Tax havens have re-emerged in the global tax debate. In 2020, France, Denmark, and Poland declared companies either registered in, or with subsidiaries in, tax havens ineligible for Covid-19 bailout packages. In April 2021, the Organisation for Economic Co-operation and Development’s (OECD’s) Inclusive Framework on Base Erosion and Profit Shifting (BEPS) received the United States’ support and proposes a global minimum corporate tax rate to help eliminate profit shifting to tax havens.

However, a perennial problem is the non-existence of a widely accepted definition of ‘tax haven’ and scarcity of suitable data in which to measure the scale of BEPS. Indicative criteria of a tax haven include: (i) no or low effective tax rates; (ii) lack of effective exchange of information; (iii) lack of transparency; and (iv) absence of a requirement that activities be substantial. Lists such as the European Union’s (EU’s) list of non-cooperative jurisdictions for tax purposes often attract criticism for not capturing all jurisdictions exhibiting the above features. Updated in February 2021, the EU includes twelve countries on the ‘black list’ and nine on the ‘grey list’ (including Australia!).

Our study exploits newly available mandatory public country-by-country reporting (CbCR) data for EU banks to document the extent to which they operate in tax havens; assess the impact of CbCR on geographic segment reporting in their annual reports; and investigate the relation between tax haven involvement and geographic segment aggregation.

Public country-by-country reporting

Since 2013, the EU requires banks operating within their jurisdiction to publish annual tax-related financial information on a country-by-country basis including: turnover, profits, taxes, employee numbers, and subsidiaries and branches (entities) for each country in which the bank operates. CbCR was a late and unanticipated inclusion within the EU Capital Requirements Directive IV (Basel III) and is expected to lead to a better alignment between a firm’s economic presence and where their corporate taxes are paid. Importantly, CbCR surpasses the pre-existing financial reporting requirements of International Financial Reporting Standards.

Research design and methodology

Our sample includes 70 multinational banks from 14 major EU countries for 2012-2016, and a control sample of 39 multinational EU insurers unaffected by CbCR requirements. These firms represent 92.5% and 83.4% of total assets of all EU banks and insurers, respectively. We hand-collected CbCR disclosure items from the annual CbCR of each bank, and geographic segment information from the segment reporting note in the financial statements.

First, CbCR data permits us to calculate the profit margin, turnover and profit per employee, and book and cash effective tax rates, at the individual country level for each bank-year. Action 11 of the final OECD BEPS project recommendations, suggests these indicators can be employed to evaluate the disconnect between the jurisdictions where taxable profits are reported and the location of the underlying real economic activities generating those profits.

Second, CbCR increases transparency of banks geographic footprint and performance, so it may alter managers’ incentives regarding geographic segment reporting. To test this, we employ a difference-in-differences research design to test for changes in the number of reported geographic segments, country segments, and line items per segment, for EU banks relative to EU insurers after the introduction of CbCR.

Third, prior United States studies suggest that managers make tax haven involvement less transparent via more aggregated geographic segment disclosures to avoid scrutiny. To test this, we estimate several empirical specifications of the relation between the intensity of tax haven involvement and geographic segment aggregation. An attractive feature of this setting is the granularity of the country-level CbCR data which permits us to develop refined measures of geographic segment aggregation and new measures of tax haven intensity. The two aggregation measures are the proportion of material countries (those who contribute 10% or more of the total sales or total profits of the bank) in which the firm operates not disclosed at the country level in geographic segment disclosures; and an average geographic fineness score that reflects the level of disaggregation of geographic segments in financial statements. The three measures of tax haven intensity are the ratio of profit/loss before tax (or turnover or entities) disclosed in tax havens to total profit/loss before tax (or turnover or entities).

