The report “Business Fleets and EVs: Taxation Changes to support home charging from the grid” released by the Reliable Affordable Clean Energy Centre (RACE for 2030) on 28 June 2022, investigates how taxation changes can support home charging by accelerating business fleets uptake of battery electric vehicles (BEVs). The report is produced in collaboration with lead researcher, Dr Anna Mortimore of Griffith University and Dr Diane Kraal of Monash University.

Business fleets can be seen as the “effective pathway for early adoption of Battery Electric Vehicles (BEVs) but their site re-charging facility are low.” A 2020 business fleet survey indicated that home charging would need to be considered because 47% of business fleets are home garaged. Thus, providing an appropriate framework for business fleet BEVs to be home charged, by installing smart meters and optimising CO2 emission reductions, is fundamental to the transition of electrifying business fleets. Home charging is recognised as the key source of charging, where work fleet BEVs will be charged at employee’s place of residence, rather than at a workplace charging station.

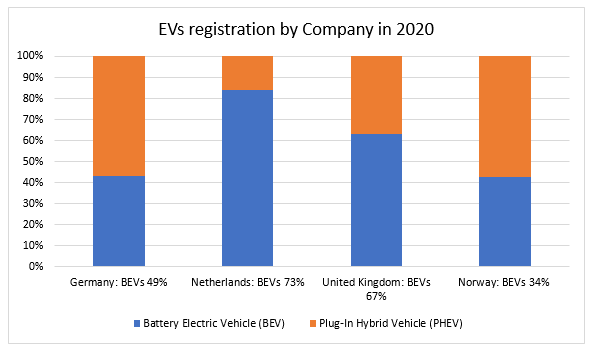

Business will not invest in workplace charging infrastructure or install home charging smart meters when business fleet managers are not choosing BEVs. That is, business buyers account for over 40% of light vehicle sales, but BEV sales to business fleets was a low 0.02% (or 488 BEVs) of the new light vehicle sales in 2020. In European countries, business fleets are the major buyers of BEVs, with over 57% of BEVs being acquired by business, showing companies play an important role in the transition of electrifying corporate fleets. The European countries with the highest uptake of business fleets were as follows.

Transport analyst Saul Lopez claims that company cars are huge driver of the new car market in Europe and after a new car is added to the corporate fleet, it will be sold off in only three to four years as a relatively new car on the second-hand market.

In these European countries, policy design of the national company car taxation have been effective in accelerating the uptake of BEVs in the corporate fleet.

We provide our recommendation on short term and long term tax changes based on the review of the above countries company car tax policy; a qualitative interview of a select fleet managers to ascertain perceptions on future uptake of BEVs, and understand attitudes, barriers and enablers with regards to adopting home charging of business fleets.

Choice of new fleet vehicle depends on the total cost of ownership

Our interviews with fleet managers indicate that purchase choice for fleet vehicles depends on the vehicles’ total cost of ownership (TCO) for BEVs and internal combustion engine vehicles (ICEVs). The TCO enables a cost comparison between a BEV and a similar ICEV, for the overall costs, including taxation concessions and resale value.

Currently there is a wide cost gap between the BEV and an equivalent ICEV, meaning BEVs are not cost competitive.

Case studies

To appreciate the challenge for business fleet managers, we modelled and compared the TCO for the Hyundai Kona. The BEV version costs $64,037 (excluding GST of $6,403) and amounts to $66,337 (exclusive of GST) if including the installation cost of the home charger of $2,300 (exclusive of GST). This was compared to its equivalent Kona ICEV costing $31,329 (exclusive of GST), resulting in a price premium of $35,008 for choosing the Kona BEV. In effect, it is not cost competitive to choose a BEV.

On top of the cost disadvantage, we found that current taxation laws can be fiscal disincentives to business fleet uptake of BEVs. For example, depreciation concessions and GST input tax credits are both capped at the car depreciation cost limit, which was $55,211 (exclusive of GST of $5,521) for the 2021-2022 income tax year. Consequently, the depreciation deduction is applied to the capped amount of $55,211 (excluding GST), and not to the cost of the Kona BEV of $64,037 (excluding GST of $6,403). The claim for input tax credit for GST paid is limited to the cap of $5,521. This means the input tax credit on the Kona BEV of $6,403 cannot be claimed in full, leaving an additional GST paid on the BEV of $882, which can be significant cost for the acquisition of large business fleets.

