In Budget 2017-18, the Government continues to propose its Enterprise Tax Plan, in which it argues that economic growth will be supported if we cut the company tax rate for all companies to 25 per cent by 2026‑27. To date, this proposal has not been accepted by the Parliament. The Government argues that a lower corporate tax rate “promotes business investment by raising the return from investing in Australia”, and that it will “raise productivity and real wages and permanently expand the economy by just over one per cent in the long term”.

While it interesting to assess the impacts of this policy change, this analysis should not be undertaken in isolation. Economists generally believe that all taxes create distortions, thereby reducing economic activity and welfare. As such, cutting any tax rate will deliver benefits. However, the extent of the welfare benefits and the distribution of the benefits vary significantly across different taxes. The benefits of a tax cut should be measured against the benefits that would be achieved by using the money to cut a different tax.

In a new research paper, Tran and Wende (2017), we undertake comparative analysis of different taxes. Specifically, we calculate the excess welfare loss from raising each additional dollar of revenue for the three main sources of Australian tax revenue: company income tax, personal income tax and goods and services tax (GST). This is equivalent to measuring the welfare gain from a marginal tax cut.

Our analysis uses a dynamic general equilibrium overlapping generations model. This type of model has been tried and tested in many countries but has had limited use in Australia. As the model uses a general equilibrium framework, it is internally consistent with responses by households and firms balancing. The dynamic model captures transition paths and shows the time it takes for the benefits of policy changes to be realised. Lastly, as the model contains 243 different household types in every period, it captures the distributional impacts of policy changes and also the heterogeneous responses of household to policy changes.

Our findings indicate that company income tax results in the largest aggregate welfare losses as it discourages investment and subsequently decreases the capital stock. This has the effect of lowering productivity and wages. The welfare loss is large because foreign capital is highly mobile and therefore very responsive to the company tax rate.

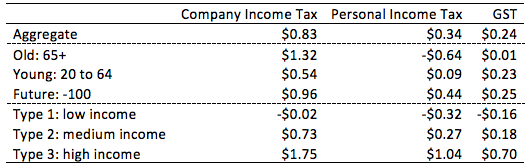

More specifically, the company income tax results in an aggregate excess welfare loss of 83 cents per additional dollar raised, compared with 34 cents for personal income tax and 24 cents for GST. The result that company income tax causes larger welfare losses than personal income tax or GST is robust to a large number of parameter changes.

Table 1: The excess welfare loss per additional dollar of revenue by tax and household grouping.

Source: Tran and Wende, 2017

The magnitude of the welfare losses in the model depend on the model calibration and also the assumptions used. Important model specifications include the assumption that the foreigners are the marginal investor in Australia, the calibration of household’s consumption leisure elasticity, the calibration of the share of fixed factors in the economy and the degree of foreign ownership. However, while the magnitudes of welfare changes vary with changes in the calibration, the ordering of the welfare loss across taxes is robust to significant changes in calibration. That is to say, company income tax has a higher aggregate excess burden than personal income tax or GST for a large range of alternate model specifications.

An alternative: Increasing tax deductions for capital investment

We also consider other ways to reduce the distortions created by company tax in our modelling. Some alternatives can result in larger aggregate welfare gains than cutting the company tax rate. These alternatives include immediate expensing (deductions for business costs) and accelerating depreciation deductions on capital investment by companies.

To understand why it is preferable to increase deductions for companies rather than cutting the rate, one needs to consider where firms derive their profits. The profits of firms can be understood as coming from two sources, being variable capital and rents. Examples of rents are land, natural resources or a firm’s market power.

The welfare loss of the company income tax is due to the distortion to investment in variable capital. Taxing rents does not distort investment in variable capital but it does have distributional impacts as it moves income from the owners of rents to the beneficiaries of government expenditure. As rents are partially foreign owned, taxing these results in a transfer from foreigners to residents and therefore improves aggregate welfare. If we can tax rent without taxing variable capital, this is welfare improving.

Immediate expensing allows the value of new investment to be deducted immediately from a firm’s taxable income. This removes the distortion to investment in variable capital while continuing to collect revenue from rents. As such, immediate expensing provides an incentive for new investment and removes the distortion of the company tax from variable capital. Unlike a company tax rate cut, immediate expensing provides no direct benefit to current equity owners as the tax rate on existing capital and rents is unchanged. The beneficiaries of increasing immediate expensing are future workers who see wage increases through higher labour productivity.

While improving welfare, company tax cuts have distributional effects

Our result that the company tax causes the largest welfare loss has important implications for the current policy debate on the company income tax cut proposal in Australia. Our analysis unfolds the fundamental mechanisms behind the benefits of cutting the company tax rate.

Importantly, we find that the welfare losses are not evenly distributed across households and generations over time.

First, cutting the company tax rate raises the dividends firms can pay out, thereby raising equity prices. This benefits those with large equity holdings, primarily older households that have had higher incomes.

Secondly, cutting the company tax rate raises investment and, over time, the capital stock, increasing future labour productivity and wages. This will benefit all future workers but high skill workers will benefit most.

Our work shows a company tax cut raises aggregate welfare but the benefits are not evenly distributed across households and generations. To obtain popular support for the tax reforms, those who benefit the most will likely have to compensate those who do not benefit as much, so that everyone can be better off.

Reference

Chung Tran and Sebastian Wende, “On the Excess Burden of Taxation in an Overlapping Generations”, ANU Working Paper 2017.

Recent Comments