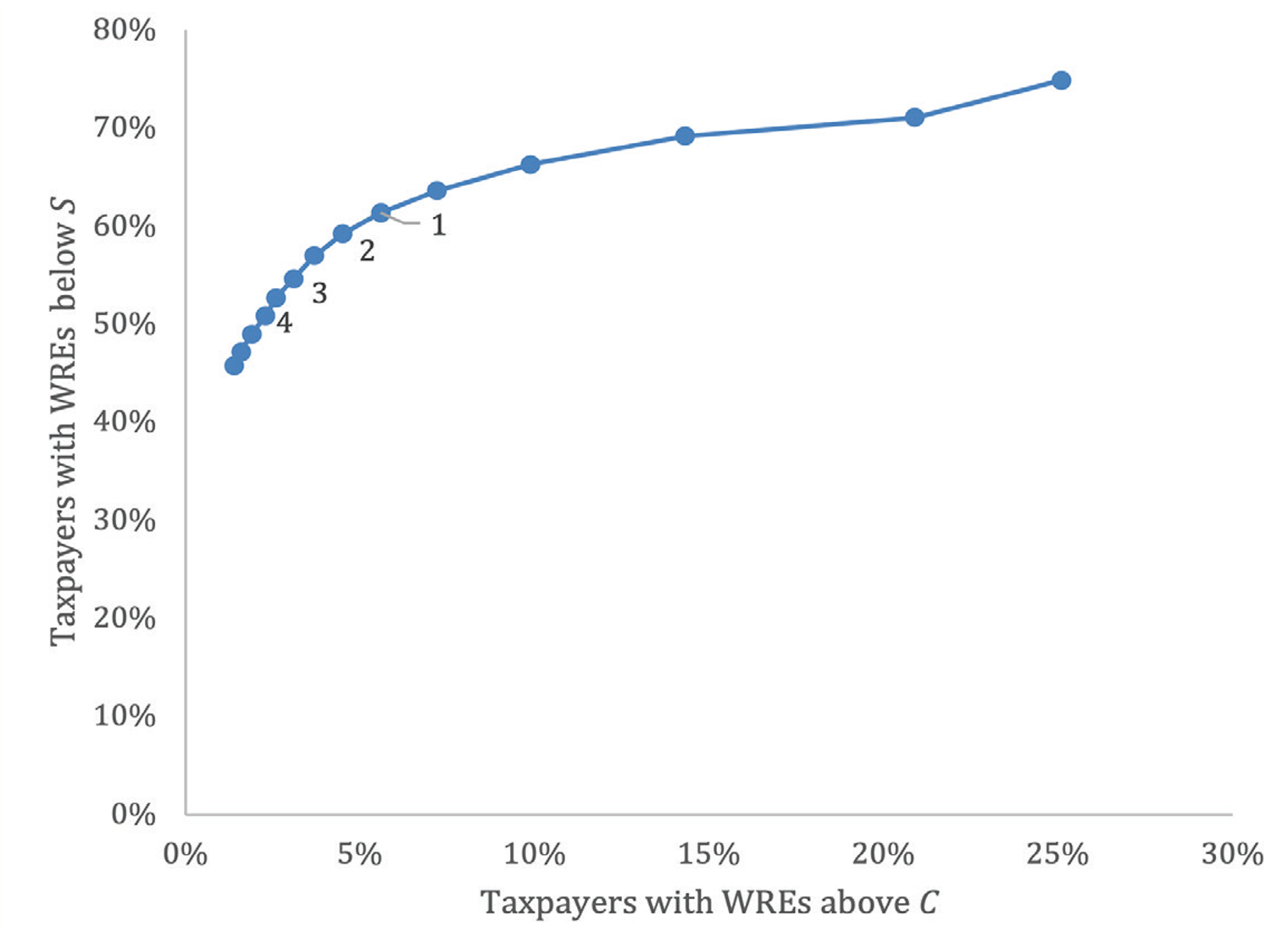

In Figure 1 below, the percentage of taxpayers with WRE deductions below the standard deduction level (S) is plotted against the percentage of taxpayers with actual WRE deductions over the cap (C). Included on the graph are Options 1 to 4, from Table 1, above. The graph is a visualisation of the trade-off between the simplicity benefit of claiming the standard deduction for WREs and the proportion of taxpayers who would incur a higher tax liability from the cap on actual WRE deductions.

Figure 1: Trade-off between percentage of taxpayers with WRE deductions below the standard WRE deduction (S) and percentage of taxpayers with WRE deductions above the cap on actual deductions (C)

Source: John Minas and James P. Minas, ‘Deductions for work-related expenses: an analysis of options for reform’ (2021) 36(1) Australian Tax Forum.