To encourage the uptake of work fleet BEVs and influence home charging, the project recommends 17 tax changes (both short term and long term), to reduce the cost gap between BEVs and similar or equivalent ICEVs. The recommended tax changes refer to federal taxes under the Fringe Benefits Tax Assessment Act 1986 and under the Income Tax Assessment Act 1997.

Tax recommendation examples: short-term changes to FBT and Income Tax

The following recommended tax changes, identified as short term can be applied immediately, with ministerial sign off which do not involve any major legislative reform.

Short-term tax changes to Fringe Benefits Tax (FBT) for BEVs and home charging include:

- Exempt FBT for BEVs (statutory formula method) for salary packaged arrangements.

- Home garaged fleet BEVs to be exempt from FBT.

- Home charging including smart charger to be exempt from FBT

Short-term tax changes to Income Tax for BEVs and home charging include:

- Instant asset write off to apply only to BEVs;

- Instant asset write off for the cost of home charging and smart chargers;

- Accelerated depreciation to apply only to BEVs;

- Increase GST credit limit cap for BEVs be equivalent to Luxury Car Tax threshold for fuel efficient vehicles;

- Increase depreciation limit cap for BEVs be equivalent to Luxury Car Tax threshold for fuel efficient vehicles.

Modelling short term tax changes

To illustrate the potential benefits of the tax changes, the TCO was modelled for ‘like for like’ paired KONA BEV and the KONA ICEV under current taxation law and compared when the following ‘select recommended short term tax changes were applied:

- Exempt FBT (statutory method) for the Kona BEV and not the Kona ICEV, and

- Apply the instant asset write off for the Kona BEV and not the Kona ICEV, and

- Include the Victorian government subsidy of $3,000 and road user charges.

The TCO modelling found that a combination of all the above proposed tax changes and Victorian government subsidy over a three-year period, significantly reduced the cost gap between the Kona BEV and Kona ICEV from $35,008 to $2,522, which may be acceptable to business fleet managers acquiring a fleet BEV.

This was not the case, if the KONA ICEV was a pool vehicle exempt from FBT or had zero or low private kilometres and the cost basis of FBT applied.

Recommendations for longer term tax reforms

Based on the review of overseas jurisdictions (Norway, The Netherland, United Kingdom and Germany), the following longer term tax reforms were proposed to reduce the FBT for BEVs, and encourage fleet employees home charging of fleet vehicles:

- FBT rate for car benefits be based on CO2 emissions;

- Discount FBT ‘car base value’ in statutory fraction method, for BEV fleets;

- Introduce special FBT statutory fraction for BEV fleets until there is price parity between BEVs and equivalent ICEVs;

- Provide subsidy or rebates to fleet employers for installation of home charging infrastructure.

Treasury Laws Amendment (Electric Car Discount) Bill 2022

The Albanese Government has introduced a bill to amends the FBTAA 1986 to exempt fringe benefits tax for electric vehicles from 1 July 2022 that are zero or low emission vehicles, made available by employers to current employees for cars at are below the luxury car tax threshold for fuel efficient vehicles. The exemption applying to low emission vehicles will include plug-in hybrids electric vehicles. The Government will review the FBT tax cut in three years, considering the electric vehicle tax up and whether the concessions should be continued and in what form. However, the FBT tax change, does not exempt installation of home charging and smart meters for home garaged work fleet vehicles.

The TCO modelling in the RACE for 2030 Report, indicates the government proposal will improve EV affordability, but not the cost gap between EVs and their equivalent ICEV. Additional short-term and long-term tax changes (as recommended in the report) will be required to address the cost gap.

Conclusion

Our study illustrates fiscal disincentives under the Australia’s current taxation laws to business fleet uptake of BEVs and home charging. Modelling suggests that to accelerate the uptake of BEVs in business fleet, and encourage home charging of fleet vehicles, all recommended short-term tax changes will be required for both FBT and income tax.

