Editor’s note: This is an extract of a speech given by Miranda Stewart at the Women in Economics post-Budget event, held at the National Press Club of Australia on 16 May 2017. Speeches by two other speakers can be accessed here and here.

Budget 2017-18 highlights fairness as a key goal. A focus on the future is important and we are rightly concerned about population ageing and intergenerational fairness. However, it is important to remember that budgets in reality have current distributional impacts. In any budget, we are affecting the distribution of benefits and burdens – fairness – between people who are age 3, 23, 53, 73 in the current year.

Recognising a revenue problem but at the expense of increasing complexity

It is important that the Government has acknowledge the “revenue problem”; this is a significant change from the 2016-17 Budget which still aimed to achieve a sustainable surplus through expenditure cuts without raising taxes.

However, this Budget does not achieve tax reform. To raise revenue, the Government has modified existing levies, and grafted on some new levies, to the tax system. This adds complexity in all sorts of ways. This includes the increase in the Medicare Levy; the Skilled Worker Fund (457 visa) Levy on businesses and the Bank Levy; and the “vacant property” tax on foreign residential investors. The Budget also increases the repayment schedule (and lowers the threshold for repayment) of the Higher Education Contribution Scheme (HECS). For more on the bank levy, see my discussion, and on HECS see Bruce Chapman’s article.

For those with low incomes who receive transfers including family or welfare benefits, we are increasing surveillance as well as complexity. This includes a proposal for drug testing which is apparently for people’s own good and a new rule policing young women’s sexuality by requiring that sole parents must be certified by a third party to prove they are single.

Medicare Levy

The Medicare Levy rise of 0.5% (taking it to 2.5%) is the simplest and biggest revenue raiser, at an estimated $4 billion a year because it applies to the entire taxable income of most taxpayers, above low thresholds. For this reason, it also raises a lot of revenue from higher income earners.

In contrast, the Abbott Budget Repair Levy of 2% on top of the 47% tax rate raised about $1 billion a year. The Opposition has stated that it would seek to extend this increase in the top marginal rate. Critics have suggested that a top rate of 49.5% would produce disastrous consequences for work and creative effort. But this increase in tax progressivity, which would mostly hit those on high wages, is unlikely to have that effect: evidence shows high wage earners tend to be inelastic in their response to taxes.

The Opposition would also limit the increase in the Medicare Levy to those on above-average wages. This makes it look more like the Medicare Levy Surcharge which was introduced to encourage high earners to take out private health insurance; most of them now do so. The problem with this suggestion is it introduces yet another tax rate threshold for households with average earnings.

Housing and tax

Many of the tax measures concern housing. Most will add significant complexity, for arguably little gain.

The new limits on some rental property deductions and the removal of the main residence exemption for non-residents are likely to have only a marginal effect and add new boundaries in the system. It may simplify the ATO’s job to ban deductibility of travel expenses and end depreciation of some fixtures for rental property investors, where deductions have been trending up. But the saving is relatively small.

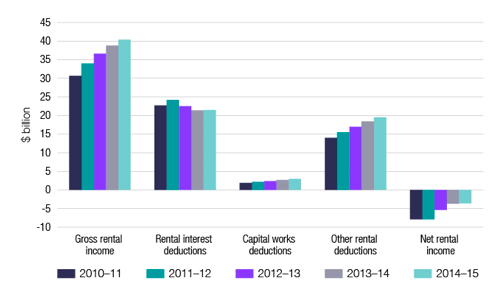

Net rental losses have almost halved in the last few years, mostly as interest rates declined, but were still $3.5 billion in 2014-15. ATO statistics reveal that the biggest contributor to negative gearing remains interest expense; it was recently identified that half of Westpac’s loan book is interest-only loans.

As observed by Rachel Ong, it would be better policy to reduce the CGT discount to 40% for investment income and gains and quarantine investment losses and expenses to investment income, as recommended by the Henry Tax Review. The goal is to establish tax treatment for savings on a more consistent basis.

Figure: Rental Property Expenses and Losses

Source: ATO Tax Statistics 2014-15

Source: ATO Tax Statistics 2014-15

The “home down-sizing” superannuation measure for retirees selling their home is dressed up as housing policy. But will it really do more than allow some self-funded retirees who have reached the $1.6 million cap on non-concessional contributions to top up their superannuation? Some financial advisors are already suggesting creative ways to plan access to this new concession.