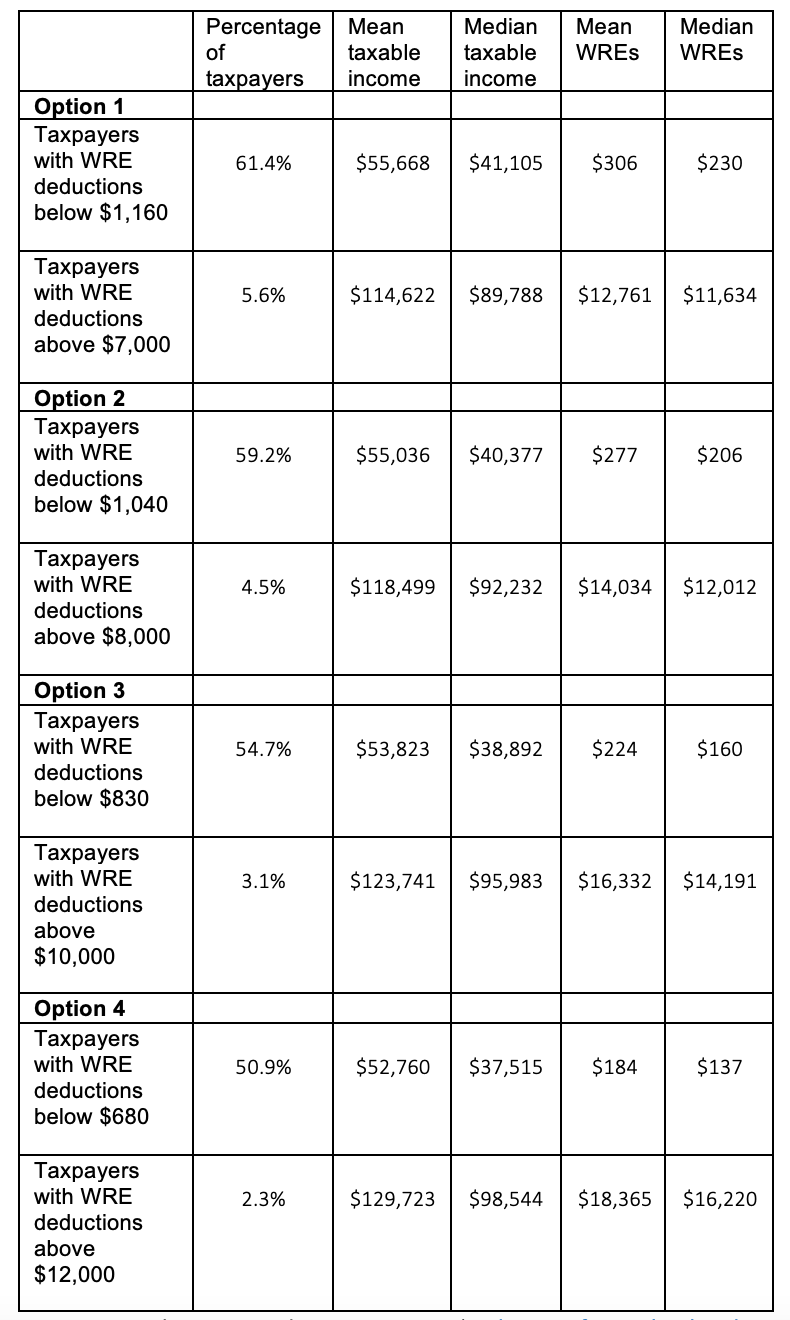

From our analysis, we focussed upon four options for reform that achieve a good balance between simplicity gains for most of the taxpayer population who would claim a standard WRE deduction, and the cap on actual deductions only applying to a small proportion of taxpayers.

These four options are set out in Table 2, along with the mean and median taxable incomes and levels of WRE deductions for taxpayers in each of the standard deduction and actual deduction groups for each of the four reform options.

Table 2. Four revenue-neutral combinations of a standard WRE deduction and cap

Source: John Minas and James P. Minas, ‘Deductions for work-related expenses: an analysis of options for reform’ (2021) 36(1) Australian Tax Forum.

Conclusion

Our proposed reform to WRE deductions has the advantages of being simple, transparent, and revenue neutral. Although the abolition of WRE deductions is another possible means of increasing simplicity, that is likely to be less politically feasible than our proposal for reform. Future research could consider the extent to which the costs of WREs could shift from employees to employers in the event that actual WRE deduction claims were capped.

We conclude that the simplicity gains for taxpayers and tax administrators are key arguments in favour of reform.

Recent Comments