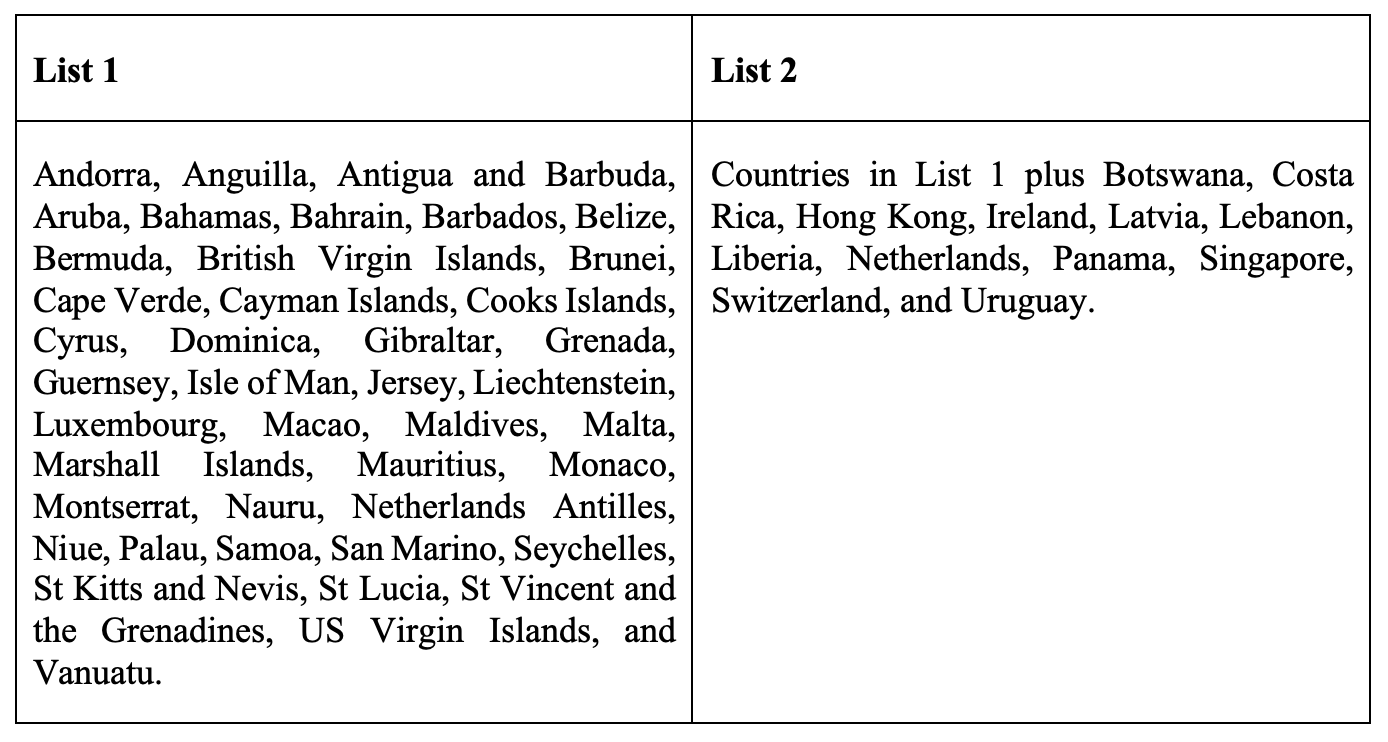

We follow prior empirical studies and rely on tax haven lists commonly used in the literature. The composition of the lists we use is crucial because several jurisdictions deemed tax havens on some lists are relatively large EU countries (for example, Ireland, Netherlands) or global financial centres (for example, Hong Kong, Switzerland, Singapore). EU banks are likely to have legitimate operations in these jurisdictions and thus less likely to be concerned about disclosing activity in these tax havens and are more likely to disclose these as stand-alone geographic segments. We begin with the most recent tax haven list used in the literature (a total of 54 tax havens). Then, we split the tax havens into ‘small tax havens’ (List 1), defined as tax havens with populations less than 1.6 million as at December 2015, and the ‘Big 12’. The ‘Big 12’ are added to List 1 to form List 2 and we use both lists in our analysis (see Table 1).

Table 1: Tax haven lists used in our study

Empirical results: Tax havens and profit shifting

The top 30 countries, ranked by the frequency with which EU banks disclose turnover or profit in that country, reveals the United Kingdom, the United States, and Germany as the most popular. However, Ireland, a tax haven, has the highest profit margin of 56.6%, second highest turnover per employee of €60.6 million, and highest profit per employee of €31.8 million. Similarly, Luxembourg has the second highest profit margin of 54.9%, fifth highest turnover per employee of €50.1 million, and second highest profit per employee of €25.5 million. In contrast, the UK has a profit margin of 35.1%, turnover per employee of €57.2 million, and profit per employee of €12.9 million.

Seven tax havens appear among the top 30 jurisdictions including, in order of frequency, Luxembourg, Ireland, Switzerland, Singapore, Netherlands, Hong Kong, and the Channel Islands. The results for Netherlands, Singapore, Switzerland, and Hong Kong, are broadly in line with those of non-tax havens which may reflect EU banks locating operations in these larger countries for legitimate commercial reasons rather than for tax minimisation. Notably, many tax havens often highlighted in the financial media (for example, British Virgin Islands, Panama), are not used extensively by the sample banks.