To have more impact, the down-sizing measure would require easing of the age pension assets test. That was tightened effective 1 January 2017 and it presents a significant disincentive for homeowners on a part-pension to sell their home.

Probably the most valuable tax measure for housing has not attracted much publicity: The ability for real estate investment trusts to invest in residential real estate while still having ‘trust’ taxation could support institutional ownership of residential property, still not established in Australia. The extra 60% CGT discount is not likely to add much; the key issue here is the income stream from rental returns and capital gains on sale.

A Gender Lens on Tax-Transfer Policy

The budget has a different impact on women and men, who are differently situated in the economy, work, care responsibilities and on the income distribution. Women are more than 60% of age pensioners; more than 80% of sole parents receiving benefits; and only one quarter of the top 10% in the income distribution while the gender wage gap is 17%.

Not surprisingly, taxes that affect lower income people tend to affect women more severely as a group, while concessions that benefit high income savers tend to benefit men more than women. For example, the lower HECS threshold and Medicare Levy hike will reduce disposable after-tax income of low income workers. That includes women who are on part-time wages as well as single women and men.

But a “winners and losers” analysis misses the point. The effects of our structural tax-transfer policy impact negatively on women’s income, careers, human capital and retirement in the longer term.

With new commitments in the G20, OECD and sustainable development goals for gender equality, I hope the government will take seriously the systemic gender effects of its tax, expenditure and regulation decisions, in its budget process. At present this work is being done outside government including by the National Foundation for Australian Women’s Gender Lens and by the Opposition.

There has been recent discussion about the top marginal tax rate as “too high”, including by former Prime Minister Paul Keating. But this ignores that mothers who are very often the “second earner” in a household face among the highest effective marginal tax rates in our system, reaching 80% or 90%, when taxes, family payments and net childcare costs are taken into account.

Essentially, the budget perpetuates an Australian 1.5 earner family model in which mums work part-time and are still responsible for childcare, while dads work full-time and spend much less time caring for kids. Families respond rationally to these disincentives for mothers to increase their work participation. This means families have less income and can save and consume less. Where family breakdown occurs (in about one third of families), women may be significantly worse off. Demographically speaking, for long term growth and taxes, we all lose out.

The budget does not address this issue. Indeed, one seemingly minor family payment tweak will make this worse for many dual earner families. This is the increase in the withdrawal rate to 30% (from 20%) for means testing Family Tax Benefit A, which applies from a household income of $94,000 – one median to average male wage and one part-time female wage.

On the positive side, the reformed Child Care Subsidy which starts in 2018 will make some low and medium income earning families much better off, addressing the effective marginal tax rates to some degree; although the early childhood investment of just one more year at 15 hours per week is far from a commitment to universal early childhood education for all children as a right.

The paid parental leave scheme introduced in 2011 will continue and evidence shows it has been successful in helping women’s attachment to work and supporting infant care. It is still too low at the minimum wage; does not carry superannuation contributions; and is not for long enough. For all these reasons, men also won’t take it.

What is the vision in this budget?

The Budget seems fair; more likely, it is middle of the road. It does not reverse the trend of recent policy which embeds a gap between the haves and have nots in housing, work, social welfare, family payments and retirement. We need to do more to build social cohesion for the future.

Meanwhile, the revenue measures are just tinkering at the margins. As well as strengthening our income tax, one policy that could raise the revenue we need is broadening the GST base or raising the rate. Estimates indicate that an increase in the GST rate to 15%, even on the current base, would raise at least $25 billion per year – of course, compensation would be needed for those on low and moderate incomes. The Government abandoned the tax and federation White Papers before the last election; but we cannot rely only on the Medicare Levy and proposed Bank Levy to get back on track.

All good points but what is your vision for a fairer system? I, for one, would be willing to join with you and others like us to start forming a big picture strategy for reform. Personally, I think a greater reliance on consumption taxes on luxury items only and estate/inheritance taxes tick a lot of the boxes necessary to address income, wealth and gender inequality, as well as sustainability.