Labour taxes on the average worker across OECD countries continued to decline for the sixth consecutive year in 2019, according to a new OECD report.

Taxing Wages 2020 shows that the “tax wedge” – total taxes on labour costs paid by employees and employers, minus family benefits, as a percentage of the labour cost to the employer – was 36.0% in 2019. This OECD-wide average rate, calculated for a single person with no children earning the average wage, represents a fall of 0.11 percentage points from 2018.

The indicators presented in Taxing Wages 2020 provide an important baseline on labour taxation in 2019, against which the impact of the COVID-19 pandemic can be measured. In responding to the COVID-19 pandemic, many countries have introduced a range of concessions that will contribute to a further decrease in labour taxes in many countries. Indicators for 2020, which will include the impact of the pandemic on wages and the different elements of labour taxation including income taxes, social security contributions, payroll taxes and cash benefits, will be available in the 2021 edition of the report. These indicators will inform future policy discussions on the role that labour taxes should play in the overall tax mix, both in recovery and beyond.

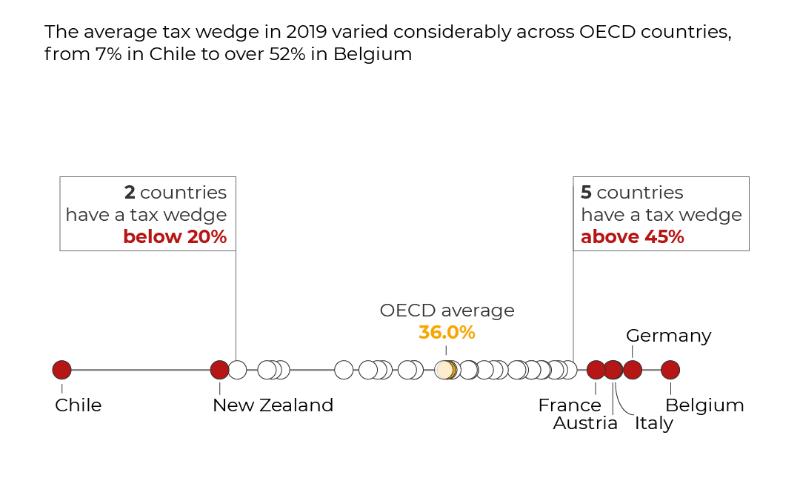

The decline in the average tax wedge between 2018 and 2019 was due to decreasing tax wedges in 17 countries. While the decrease in most of these countries was small, at less than one percentage point, the tax wedge in Lithuania fell from 40.7% to 37.2% (-3.43 percentage points), due to a strong decrease in employer SSCs following a major tax reform. In a further 19 OECD countries, the tax wedge increased between 2018 and 2019. This increase was less than 0.5 percentage points in all countries except Estonia, where there was an increase of 1.08 percentage points due to a reduction in the income tax allowance. Across countries, the tax wedge on the average worker in 2019 ranged from over 45% in France, Austria, Italy, Germany and Belgium to under 20% in New Zealand and Chile. In Australia, the tax wedge was 27.9%.

Tax wedge on labour costs in OECD countries, 2019

Taxing Wages 2020 also considers the net personal average tax rate (NPATR), which measures the income tax and SSCs paid by employees, minus any family benefits received, as a share of gross wages. In 2019, the OECD average rate was 25.9% for a single person with no children earning the average wage. This rate is 0.4 percentage points higher than in 2018. The NPATR for the average worker varies considerably among countries: ranging from below 15% in Mexico and Chile to over 35% in Denmark, Lithuania, Belgium and Germany.

The report also includes a Special Feature on the taxation of non-standard workers. Tax systems in which different employment forms are taxed differently may incentivise the adoption of certain employment forms over others. For example, in Italy and the Netherlands, the tax-related labour costs of standard employees far exceed those of non-standard workers, indicating that firms have incentives to shift away from standard employment. In many countries, non-standard-workers do not enjoy the same range of social protections as standard workers and the COVID-19 pandemic has further highlighted the vulnerability of some of these workers. Policymakers need to examine the incentives that may accompany differential taxation across employment forms in their countries to ensure that tax systems do not unduly incentivise the growth of tax-advantageous employment forms or exacerbate the vulnerability of non-standard workers.

Key findings from Taxing Wages 2020:

Tax wedges for single people and families with children

- In 2019, the highest average tax wedges for single workers with no children earning the average national wage were in Belgium (52.2%), Germany (49.4%), Italy (48.0%), Austria (47.9%) and France (46.7%). The lowest were in Chile (7.0%) and New Zealand (18.8%).

- In 2019, the highest tax wedge for one-earner families with two children at the average wage was in Italy (39.2%). Finland, Greece, Sweden and Turkey had tax wedges of between 37% and 38%. New Zealand had the lowest tax wedge for this family type (3.5%), followed by Chile (7.0%) and Switzerland (9.9%).

- Between 2018 and 2019, the largest increases in the tax wedge for one-earner families with children were in Slovenia (3.3 percentage points), Poland (2.6 p.p.), New Zealand (1.6 p.p.), Estonia (1.4 p.p.) and the Czech Republic (1.0 p.p.). The largest decreases were in Lithuania (4.2 p.p.), Austria (3.7 p.p.) and France (2.3 p.p.).

- The tax wedge for one-earner families with children is lower than for single individuals without children in all OECD countries except in Mexico, where both household types face the same tax levels. The differences are around 15% or more of labour costs in Belgium, Canada, the Czech Republic, Germany, Hungary, Ireland, Luxembourg, New Zealand, Poland and Slovenia.

Net personal average tax rates (NPATR) for single people and families

- In 2019, the highest average NPATR for single workers with no children earning the average wage were in Belgium and Germany (both 39.3%), Lithuania (36.1%) and Denmark (35.4%). The lowest were in Chile (7.0%) and Mexico (10.8%). The OECD average increased by 0.4 percentage points to 25.9%.

- The average NPATR for one-earner families with children was 14.6% in 2019. The highest NPATRs for one-earner families with two children at the average wage were in Lithuania (27.7%), Turkey (26.5%) and Denmark (25.2%). The lowest NPATRs were in the Czech Republic (1.8%), Canada (2.4%) and Estonia (2.9%).

Special Feature – Taxation of non-standard work

- Among the seven OECD countries that are observed in the Special Feature, in Italy and the Netherlands, the tax-related labour costs of standard employees exceed those of non-standard workers, indicating that firms have incentives to shift away from standard employment.

- For example, in Italy, the tax wedge of an employee with a permanent contract earning the average wage was 47.7% using 2017 tax rules compared to 14.4% for a worker taxed under the forfait regime. In the Netherlands, the tax wedge of an employee was 37.4% compared to 15.1% for a self-employed worker.

To access the report, country notes, and summaries, visit: http://oe.cd/TaxingWages.

Recent Comments