In Part 1 of this series on Basic Income, we travelled back in time to England on the eve of the industrial revolution in search of the first Basic Income scheme. When capitalism supplanted the traditional master-and-servant system of pre-industrial England, the Speenhamland system of local benefits for rural workers was replaced by the brutalities of the New Poor Law that denied benefits to ‘able-bodied’ unemployed people so that the factories had a ready supply of labour.

In the 20th century, the labour movement and social reformers learned from the past that under capitalism, the labour market, politics and social welfare are intertwined. They built a ‘welfare state’ on a foundation of universal suffrage, full employment, labour regulation, universal social services, and social security for people lacking enough income to live decently.

In Part 2, we identified challenges to the modern welfare state including precarious employment, attempts to wind back social spending, and the increasingly harsh treatment of people relying on working-age social security payments which recalls the Poor Law distinction between ‘deserving and undeserving’ poor. This has led to new questions about whether, and how, a Basic Income scheme might be part of the solution.

The three pillars of the social minimum

Income support is only one element of the ‘social minimum’ – the set of social guarantees that underpin income security in wealthy capitalist societies. The three pillars of a decent minimum income are the family, labour market regulation, and the welfare system, broadly defined.

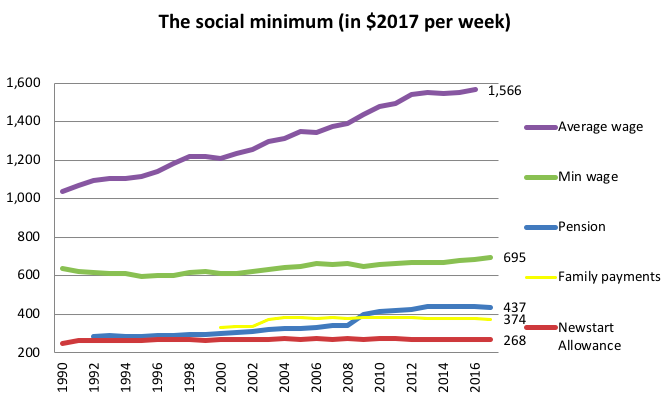

Figure 1 shows trends in key components of the social minimum income in Australia.

Figure 1: Wages, benefits and pensions for a single adult ($ per week, adjusted for inflation)

Sources: ACOSS (2017), OECD StatExtracts; Department of Social Services

Note: Minimum wage for a fulltime worker, excluding overtime. Average weekly ordinary-time earnings in main job for men and women. Family payments for two children (one of primary school-age, the other of preschool age), including maximum Rent Assistance.

Over the last two decades, the social minimum has lagged behind growth in average full-time wages. This has contributed to growth in poverty and income inequality. Figure 1 shows:

1. Newstart Allowance (unemployment benefit) is very low (currently $38 a day) and has not increased above inflation for over 20 years. The last ‘real’ increase was a $2 a week rise from the Keating government in 1994.

2.Minimum wages have barely increased in real terms for two decades, and there is a reasonably consistent relationship between them and Newstart Allowance rates.

3. Consistent with Poor Law principles, allowances for those deemed ‘able to work’ are much lower than pensions for those deemed ‘unable to work’.

4. Apart from pensions (which are indexed to wages), the social minimum is falling behind wider community living standards, proxied here by the average full-time wage. That is, the benefits of rising productivity and living standards have largely been denied to unemployed people and minimum wage-earners for two decades. Their living standards were effectively frozen in an era when the internet was in its infancy.

5. Family payments for those with low incomes rose in real terms during the 2000s but have since declined. This is due to the removal of their indexation to wages in 2009 and subsequent decisions to freeze maximum rates of payment.

Back to a Basic Income?

A Basic Income scheme alone cannot guarantee that everyone in or out of paid work has a decent income. Critics of universal basic income are right to warn that replacing employment, wage and welfare protections and services with a minimum income guarantee is risky. It risks a repeat of the Speenhamland experience that powerful interests pull the new system down, arguing that it’s too costly and work incentives and the ‘dignity of work’ would be diminished. Another risk is that income protections in the other pillars of the social minimum – especially wages and human services – would be adjusted downwards.

A better question to ask is whether a Basic Income, together with reforms to strengthen the other pillars of the social minimum, could ensure income security for all.

Much depends what kind of Basic Income scheme is introduced. Some options are:

1. A ‘living income’ (which people can live on in accordance with general community expectations – that is, above poverty levels) to replace the present social security system. This has two variants – an income-tested payment and a universal one.

2. An ‘income supplement’ which is not enough to live on, but supplements wages or social security payments to give people more flexibility to negotiate a more uncertain labour market, help with extra costs (such as a disability or retraining) or to combine employment with other roles such as care. This is usually advocated as a universal payment, or one that at least extends to the majority of income-earners.

