In the 2021-22 Federal Budget, the Government announced that the current individual tax residency rules will be replaced with new tests, based on the recommendations made by the Board of Taxation.

The focus of this blog, based on my Journal of Australian Taxation paper, is on Australian expatriates who are living and working overseas. Expatriates face many challenges in applying the current individual tax residency rules. This blog examines whether the proposed residency tests will alleviate those issues faced by expatriates in determining their residency status.

Deficiencies in current individual tax residency rules

An individual’s Australian tax residency status is determined on a year-by-year basis. There are currently four tests to determine whether an individual is a tax resident of Australia: the ‘resides’ test, the domicile test, the 183-day test, and the superannuation test. Only one of the four tests have to be satisfied for the individual to be a tax resident of Australia.

The existing residency rules are difficult to apply. They require taxpayers to grapple with ambiguous concepts including the ordinary meaning of ‘resides’ under the ‘resides’ test and the meaning of ‘permanent place of abode’ under the domicile test that are not well defined. The lack of clarity in these key concepts in the current tax residency rules results in uncertainty for taxpayers.

The problems with the individual tax residency rules are exacerbated in the case of Australians living and moving overseas. Expatriates are required to frequently reassess their residency status to account for changes in their circumstances overseas as well as in Australia.

Taxpayers face increasing difficulties in determining tax residency

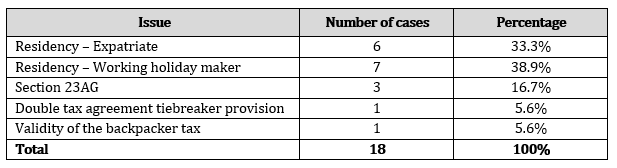

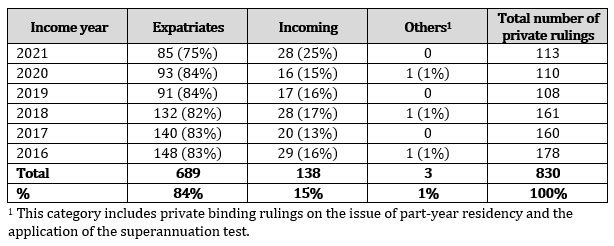

In recent years, the increase in global mobility has resulted in the issue of Australian tax residency to be a controversial area for many individual taxpayers. This is illustrated by the growing number of cases and private binding rulings on the issue of determining an individual’s tax residency status.

From 2016 to 2021, there have been 18 cases and 830 private binding rulings dealing with the issue of individual tax residency. This is in stark contrast with the 25 cases litigated in the 79 years between 1930 and 2009, when the individual residency rules were first enacted.

Table 1: Cases by issue from 2016 to 2021

Table 2: Private binding rulings from 2016 to 2021

Advantages of the proposed individual residency tests

The proposed residency tests put forward by the Board of Taxation, are based on a two-step model: a simple day-count test as the primary test of residency, followed by more complex secondary tests if the individual is not a resident under the primary test.

The proposed primary test of residency is a 183-day test; an individual will be a tax resident if they are physically present in Australia for more than 183 days in an income year. This is a simple test to apply, and it is clear when an individual will be a resident under this test, and whether the secondary tests are to be considered.

The secondary tests are based on four objective Australia-only factors: the right to reside permanently in Australia, Australian accommodation, Australian family, and Australian economic interests. Taxpayers are only required to satisfy a fixed number of factors to determine their residency status. Furthermore, the focus is on Australian connections. There is no requirement to compare the individual’s connections to Australia with their connections overseas.

This approach has an advantage over the current residency tests, particularly the ‘resides’ test and the domicile test when determining their residency status.

Arguably, the greatest challenge in applying the current ‘resides’ and domicile tests is the requirement to compare the individual’s connections overseas with their connections to Australia to determine whether the taxpayer’s behaviour is consistent with residing in Australia. This task of ‘weighting’ the individual’s circumstances is difficult since there is no certainty over the weight that is to be accorded to each factor as well as the number of factors that have to be satisfied for the taxpayer to be considered a tax resident of Australia.

Weighting of the individual’s circumstances is fundamental to the ‘resides’ test, which is the primary test of residency. Hence, the initial step to determine an individual’s residency status is already fraught with difficulties.

A similar weighting exercise is also required under the domicile test. Taxpayers are required to examine their circumstances and connections to Australia in determining if they have a permanent place of abode outside of Australia under the domicile test.

