My recently published article, Corporate tax transparency reporting and Benford’s law, examines the reasonableness of the Australian Government’s mandatory tax transparency disclosures utilising the Benford’s law phenomenon. Benford’s law is a mathematical tenet that opens up an insightful examination of a dataset that gains annual media attention, putting hundreds of companies in the spotlight based on three figures from the annual tax return: total income, taxable income and tax payable.

In doing so, this research brings to the forefront irreconcilable gaps and limitations impacting the regime arising from disparity between the accounting and taxation systems; omitted business activity occurring beyond the tax entity and between total income and taxable income; as well as the broader objectives of the taxation system. As such, it takes a novel approach in response to earlier stakeholder concerns and growing public debate over corporate tax transparency, that goes beyond purported deviations to 30% prima facie tax and the misnomer that any discrepancy to a 30% effective tax rate equates to tax forgone.

What is ‘Benford’s law’

Benford’s law has been described as a high-level test of reasonableness by scholars such as Drake and Nigrini (2000) and Henselmann, Ditter and Scherr (2015). According to Nigrini (1999), it is a mathematical phenomenon that can identify irregularities in numbers or anomalies in number-pattern, which in turn can indicate the presence of potential errors, fraud or bias.

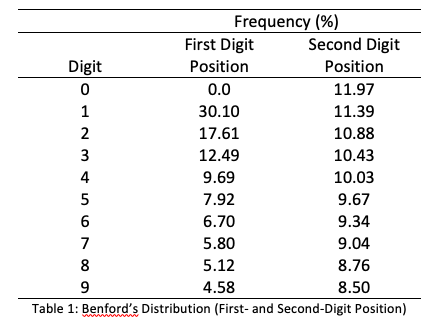

The phenomenon was first noticed by astronomer Simon Newcomb in 1881, when he observed a pattern in the wear and tear of books: the earlier pages being more worn than the latter. Then in 1938, the physicist Frank Benford, formally tested and confirmed Newcomb’s observation. Now known as ‘Benford’s law’, the phenomenon defines the natural frequency of the digit distribution to be heavily skewed, with the highest probability that the first digit will be a one (30.10%), reducing thereafter:

There are similar expected frequency distributions for following digit positions, however the bias is most pronounced in the first digit position, reducing thereafter. Here the focus is on the first- and second-digit positions. Research has found that market values, accounting data and income tax expenses are all examples of data that are likely to conform to Benford’s law.

Why is this relevant

There has been consistent and growing concern that corporations, particularly the large multinational companies, are not paying their ‘fair share’ of tax. Concern is persistently raised over the existence and impact of tax avoidance, opportunistic earnings management and tax minimisation activities in eroding government revenues and the tax system itself (consider the Panama and Paradise Papers as recent examples). As part of a suite of regulatory reforms directed towards the tax system, the government initiated the corporate tax transparency reporting regime. This is a notable step in Australian taxation history, as traditionally tax affairs have remained largely confidential (for example through confidentiality provisions found in Taxation Administration Act 1953 (Cth) Schedule 1, division 355).

Although there is general support for increased transparency and accountability of big businesses in respect of corporate income tax, some stakeholders raised concerns with the proposed tax transparency approach that has been subsequently adopted. As well as concern over the effectiveness of the regime and reputation and privacy issues, concerns related to the complexity in what appears to be a simple disclosure regime have also been raised. Importantly, concern was raised as to whether the limited disclosures would be misunderstood. Complexity generally arises due to the:

- Difference in entity structure between tax consolidated groups listed in the tax transparency report and related economic entities forming the basis of accounting disclosures;

- Inconsistencies between accounting and tax systems more generally;

- Lack of relationship between total income (a gross income figure excluding potentially legitimate business expenditure) and taxable income (net figure specific to tax law).

One reason that the tax affairs of large corporations have been able to remain confidential, despite the numerous reporting requirements (such as annual financial statements and ASX listing rules), is the substantive difference between the accounting and taxation systems’ methodologies. These differences stem from the differing objectives underpinning each system. One clear objective of the tax system is revenue raising. However, other objectives (driven by social or political factors) can legitimately lead to differing measures of profit and an effective tax rate different to the 30 per cent corporate tax rate. This can be compared with the objective of the accounting system directed at providing information for decision making purposes.

One relevant difference directly creating complexity in this disclosure regime is the structuring of the entity itself. A particular group of entities that make up a consolidated group for the purpose of preparing consolidated financial statements (as mandated by accounting standards) does not necessarily align with the structure of a tax entity or tax consolidated group found in the transparency report. Simply put, the consolidated entity for accounting purposes may not be the same entity for tax purposes, therefore related disclosures do not necessarily capture the same or all economic activity.

