Australian Prudential Regulation Authority (APRA) statistics indicate that most Australian retirees utilise an account-based pension (ABP) in the retirement phase of superannuation. An ABP allows retirees to make a choice of investment and drawdown strategies, but provides no longevity protection.

Through recent initiatives (for example, the Retirement Income Covenant), the government has expressed a desire for more retirees to use lifetime income streams. Traditional life annuities, which provide a fixed or inflation-linked payment for life, have been offered in Australia for many decades. More recently, several providers have launched innovative lifetime annuities (ILAs), which provide some of the features of an ABP, whilst still guaranteeing an income for life.

The Age Pension means testing treatment of ABPs and ILAs is however substantially different. This article draws on our recent paper to show how the current means testing rules across ABPs and ILAs are confusing and offers a better and coherent solution.

Improving Age Pension means testing

The Australian retirement income system consists of three main components, namely the government-funded Age Pension, compulsory superannuation savings, and voluntary savings. The Age Pension payment in Australia is unusual compared to most developed countries, in that it is universal, non-contributory and means tested. Age Pension means testing leads to complex interactions between the retirement phase of superannuation and the Age Pension payment; and navigating these interactions can have significant impacts on the amount of Age Pension received.

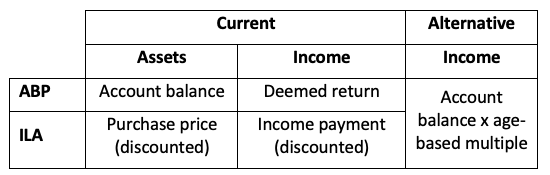

Currently, Age Pension payments are based on the lowest amount from a separate asset test and income test. As described in Table 1, the calculation of assets and income for these tests is confusing in that it is different for ABPs and ILAs.

Table 1 – Calculation of assets and income for ABPs and ILAs

A potential solution, shown in Table 1 as “Alternative”, is to abolish the asset test and calculate income consistently from all non-principal residence assets, using a percentage multiple that includes both a deemed rate of return and a return of capital. This approach is similar to the minimum drawdown from an ABP in that the multiple of assets increases with age. This approach has also been discussed previously in the Retirement Income Review and by other scholars.

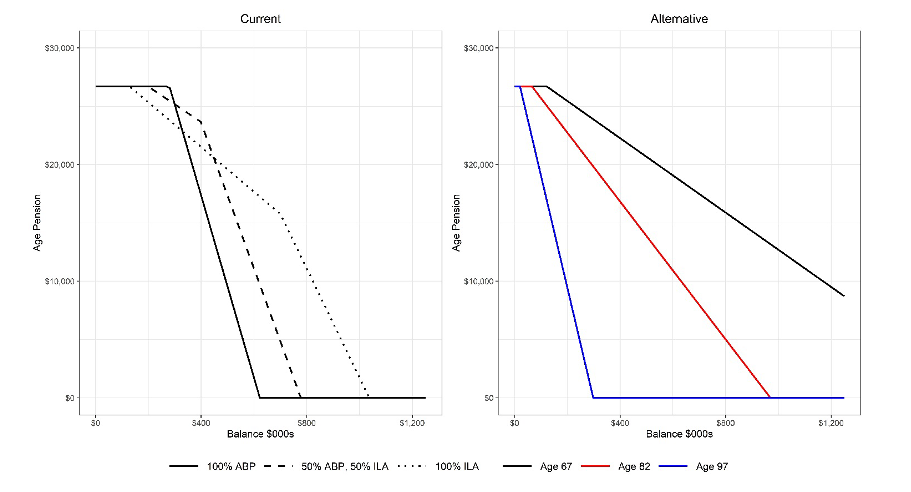

To keep things simple in our analysis of these approaches, we’re focusing on a non-working single homeowner who’s retired. All their non-principal residence assets are held in an ABP and/or ILA in the superannuation retirement phase. Results are generalisable across other scenarios. In Figure 1, we show the amount of Age Pension received across various asset (balance) levels. For the Current approach, we show the results at age 67 across different combinations of ABP and ILA, whilst for the Alternative approach we show only the impact of age since the mix of ABP and ILA does not matter. See our paper for assumptions.

Figure 1 –Age Pension received (per annum)

The slope of the lines in Figure 1 represents the taper rate of the means test, namely the amount of Age Pension lost for a $1 increase in balance. For Current, steeper taper rates come from the asset test. The effective taper rates for Current under the asset test are 0.078 and 0.047 for ABP and ILA, respectively. This difference in taper rates is due to the discount applied to the purchase price of ILAs and hence, at least initially, ILAs are favoured over ABPs under the asset test. The effective taper rates for Current under the income test are much lower at 0.011 and 0.019 for ABP and ILA, respectively. Despite the discount applied to the income payment in the ILA, ABPs are favoured over ILAs under the income test, due to historically low deeming rates currently being applied to the ABP (a maximum of 2.25% per annum).