By removing the need to engage in a weighting process and by prescribing a fixed number of factors that have to be satisfied, the proposed residency tests make it easier for expatriates to determine their residency status.

Disadvantages of the proposed individual residency tests

Under the factor test, there is a risk that expatriates may be considered to have a connection with Australia and be treated as Australian tax residents based on factors that do not necessarily imply that the individual has a continuing association with Australia.

One of the factors under this test is whether the individual has Australian economic connections, which includes having a direct or indirect interest in Australian assets. As an example, an Australian bank account with significant cash deposits constitutes holding an interest in Australian assets.

My examination of recent tax law cases reveals that expatriates maintain a bank account in Australia for a variety of reasons. For instance, a bank account was treated as a relic of the taxpayer’s past life in Australia, and was maintained as a matter of convenience to meet ongoing familial commitments in Australia. In another case, a taxpayer maintained an Australian bank account due to more favourable interest rates in Australia. Maintaining a bank account does not necessarily provide a strong indication that the individual has a connection to Australia.

Another factor under the factor test is whether the individual has a right to reside permanently in Australia for immigration purposes. This factor is satisfied if the individual is an Australian citizen or an Australian permanent resident.

Although this factor provides certainty to individuals, there is a risk that this factor may apply too broadly. This is because nationality has not been considered as a strong indicator of residency in tax law, and has only been treated as a relevant factor and not a determinative factor in recent cases. Given that it is now common for individuals to be a citizen or permanent resident of more than one country, such a factor may be inappropriate.

Therefore, by taking into account the taxpayer’s Australian bank account, and taxpayer’s right to reside permanently in Australia, there is a risk that the proposed factor test may apply too broadly. This may be problematic for Australian expatriates as they may be taxed on their worldwide income and therefore be exposed to double taxation.

The proposed individual residency tests are a step in the right direction

The current tax residency rules are outdated and require modernisation. The proposed tests will help to resolve some of the existing problems with the current residency rules by streamlining the process and providing clarity and certainty to taxpayers when determining their tax residency status. However, there are downsides to the operation of the proposed residency tests, as they may be over-broad in application.

Having said the above, the proposed tests do make it easier for expatriates to determine their residency status, and are a step in the right direction.

Nice blog on international tax with informative and good quality content. Thank you for sharing this information with us. This is really helpful.

Has the new taxation rule for expats come into effect or will it be July 1, 2023?

Thanks, but I don’t think it is “a step in the right direction”. It’s crazy to define residency in this way. For example if you’ve lived overseas for 7 years with wife and children, but have siblings a bank account and a Super fund in accumulation mode in Australia, these rules could make you tax resident in Oz. This provides no certainty at all and is ridiculous by international standards for the definition of resident for tax purposes.

I think there are important faults in both the old and proposed determinations of residence for tax purposes.

If the centre of life (vital interests) is elsewhere, there is arguably no justification for Australia to define an individual as an Australian tax resident. Therefore domicile of origin should be irrelevant. Until such time as a person actually resides in Australia they should not be liable for taxation in Australia and if they visit for a short time to work, liability should start and end with the duration of the assignment.

But the new rules continue to confuse this.

I have lived overseas for 16 years working with my husband but one day may retire in Australia. I still have a bank account, rental property that is always let and super there. One day we might want to visit for 3 months and these new rules will block this. I pay tax on income derived in Australia at non-resident tax rates now. But I don’t want to pay tax on income earnt in my country of residence which is not Australia. So it means I can never visit for more than 44 days.When does this come into effect? Has it been finalised and approved?

Unhappy with the ongoing delays to implement long standing recommendations by the Board of Taxation.

My supposedly simple saga is the opposite of most of the comentators.

I am an Aussie Citizen/ Passport Holder…I am returning from Europe to make a permanent base in Australia.

I have been offered a high paying Job which will mean extensive travel to Asia/USA/EU/UK.

A reduction in the “bright line” test to say 90 days at which time Tax Residency is assurred would give Confidence to allow multiple travel out of Australia.

The various factor tests are very subjective…I plan on staying with Friends until I decide where to rent or buy,I have no Bank accounts or Super or other Investnents in Australia and sell down of Overseas Assets will take a few years….

Accordingly these factor issues dont work for me and the 183 day rule is too rigid to allow me to do my job.

Its a bloody Mess.

RealIy great article. Idon’t understand why it can’t be that you just pay on income earnt in AU and why is AU interested in your overseas income, i.e. what loop hole does this cover? NZ is the same, they want to tax on your overseas income as well.