Further, differences exist due to specific treatment of specific business activities. For example, when the taxation system offers accelerated depreciation rates compared to accounting or requires doubtful debts to be written off (meeting certain requirements), these can result in temporary differences (differences relate to the timing of recognition). Some differences, however, are permanent and will never be reconciled with the passing of time, for example non-deductible expenditure for tax purposes or exempt income. These differences result in reported income tax expense disclosed in the income statement that is not necessarily aligned with the actual tax obligation arising with the Australian Taxation Office. These factors contribute to the concern that disparity between the systems cannot necessarily be reconciled by a limited disclosure regime.

Substantive questions are therefore raised as to whether the regime produces reasonable information. This research examined the reasonableness of the disclosures beyond an analysis of whether companies are paying their ‘fair share’ of tax based on the 30% corporate tax rate, acknowledging the disparity between accounting and taxation. Henselmann et al. (2015) suggest Benford’s law is helpful in assessing the reliability of financial reporting content and an appropriate method to consider the reasonableness of the tax transparency data, through mapping out digital frequencies across the three disclosed figures.

What the study did

Using the 2014-15 corporate tax transparency report data, the leading (first) and second digit frequencies of total income, taxable income and tax payable (observed) were compared against Benford’s distribution (expected). The Z-statistic and chi-square test were used to assess the observed frequencies/distribution against the expected frequencies/distribution to test for statistical significance.

Importantly, a number of characteristics of Benford’s law are worth noting. Firstly, where there is an in built maximum or minimum to the data set, non-compliance with the expected distribution can occur. Given entities are only included in the report once they meet the minimum total income threshold ($100 million or $200 million dependent on whether they are public or private entities respectively), it was anticipated that total income may not conform to the expected distribution.

Secondly, multiplication or division does not generally impede compliance. For example, tax payable in basic terms being a percentage of taxable income was not expected to influence compliance.

Thirdly, omitted data does not generally impede compliance. 1,904 firms were identified and observed with a total income disclosure. Of those, 1,363 reported taxable income and 1,226 reported tax payable. The reports do not divulge tax losses or tax refunds, instead they are reported as zero. This leads to a limited understanding of the complete tax position but was not anticipated to influence compliance with Benford’s law.

What the study found and where does this lead?

Unsurprisingly, the distribution for total income was significantly different to the Benford’s distribution for the first digit position, likely a result of the in-built threshold. Yet intriguingly, taxable income and tax payable were not statistically different and thus can be labelled as Benford’s Sets. This indicates a very low level of error, bias or fraudulent reporting and provides somewhat compelling evidence towards the regime’s reasonableness. These findings support prior research that suggests large companies place a strong emphasis on tax compliance and that there are legitimate and illegitimate tax planning efforts.

Importantly, the study suggests that taxable income and tax payable are substantively removed from total income, evidenced by the lack of contamination of the in-built minimum threshold present in total income. Arguably, total income is a meaningless starting point. Moreover, despite somewhat reasonable disclosures being produced, the disconnect or disparity between the accounting and taxation systems results in continued concern over the regime’s ability to enable the public to better understand corporate taxation, particularly where media seize aspects of the disclosures that are the least connected (total income and tax payable).

Importantly, the research reveals that there are strong overtones of what is disclosed (revealed to have low deviation) and what is censored by the regime (outside of the regime’s scope), highlighting the need for a closer consideration of irreconciled differences, particularly in respect to the underlying corporations captured by the regime and their alignment with the economic entity within the public spotlight.

Elizabeth, I am aware of Benford’s ‘Law’, but had never imagined its relevance to taxation. I’ll read the paper to see what I think. My interest is tax transparency (among other things.) The comment that “Arguably, total income is a meaningless starting point” concerns me, but perhaps it is right. My sense of it is that “total income” may not be a useful starting point in individual cases (a taxpayer may have realised a large capital loss, or incurred a singular deductible expense) but across the whole 10.8 million individual taxpayers it remains a key benchmark, as the gap between it and the number for taxable income is for me at least a key indicator of who is pulling their weight and who is not. Arguably, sole traders with significant expenses – a modern tradie perhaps – may have a high total income but a much lower taxable income. Are you aware of any data that examines this issue? Joe Roach

Thanks for the comments Joe! You will see some discussion of total income as the starting point in the full article. I hope you enjoy it. This was a particular aspect raised by the submitters to the original proposal, which these findings somewhat agree with. You make a relevant point though; from an aggregate viewpoint we can garner useful insights. Keep in mind too that the source of Total Income is item 6 of the tax return, which created some concern. I also think that, in relation to an obligation to tax, the relevant expenditure that occurs between total income and taxable income cannot be ignored. It is important to consider the context to which this data is then broadcast and the limited scope of this regime. There is a meaningful gap in what is being provided. What is intriguing is what is not being captured by this reporting regime. As to comparing to individuals, we need to be mindful of the different compliance setting. The companies captured by the regime are generally producing general purpose financial statements according to accounting concepts, whilst complying with the tax legislation in the determination of their tax obligations. As such, there is an added layer of complexity to transcend to fill the gap, and be transparent, between what we see as notable businesses (economic group) and this tax reporting regime (tax consolidated group/tax entity). Cheers, Lizzie.