With 100% allocation to ABP, the asset test applies at all balance amounts. When 50% ILA allocation is incorporated, the asset test discount on the ILA means that at balance levels between approximately $200,000 and $400,000 the income test applies, while the asset test only applies at balance levels above $400,000. Hence, at balance levels above $300,000, additional Age Pension can be obtained by incorporating some ILA allocation. At balance levels above $800,000, the only way to obtain any Age Pension is to have a proportion of ILA allocation above 50%.

The removal of the asset test in Alternative sees a taper rate applied to ABP and ILA assets equally but varied by age, with the taper rates being 0.016, 0.030 and 0.096 for ages 67, 82, and 97, respectively.

The optimal mix and drawdown speed

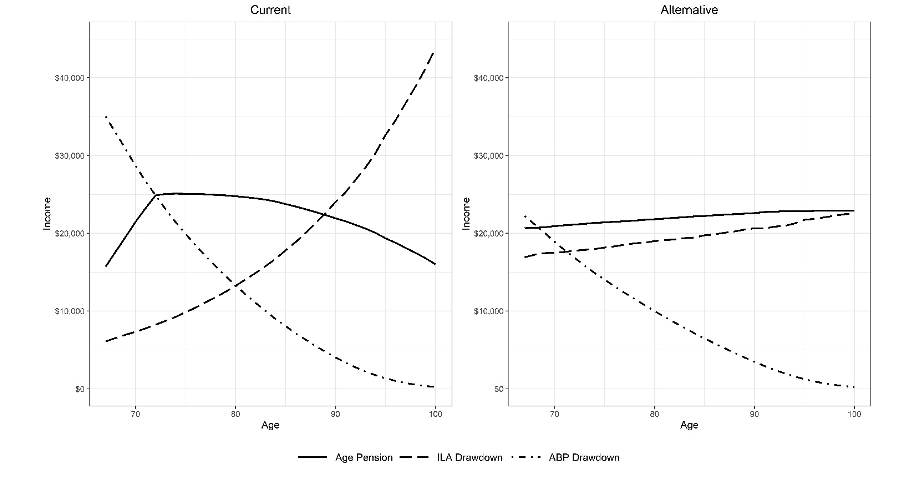

Now let’s turn our attention to the optimal mix of ABP and ILA, and optimal drawdown speed, assuming retirement phase assets of $500,000 at age 67. We used a lifecycle model to perform optimisation, details of which can be found in our paper. We found that the optimal allocation to ILA is 40% for Current and 58% for Alternative. Projected sources of income for these optimal decisions are shown in Figure 2.

Figure 2 – Projected income sources during retirement (per annum by age)

For Current, the annual Age Pension amount starts at $15,700 before rapidly increasing to $25,100 by age 74. This is driven by a rapid drawdown of the ABP in the early years of retirement, to benefit from the higher taper rate of the asset test. Income from the ILA is kept very low in the earlier years of retirement, to not influence the income test. The initial low ILA income causes an exponential increase in ILA income in later years, which brings the Age Pension down again due to the income test. This trend is common to all initial asset levels of $400,000 and above. Despite Figure 1 indicating that higher balance levels create a stronger initial incentive for ILA allocation, if ILA allocation is too high the ability to increase Age Pension by rapid ABP drawdown is compromised.

For Alternative, the annual Age Pension amount starts at $20,700 and slowly increases with age due to the general incentive to drawdown in a way to increase Age Pension receipt. This relative stability is because the increase in taper rate with age (as discussed above) is offset by a reduction in assets with age. This is a desirable feature of this means testing setting. The drawdown speeds for Alternative are not as dramatically fast or slow as Current, for the ABP and ILA, respectively.

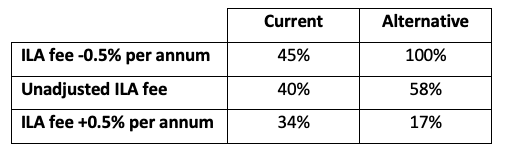

Evidence of the influence of the Current means testing rules on decisions can be found by considering the optimal allocation to the ILA as we adjust the ILA fee. We tested both an upward and downward adjustment of 0.5% per annum; results can be found in Table 2. Changing the ILA fee has very little impact on the range of optimal ILA allocations for Current (34% – 45%) but a substantial impact on Alternative (17% – 100%). This is because the ILA allocation (and drawdown speeds) for Current is driven by minimising the impact of the asset test on the ABP and the income test on the ILA, as discussed above, rather than the cost and value of the ILA.

Table 2 – Optimal ILA allocation depending on ILA fee

Implementation

Implementing the proposed Alternative structure would require ILA providers to track an underlying balance for each annuitant; this should not present any logistical challenges. Furthermore, this would also allow the government to implement a coherent incentive to annuity purchase if so desired. There are of course, substantial challenges that would be faced in moving away from the current means testing framework, which we look forward to considering in future research.

Recent Comments