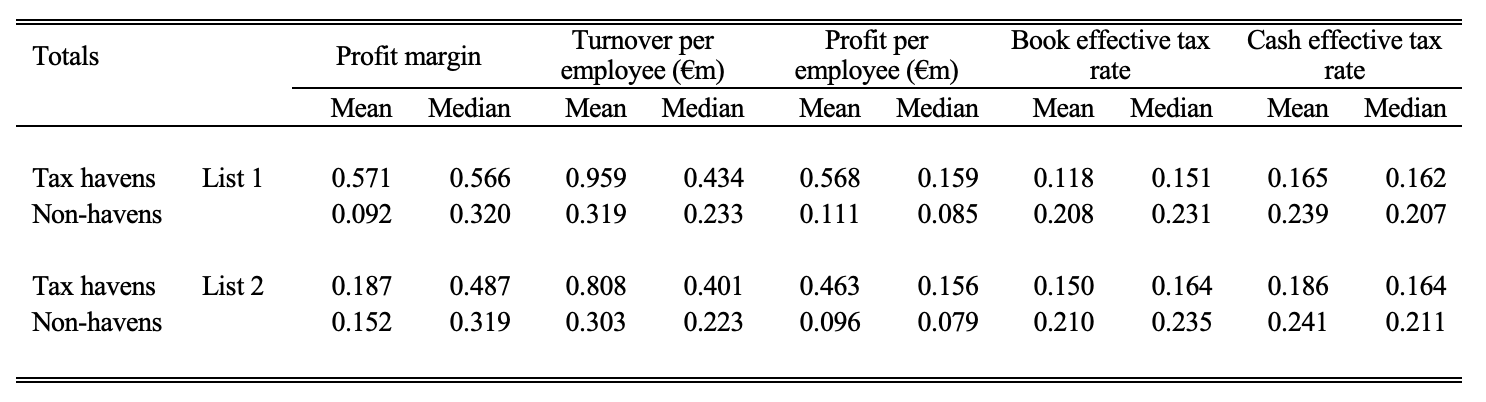

Regardless of the tax haven list used, the operations of EU banks in tax havens enjoy higher profit margins, higher turnover per employee, and higher profit per employee; and lower book and cash effective tax rates, relative to corresponding non-tax haven operations (see Table 2).

Table 2: A comparison between tax haven and non-tax haven operations of EU banks. Extract from Table 4, Panel C of Brown et al 2019.

Analysis of the 15 tax havens most used by EU banks reveals an apparent disconnect between banks’ economic presence in tax havens and the quantum of profits recognised in them. Despite only accounting for 7.8% of total turnover and 4.6% of total employees, 18.5% of total profits before tax are recognised in tax havens.

Finally, the means for the profit shifting indicators are calculated at the firm-level. Univariate tests are performed on differences in means between tax havens and non-tax havens using unconditional means and means conditional upon tax haven use. The results confirm that EU banks report statistically significantly higher profit margin, turnover per employee, and profit per employee, for their tax haven operations relative to their non-tax haven operations. For example, the unconditional mean of profit per employee for tax havens (List 1) equals 24.3% compared to 5.4% for non-tax havens (difference of 18.9% with a t-statistic of 4.85). Sample banks report significantly lower book and cash effective tax rates in tax havens although results are stronger using unconditional means.

Empirical results: Impact on geographic segment reporting

We find no evidence that the introduction of CbCR is associated with changes in the number of geographic segments, country segments, or number of line items per geographic segment, disclosed in segment reporting notes after CbCR introduction.

Consistent with the notion that EU banks may aggregate geographic segments to obfuscate tax haven activities, we find a positive association between tax haven intensity and geographic segment aggregation.

Conclusion and policy implications

Overall, these results provide empirical evidence of the significant financial benefits that accrue to EU banks operating in tax havens and provide prima facie evidence of profit shifting. The findings also suggest that EU banks operating in tax havens strategically aggregate geographic segments consistent with obfuscation of tax haven involvement to avoid criticism from operating in these politically sensitive jurisdictions.

Our evidence suggests that mandatory public CbCR has limited impact on geographic segment reporting. Nevertheless, CbCR provides additional information to better identify the existence and scale of tax haven involvement. Our results should be informative for EU policymakers who recently expanded public CbCR to all industries.

Recent Comments