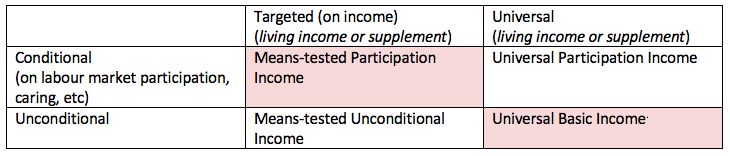

At the heart of the contest between different Basic Income models are tensions between adequacy and universalism, and between the obligations and entitlements of citizens.

Either a living income or an income supplement could be conditional (for example, on labour market participation) or unconditional (for example, an entitlement of citizenship). This distinction was drawn by Tony Atkinson, who advocated a ‘Participation Income’.

Tensions between adequacy and universalism arise due to the high cost of a universal scheme providing sufficient income for people to live on. As Martinelli (2017) puts it: ‘an affordable UBI would be inadequate, and an adequate UBI would be unaffordable’.

Whiteford estimates that a universal, unconditional Basic Income set at the pension rate ($21,000 a year for a single adult), with allowances for partners and children, would cost $360 billion a year, compared with the $150 billion cost of existing social security payments. A large increase in tax rates (not only for high income-earners) would be needed if this were funded through the income tax system, even if the Univeral Basic Income replaced the tax-free threshold (Scutella 2004).

On the other hand, a Universal Basic Income costing the same as the current social security and welfare programs would yield a payment of around $6,000 a year, less than half the already inadequate Newstart Allowance ($13,500).

Basic Income options for Australia

Most debate in Australia has focused pragmatically on two options (the shaded segments of Table 1):

1. A ‘Basic Living Income’ that replaces existing income support and is means-tested. An example is the ‘common working-age payment’ advocated by a government welfare review in 2001.

2. A modest ‘Universal Basic Income’ that supplements income support and minimum wages and is not means-tested. An example was the ‘Guaranteed Minimum Income’ advocated by the Henderson Poverty Report in 1976.

Table 1: Types of Basic Income

Impact of options on the labour market and welfare system

What is the likely impact of these basic income options on the labour market and welfare system?

Much of the debate over the labour market impact of a Basic Income scheme concentrates on ‘work incentives’ for paid work. As Martinelli (2017) and Bowman et al (2017) point out, this argument has been over-stated. Experimental unconditional Basic Income schemes in the United States and elsewhere have only marginally reduced labour force participation. The myth of the ‘dole bludger’ who would rather do nothing at home than work is just that. The main impacts on paid workforce participation were among people who gave priority to other activities, especially caring and studying.

The more interesting, and more important, labour market impact of a basic income is its effect on wages. This could go either way. If workers have an alternative to working for wages they may drive a harder bargain, in which case wages would rise. Alternately, if workers have access to a wage supplement, employers may drive a harder bargain to capture this subsidy, or the Fair Work Commission may discount minimum wages, in which case wages would fall.

According to Martinelli (2017) and Gray (2017), who can drive the harder bargain depends on which Basic Income option is chosen.

Option 1 (Basic Living Income) is likely to improve pay and conditions for low-skilled work. It might (modestly) reduce workforce participation among unemployed people, especially if unconditional. Low-skilled workers, who are less likely to have substantial family resources or personal savings to fall back on, would have a viable alternative to working in a job they don’t want.

If the Basic Living Income were income tested to moderate its cost, then it is of no immediate benefit to middle and higher income-earners, but would still play a vital insurance role for those households. We all face risks such as redundancy, ill health or marital separation.

Option 2 (modest Universal Basic Income) is likely to strengthen pay and conditions for higher-skilled work and may reduce their paid workforce participation slightly (mainly among parents and other carers). This is because even a modest Basic Income would enhance choices for those with significant family support or savings.

However, it would probably reduce wages for low-skilled workers who lack family support or savings. A modest Universal Basic Income would do little to improve their bargaining power. Unless it is built on a solid foundation of robust minimum wages and secure working hours, the subsidy is likely to captured by employers, especially if Fair Work Commission takes account of a major increase in public support when setting minimum wages.

Climbing or sinking?

(Source: Koi Bito Forum)

The end result could be an increase in wage inequality. By supplementing low-paid, insecure work, there is a risk that a Basic Income that is too low to live on could entrench it for people lacking bargaining power.

In Part 4, I will examine three possible responses to the dilemmas identified above: (1) a means-tested Basic Living Income; (2) a less strictly means-tested ‘life cycle’ Living Income and (3) A set of smaller Supplements to meet particular costs. These could be combined to form a two-tier Basic Income scheme with a base rate of payment to meet general living costs and a supplementary tier to meet additional costs.

This four part series is written based on the presentation, ‘From basic income to poor law and back again: can a UBI break the Gordian Knot between social security and waged labour?’, by Peter Davidson at the Australian Social Policy Conference at UNSW on 27 September 2017. Read Part 1, Part 2 and Part 4.

Pingback: From Basic Income to Poor Law and Back Again - Part 4: Designing a Viable Basic Income - Austaxpolicy: The Tax and Transfer Policy Blog

Pingback: From Basic Income to Poor Law and Back Again - Part 2: Whither the Welfare State? - Austaxpolicy: The Tax and Transfer Policy Blog