As part of its stimulus response to the global financial crisis (GFC), the Australian Government introduced an investment tax break. This policy allowed businesses undertaking machinery and equipment investment during 2009 to claim extra tax deductions, which ranged from 10-50 per cent of the cost of the investment.

In a recent working paper, we use two business-level datasets to assess the effects of the tax break. While many of the other components of the GFC stimulus have previously been evaluated, our work is the first to evaluate the effectiveness of the investment tax break.

Whether investment tax breaks affect business investment is of obvious interest from a public policy standpoint. In addition, one element of Australia’s company tax regime makes an Australian answer to this question particularly interesting: the imputation of corporate dividends.

As recently explained in this blog by John Freebairn, under dividend imputation, tax paid by companies becomes a credit for the personal income tax of resident shareholders. Any decline in the tax paid by a company is offset one-for-one by an increase in the tax payable by resident shareholders on their dividend income. This means that the companies that we study, which are owned by resident shareholders, faced little to no fall in their cost of capital as a result of the policy.

As such, any measured investment response is likely to be driven by other ‘non-standard’ mechanisms, such as a relaxation of financial constraints. This means that our work provides new evidence on the mechanisms underlying the investment response to such tax incentives.

Measuring the effect of the tax break

The key difficulty in measuring the effect of policies such as the tax break is accounting for other factors that may also affect investment. To measure the effect of the tax break in isolation, we exploit the fact that the tax break was more generous for small businesses than it was for large businesses. For investment undertaken during the last six months of 2009, small businesses received a 50 per cent bonus deduction, while large businesses only received a 10 per cent bonus deduction.

The exact definition of ‘small’ and ‘large’ businesses for tax purposes was complicated. Broadly, businesses with revenue below $2 million were considered small and others were large. So, our analysis amounts to comparing the investment of businesses with revenue above and below $2 million. To examine this, we used two business-level datasets: tax data contained in the Australian Bureau of Stastics’s (ABS) Business Longitudinal Analysis Data Environment (BLADE); and the microdata from the ABS’s Survey of New Capital Expenditure.

We employed two statistical techniques for identifying the effects of policy changes. The first is regression discontinuity. This approach compares investment for businesses with revenue just below $2 million to investment for businesses with revenue just above $2 million. Any difference between the investment outcomes is interpreted as the effect of the policy. The key assumption is that businesses just above and below the revenue threshold were identical, apart from the different treatment under the tax break.

