Individual taxpayers and businesses incur costs when complying with tax laws in addition to the tax paid and the efficiency costs. These costs are associated with time and money spent on record-keeping and completing tax forms, wages for accounting staff, and fees paid to external tax advisers. These costs are known to be significant and can deter taxpayers or businesses from effectively engaging with the tax system.

The regular measurement of tax compliance costs is useful for policy purposes. Tax compliance costs have traditionally been estimated using large-scale surveys. Although these surveys are capable of delivering plausible results, they are expensive and time-consuming and, as a result, do not take place very often. Moreover, even if large-scale surveys were carried out frequently, they might not have be conducted in a comparable fashion.

To find a reliable and feasible alternative, some techniques from data science can be utilised and adopted in measuring tax compliance costs. A key aspect of data science is to approximate the data generation process as closely as possible, crucial to gain a critical understanding of how tax compliance costs arise and flow. These costs are a direct result of a tax system. Complex tax laws result in higher amounts of resources spent by taxpayers on complying with these laws. If the complexity of the tax system can somehow be quantified, then it is possible to estimate the resulting tax compliance costs.

Like tax compliance costs, tax administration costs are also a direct result of the same tax system. If the tax system is complex, tax collectors will also incur higher costs to ensure that taxpayers are compliant. Fortunately, the data on tax administration costs are much easier to obtain. It is widely accepted that costs of running the central tax agency approximates the tax administration costs. Thus, it is reasonable to conclude that the running costs incurred by the Australian Taxation Office (ATO) embed some information on Australian tax system complexity.

Using the historical administration costs of the ATO, a series of annual growth rate can be easily computed. A critical question should be asked: What are the fundamental factors that drive the growth? We conclude in our study that there are three main responses to this question. First, the price inflation factor. Secondly, population growth implies that more people are required to fulfil their tax obligations and therefore more administrative tasks for the ATO. Finally, when the tax system becomes more complex, for example, new tax laws are introduced, more resources will be spent by the ATO accordingly. We focus on the key word ‘fundamental factors’ as they are the driving force of long-term changes in tax administration costs. In the short term, the ATO can incur higher or lower administrative costs regularly due to factors such as organisation restructuring and purchasing additional computers. A realistic approach must take into account both the long- and short-term factors.

Method and result

Since a link between administrative costs of the ATO and the complexity of the tax system has been established, we use a state space model with a Kalman filter to extract and quantify that connection. The state space model is a well-established statistical method with strong applications in applied physics. For example, in measurement analysis, all equipment readings are considered as inaccurate due to minute levels of interference such as electrical noise. The state space model decomposes measurements into true unobservable measurements and random noise, and by applying a Kalman filter, true measurement can be continuously estimated as long as new observations become available. Such models have greatly advanced applied physics such as sending satellites into orbit. They can also be applied in taxation studies.

By applying both the state space model and the Kalman filter, we are able to estimate the growth rates of Australian tax system complexity (the true measurement) from the ATO’s annual administrative costs that are no longer affected by short-term factors (random noise).

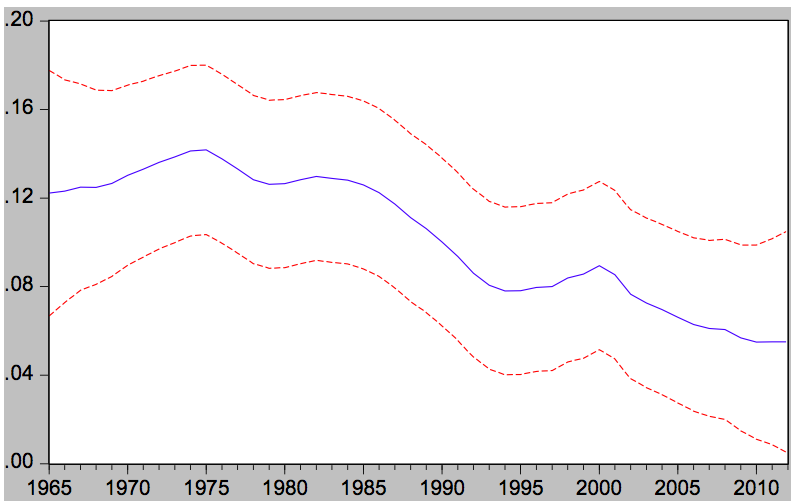

We sourced the ATO’s annual costs between financial years 1964 and 2012 for our analysis. The estimated growth rates of the complexity of the tax system are presented in Figure 1. The blue line represents point estimates of the growth rates of the tax system complexity and the red lines are 95% confidence interval.

