We examine the relation between the riskiness of chief executive officers’ (CEOs’) sports hobby and firms’ aggressiveness in tax planning. We expect that individuals develop specific sports interests based on their personal risk preferences after trading off the utility derived from participating in sports with potential risks of injuries. We propose that CEOs’ personal risk-taking preferences, measured by their self-disclosed sports hobbies, extend across both the personal and corporate decisions they make including corporate tax aggressiveness.

While new to the accounting and finance literature, the association between an individual’s sports hobbies and their personal risk preferences has long been recognised by psychology researchers, who suggest that the pursuit of sports can be indicative of personal attitudes toward risk. Prior literature documents that individuals loving sports with high injury risks are risk seekers and tend to underestimate risks associated with their chosen sports.

As evidenced by a number of prior studies, corporate tax planning offers an interesting setting to study the effect of CEOs’ innate risk preferences on corporate risk-taking. A firm’s tax aggressiveness is a unique and strategic decision made by its top management, where such a decision is an outcome of cost-benefit tradeoffs. On the one hand, firms can generate considerable tax savings by taking aggressive tax positions through structuring business transactions in grey areas of tax laws or operating in regimes with low tax rates that may test the limits of tax compliance. On the other hand, aggressive tax positions can expose firms to uncertainty in compliance and tax risks including regulatory fines, penalties, and reputation risk. Ultimately, executives’ risk preferences likely play a significant role in the trade-offs.

To capture firms’ tax aggressiveness, we use four different measures: (1) a predicted tax shelter score, (2) predicted unrecognised tax benefits, (3) the coefficient of variation of the cash effective tax rate, and (4) the industry-size adjusted long term cash effective tax rate.

Measuring sports risk

Sports psychology researchers broadly define high physical risk sporting activities as having high likelihoods of injury and death. Thus, to quantify a CEO’s risk-taking preference, we develop a measure to capture the risk of the CEO’s sports hobbies, labeled SPORTS_RISK, based on the actual injury rate of a particular sport. We obtain the number of sports-related annual injuries from the National Electronic Injury Surveillance System (NEISS) produced by the Consumer Product Safety Commission (CPSC), a nation-wide system that collects information on patient hospital visits in the United States. The NEISS details the activities (sports and otherwise) that caused the injury and classifies the consumer product, if any, involved in the injury. In consideration of the age range of our sample CEOs, we include the number of injuries reported in the database for the population between ages 25 and 85. Next, we divide the total number of annual hospital injury visits associated with a sport by the total annual number of participants between ages 25 and 85 in the same sport (based on data from the US Census Bureau’s Statistical Compendia Branch which publishes annual statistics on participation in common recreational sports across different age groups). We then use the total annual number of injuries scaled by the total annual participation associated with a sport over the period from 2001 to 2009 as our proxy to measure the sport risk and interpolate this measure across our sample period.

To estimate an individual CEO’s risk preferences for our empirical analyses, we match the calculated sport risk as described above to the reported sports hobby of each CEO in our sample. If an individual CEO has multiple sports hobbies, we set his risk preference as the maximum sport risk value among all sports hobbies of that CEO (namely his riskiest sport hobby). For example, if a CEO indicates his sports hobbies include both golf and skiing, we set his risk preference to the higher of the two calculated sport risks, which is skiing.

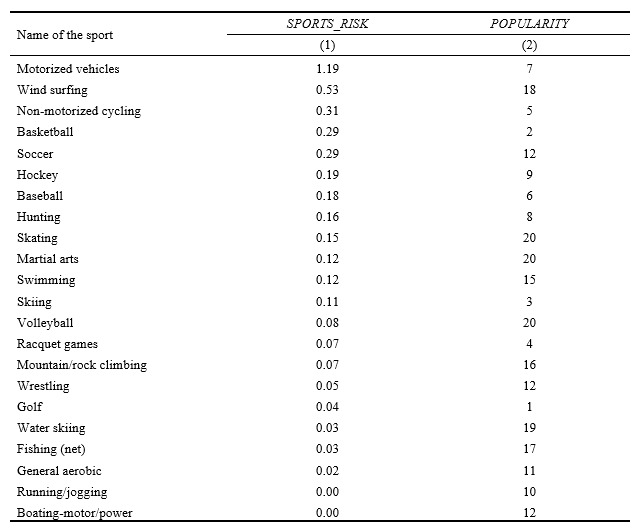

We list the top 20 most popular sports by sorted by their sports risk in Table 1. We find that motorised vehicles, including car racing and flying planes, is the most risky sport, and golf is the most popular sport (for both female and male CEOs) yet relatively low-risk. In addition, the state of California is the most common state where our sample CEOs are located, comprising 16% (117/732) of the CEOs in the sample, followed by the states of New York (11% = 79/732) and Texas (9% = 64/732). The most common sports hobbies these CEOs have are golfing, basketball, and skiing, respectively.

Results

Using a sample of 732 CEOs for US firms in Execucomp with available data on CEO self-reported sports hobbies from 1992 to 2016, we find evidence consistent with our expectation of a positive and significant association between CEO sports risk and all four measures of firms’ tax aggressiveness. These results are robust to using alternative measures of CEO sports risks and after controlling for other factors that may affect firms’ risk-taking decisions.

In cross-sectional tests, we find the positive association between CEOs’ sports risks and firms’ tax aggressiveness is more pronounced for CEOs with greater monetary incentive (proxied by equity risk incentive), and with greater CEO power (proxied by CEO pay slice) that captures the extent of freedom that CEOs have in making their aggressive tax planning decisions. These results are consistent with financial incentives playing an important role in amplifying CEOs’ risky tax planning behavior. They also show the importance of control mechanisms such as board of directors independence in constraining powerful CEOs in overriding resistance from subordinates when implementing aggressive tax planning.

Although an emerging stream of research attempts to associate managers’ personal risk preferences as a distinct managerial characteristic that affects corporate tax planning, the proxies used to measure personal risk preferences in these studies such as religiosity, gender, political orientation, and facial masculinity, likely capture multiple managerial characteristics that could confound their documented results. We differ from those earlier studies by considering a CEO’s innate and intrinsic risk proclivities captured by the CEO’s risk preferences as reflected in his/her sports hobby. An implication of our results is that if auditors, boards of directors and other parties are interested in the risk preferences of the CEO they should ask about the individual’s sports hobbies.

Table 1: Top 20 most popular sports sorted by sports risks

This table reports the top 20 most popular sports among our sample CEOs, sorted by the value of SPORTS_RISK in Column (1). Column (2) ranks the popularity of each sport listed in the table (POPULARITY), after excluding tackle football as it is likely to be a spectator sport for our sample CEOs.

Journal article

Luo, S, Shevlin, T, Shi, L & Shih, A (2022), “CEO sports hobby and firms’ tax aggressiveness”, Journal of the American Taxation Association, vol. 44, no. 1, pp. 123-153.

Recent Comments