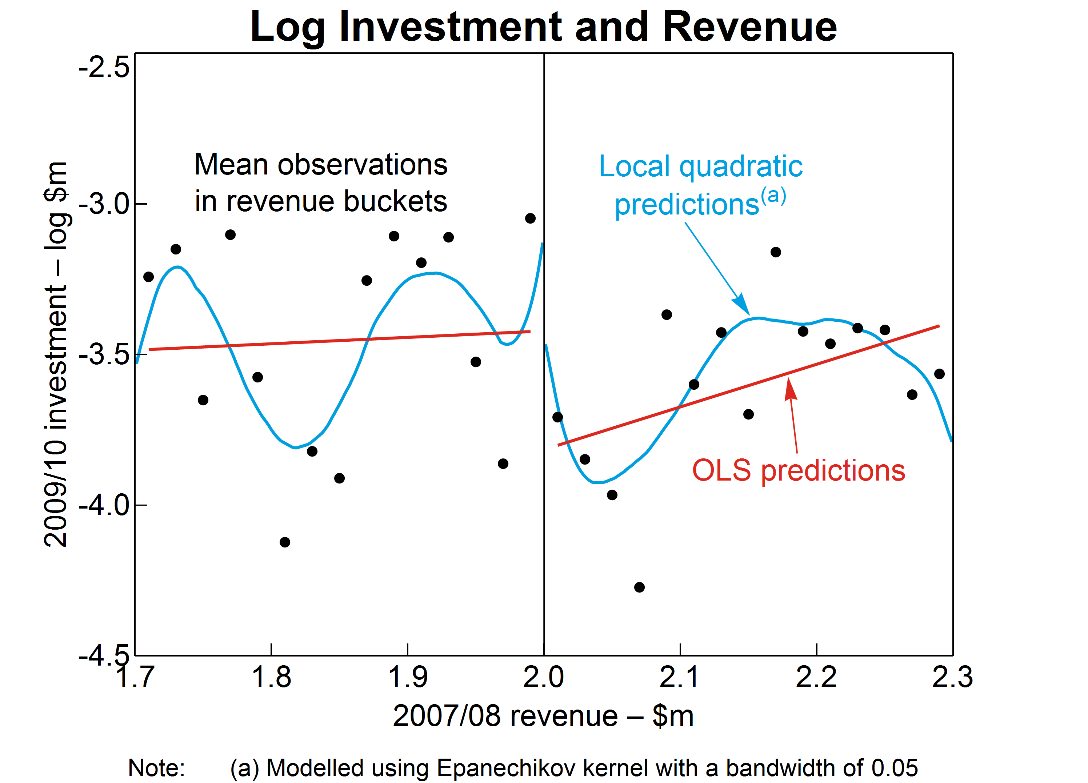

A graphical representation of the approach is shown in Figure 1. The dots represent mean investment by businesses falling into different revenue buckets ($20,000 wide). The red and blue lines are lines of best fit using linear and more flexible approaches, respectively. All three provide evidence of a sizeable fall in investment for businesses with revenue above the $2 million threshold.

Figure 1

The second technique we used was difference-in-differences. This technique relies on identifying a control group, in our case large businesses, and a treatment group, small businesses. It measures the effect of the tax break as the difference between the change in investment for small businesses across the pre-tax break and tax break periods, and the change for large businesses. The key assumption is that, in the absence of different treatment under the tax break, the two sets of businesses would have behaved similarly.