The longer-term tax reform proposes alternative FBT policy design to incentivise uptake of BEVs, discouraging acquisition of ICEVs by basing the FBT rate on CO2 emissions, and introducing tax rebates and tax subsidies to fleet employees and employers to support and encourage home charging, which is recognised in overseas jurisdictions.

Click the link for the full Report.

There is a higher FBT cost under the modelling because the statutory formula is used – bringing the focus to the comparative cost of the car. But, if the employee bears the costs through salary sacrifice, then the employee will only choose to have a salary sacrifice a private car (EV or IC) if there is a tax advantage in doing so. Because FBT is levied at the top marginal rate + Medicare, only the most highly paid get a tax benefit.

But FBT is calculated to recover the income tax and GST that would have been paid by the top marginal tax rate employee had he/she purchased the car out of after tax salary. The clear effect of an FBT exemption for EVs is that it is the same as making the EV fully tax deductible and GST-free. But, worse, the tax relief for this private expenditure is most valuable to the highest paid and deprives the States of GST revenue. And there is no limit on how much income tax revenue will be forgone. Any employee will be better off – and an employee can obtain full deductibility and GST-free for cars to be used privately – even by other family members.

If the aim is to provide tax relief for EVs to encourage their take up better to make it transparent and allow a flat rebate for any EV purchased. At least that is fair, controllable and not capable of abuse.

The proposal might be meritorious and the potential for tax avoidance might be overcome by limiting the exemption to EVs that are not salary sacrificed- see section 41 of the FBTAA.

What should the rebate be? The FBT payable on an EV will vary depending on the cost base of the vehicle (under the Stat Formula). Exempting the FBT for an EV, will apply in all cases (under the Stat Formula). The exemption will provide tax relief, but will not address the cost gap between the BEV and its equivalent internal combustion fuelled vehicle.

In the RACE for 2030 project, the case study compared the following like for like vehicle: a Kona BEV $66,337 compared to a Kona internal combustion engine vehicle (ICEV) $31,329. The cost gap of $35,008 (excluding GST), means the FBT (Statutory formula) for a BEV could be up to twice as much paid for an equivalent ICEV. FBT exemption will provide tax relief for the BEV, but additional tax changes will be required to address the cost gap. The UK did exempt Company Car Tax for BEVs in 2021, together with additional tax changes, subsidies and regulatory CO2 emission standards. The UK company car tax exemption was well received, where one in three UK fleet managers expect half of their company car fleet to be electric by 2025. Without policies and incentives, Australia is missing out on more affordable EVs. For instance, there were only 10 EVs under $60,000 in Australia, compared to 24 EVs in the UK. Otherwise, only employees on the who can afford the high priced EVs will benefit from the FBT EV exemption.

Under salary sacrifice arrangements the tax benefit flows to the employees on highest rate and are proportionately more for higher priced vehicles. For someone on the highest rate, about half of the price of an EV would otherwise be paid in tax. If salary sacrifice is NOT allowed, the FBT benefit flows to the employer – which is an incentive to change fleets earlier. The tax benefit doesn’t vary according to the income of the employee. But if the policy initiative is to make EVs tax deductible and GST-free, then the incentive is better directed by a rebate to the taxpayer directly of (say) 30% of the price of the car. Otherwise the measure provides proportionately more benefit to those on higher incomes. Worse, a high income earner can achieve deductibility and GST-free status for any number of cars for use by family members.

Slow charging of batteries in home garages over-night is one thing but the issues facing apartment complexes are considerable. As someone who is attempting to install infrastructure to support the adoption of electric cars in two apartment complexes I have discovered that the biggest issue we face is the inadequacy of the electricity infrastructure to handle charging facilities. Both apartment blocks will require retro-installing charging facilities and increasing the capacity to receive electricity. A very expensive problem but compounded by the fact that neighbourhood electrical sub-stations also have limited capacity and will need to be upgraded as other apartment blocks come on-line.

Yes this is a well recognised problem with installing charging infrastructure in existing apartments, and has not be regulated for new apartments. This is a transition phase, where we will see more fast chargers at petrol stations.

https://www.carsguide.com.au/car-news/goodbye-petrol-stations-hello-charging-stations-ampol-and-bp-begin-to-dump-the-pump-for