Figure 1: The estimated growth rates of the complexity of the tax system

Source: Wu and Binh (2017), Estimating aggregate tax compliance costs: A new approach using a state space model, Australian Tax Forum, 32(1), pp. 197-224

Source: Wu and Binh (2017), Estimating aggregate tax compliance costs: A new approach using a state space model, Australian Tax Forum, 32(1), pp. 197-224

We can see that Australian tax system complexity is growing at a declining trajectory over time, despite a few temporary increases. For example, the introduction of the Goods and Services Tax (GST) in 2000 did accelerate the growth of tax system complexity, however it did not reverse the overall trend.

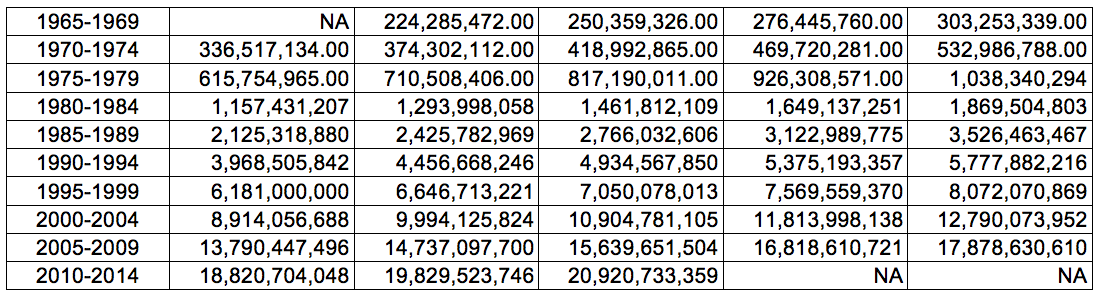

Evans et al (1997) conducted a comprehensive survey on tax compliance costs across Australia and reported a net aggregate compliance cost of A$6.181 bn for the financial year 1994-1995. Given that both tax administration and compliance costs are direct products of the tax system, we can say that tax compliance costs should grow at the same rate as the tax system complexity growth rate . Thus, it is reasonable to generate a series of tax complianc cost calculations based on survey results and state space model outputs. The results are presented in Table 1.

Table 1: Estimated Annual tax compliance costs

These generated annual tax compliance costs are in nominal prices. By construction, these costs are driven only by the tax system. Temporary shocks such as higher fuel prices that result in higher tax compliance costs are not reflected in our estimates.

A few thoughts on the results and their implications for future research

We simply matched our current understanding of the tax system to applicable data science techniques. As such, our model outputs are only as good as our understanding of the Australian tax system. In theory, our model is capable of generating annual tax compliance costs as long as the ATO exists. However, a reality check is necessary whenever this model is used. For example, have there been substantial changes to the tax system that make the underlying assumptions of the model invalid? This leads to the question of why data science should be applied at all in this context and what roles it can play in future tax research or policy development.

Data science is about pattern seeking and can rarely be used to explain natural phenonmena like physical laws. Patterns can help to perform immediate forecasts and quantify latent factors that are traditionally unobservable. More importantly, they have the potential to aide tax system design. For example, supervised machine learning techniques can be applied annually to fully profile income deduction claim patterns among Australian taxpayers. Such profiles can be used to exmaine the effects of changes to income deduction policies.

Data science and taxation policies can complement each other and there is a wealth of research potential that lies within it. Data science can be used to track the movement and provide almost simultaneous feedback on the effect of tax policies. At the same time, tax policy makers can make changes to organisation and laws so that a wider range of data science techniques can be applied. This unique combination is not often seen in social science settings and its potential is exciting.

Did the study take into account the mandatory annual efficiency dividend imposed on Govt departments?