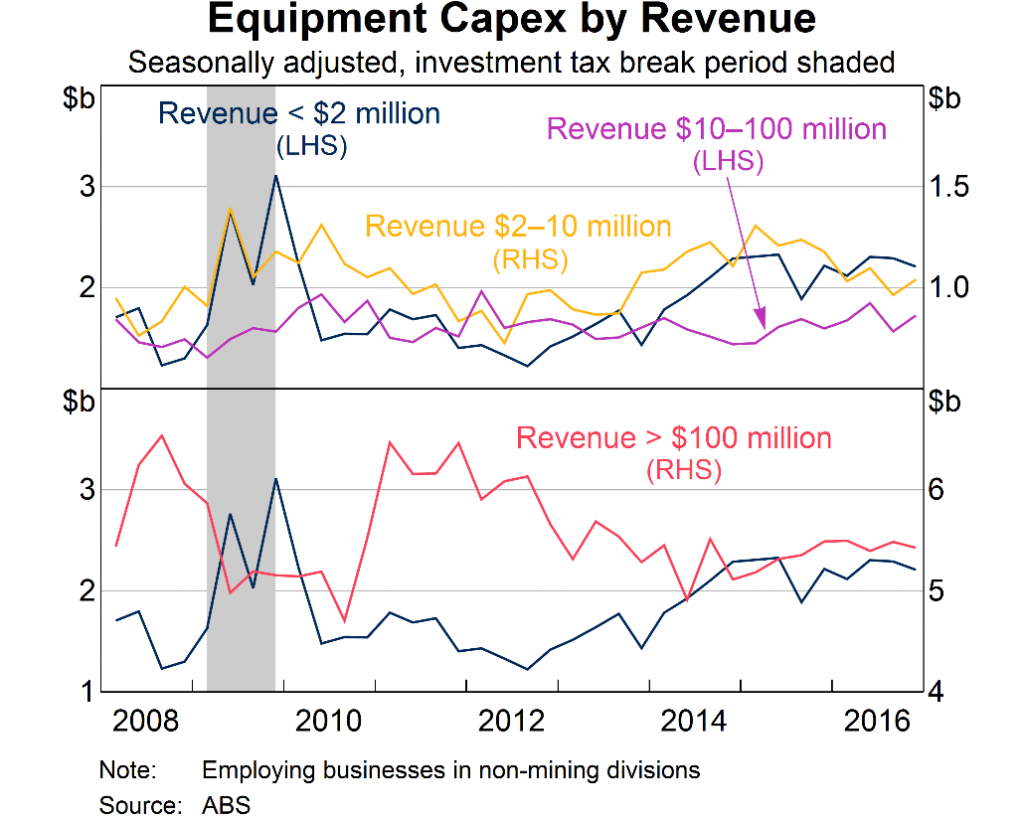

Figure 2

Figure 2 shows a graphical representation of this technique. The data show a very clear distinction between equipment capital expenditure (capex) for businesses receiving the highest tax break (revenue below $2 million), and other businesses during the tax break period (shaded). It also shows that outside of this period, investment behaved similarly for small and large businesses, particularly businesses in the $2‑$10 million revenue range.

Results

Both our regression discontinuity and difference-in-differences approaches provide strong evidence that businesses responded to the tax break by increasing investment. Moreover, we find no evidence that businesses responded by lowering investment in future years. So the tax break stimulated an actual increase in investment and the capital stock, rather than just bringing forward investment from future years.

Still, the magnitude of the effects differed by business type. A 10 percentage point increase in the rate of the tax break is estimated to have increased companies’ investment by around 15 per cent, and unincorporated businesses investment by around 60 per cent.

The much larger response of unincorporated businesses is consistent with the fact that they face a different taxation regime to companies. For unincorporated businesses, the tax break lowered the owner’s tax bill, giving the owner an additional incentive to invest. In contrast, for companies owned by residents, the lower tax paid by the company was offset by higher tax paid by the shareholders on their dividend income, and so such an incentive does not exist.

Still, the fact that companies did respond suggests that the tax break increased their incentive or ability to invest. That is, it influenced businesses through some other ‘non-standard’ channel. We speculate that the tax break may have freed up businesses’ cash flows, therefore allowing them to invest more by loosening their financial constraints.

The macroeconomic effect

While identifying whether or not businesses responded to the tax break is interesting, a natural policy questions is: did the tax break have a substantial effect on the macro-economy?

We estimate that, without the policy, private equipment investment would have been around 30 per cent, or $22 billion, lower in 2009. We adjust this down to account for the fact that around 25 per cent of business investment in Australia is done using imported goods and estimate the general equilibrium effects of the policy using a dynamic stochastic general equilibrium model.

The model suggests that, without the additional investment induced by the tax break, year-ended real gross domestic product (GDP) growth over 2009 would have been 0.8 per cent, well below actual growth of 1.7 per cent. Moreover, the cash rate would have been around 50 basis points lower.

Conclusions and implications

Overall, our results indicate that the investment tax break introduced by the Australian Government during the financial crisis had a substantial effect on business-level investment and the macro-economy. That said it is important to note that the work provides only limited guidance on the potential effects of policies other than the one we studied. Other policies will differ in their timing, permanence and targeting, all of which could influence the results.

In particular, our results suggest that the tax break affected investment in part through non-standard mechanisms. While further work is needed to identify these mechanisms, one prime candidate is a loosening of financial constraints. If this was the key channel, we might expect policies like investment tax breaks to be more effective during downturns, when such constraints are more binding.

The views expressed in this article are those of the authors and do not necessarily represent those of the Reserve Bank or the Australian Bureau of Statistics. The working paper can be accessed here.

The results of these studies are based, in part, on ABR data supplied by the Registrar to the ABS under A New Tax System (Australian Business Number) Act 1999 and tax data supplied by the ATO to the ABS under the Taxation Administration Act 1953. Please see this disclaimer notice.

How about during business as usual scenarios – is the trickle down effect a fantasy or is it good economics to give businesses and the top end of earners a tax cut at expense of others?